دانلود مقاله حرفه ای بودن و اصول اخلاقی حسابداران مدیریت

چکیده

این مطالعه با استفاده از سناریوهای تجربی نشان می دهد که ویژگی های حرفه ای حسابداران مدیریت یعنی تعهد اجتماعی، استقلال حرفه ای، وابستگی حرفه ای و از خود گذشتگی حرفه ای، با سه اصول اخلاقی در ارتباط هستند که نقش های مهمی در قضاوت اخلاقی، درک اصول اخلاقی یک عمل؛ عدالت اخلاقی، قرارداد گرایی و نسبیت گرایی ایفا می کنند. فهم این مسائل، به تعیین ویژگی های حرفه ای حسابداری مدیریت که باید برای تشویق قضاوت های اخلاقی حسابداران مدیریت ترویج داده شوند، کمک می کند زیرا تحقیقات نشان می دهد که اصول عدالت اخلاقی و قرارداد گرایی، با افراد در مرحله فوق قراردادی توسعه اخلاقی و قضاوت های اخلاقی تر، سازگار است، در حالی که اصول نسبیت گرایی، با مرحله قراردادی توسعه اخلاقی و قضاوت های کمتر اخلاقی سازگار است.

مقدمه

این مطالعه، ارتباط بین ویژگی های حرفه ی حسابداری مدیریت، اصول اخلاقی آنها، قضاوت اخلاقی و درک اصول اخلاقی یک عمل را مورد بررسی قرار داده است. حرفه ای بودن شامل مسئولیت درک شده برای اجتناب از منافع شخصی در انجام وظایف (Kerr، Von Glinow، Schriesheim، 1977)، و درخواست یک استاندارد رفتاری بالاتر از استاندارد مورد نیاز قانون است (Goode، 1957). حرفه ای ها فرصت های زیادی دارند که مطابق با منافع شخصی خود عمل کرده و مسئولیت های خود نسبت به جامعه را رها کنند. این رفتار نمی تواند صرفا به وسیله ضوابط اخلاقی، پاداش های خارجی یا تحریم ها انجام شود، بلکه در عوض باید درونی شود (Noreen، 1988). این امر مستلزم درک بهتر عوامل چند بعدی درگیر در تحت تاثیر قرار دادن قضاوت اخلاقی است. این ارزش های مشترک، از طریق فرایند اجتماعی کردن (Goode, 1957) و راهنمایی یک بزرگسال با معضلات اخلاقی به وجود آمده از طریق استانداردهای حرفه ای ارائه شده اند. به عنوان مثال، تحقیقات نشان می دهند که رفتار اخلاقی به شدت تحت تاثیر محیط حرفه ای فرد قرار دارد، حتی در زمانی که رفتار، مطابق با استانداردهای اخلاقی فرد نیست (Shaub, Finn & Munter, 1993). حرفه ای بودن همچنین به عنوان انگیزه یک خودانگاره یک فرد پرکار و شایسته توصیف شده است (Kalbers & Fogarty، 1995). انتظار می رود که این خودانگاره در میان ارزش های اخلاقی مشترک بسط داده شود. بنابراین انتظار می رود که میزان حرفه ای بودن افراد، با تصمیم گیری اخلاقی آنها در ارتباط باشد. این مطالعه، این رابطه را مورد بررسی قرار داده است.

نتیجه گیری

رفتار اخلاقی، بنیاد حرفه حسابداری مدیریت است و این به طور مستقیم با قضاوت های اخلاقی مرتبط است (Flory et al.، 1992؛ Reidenbach & Robin، 1990). این گزارش نشان می دهد که ارتقاء چهار ویژگی حرفه ای بودن: تعهد اجتماعی، استقلال حرفه ای، وابستگی حرفه ای به جامعه و از خود گذشتگی حرفه ای، استفاده از سه اصل اخلاقی را تقویت می کنند که نقش مهمی در قضاوت های اخلاقی: عدالت اخلاقی، نسبیت گرایی و قرارداد گرایی دارند. از آنجایی که IMA و اعضای فردی حرفه ای بودن را ارتقاء می بخشند، آنها انگیزه های تفکراتی هستند که منجر به تصمیم گیری های اخلاقی تر می شوند. درک این پیوندها، به راهنمایی این حرفه در فراهم کردن زمینه تصمیم گیری اخلاقی تر برای اعضای آن در سازمان های خود کمک خواهد کرد. آگاهی از روابط بین فعالیت ها و منافع حرفه حسابداری مدیریت و روند تصمیم گیری اخلاقی در این مورد بسیار ارزشمند خواهد بود.

Abstract

Using experimental scenarios, the current study suggest that the management accountants’ professional attributes social obligation, professional autonomy, professional affiliation, and professional dedication are associated with three ethical rationales that have been identified as playing important roles in ethical judgment, the perception of the ethicality of an action; moral equity, contractualism, and relativism. Understanding these issues will assist in determining the management accounting professional attributes that should be fostered in encouraging the ethical judgments of management accountants since research indicates that the moral equity and contractualism rationales are consistent with individuals at the postconventional stage of ethical development and more ethical judgments while the relativism rationale is consistent with the conventional stage of moral development and less ethical judgments.

Introduction

The current study examined the association between attributes of the management accounting profession, their ethical rationales, and ethical judgment, the perception of the ethicality of an action. Professionalism involves the perceived responsibility to avoid self-interest in the performance of duties (Kerr, Von Glinow, & Schriesheim, 1977), demanding a higher standard of behavior than required by law (Goode, 1957). Professionals have many opportunities to act in their own self-interest, forsaking their responsibilities to society. This behavior cannot be solely enforced by ethical codes, external rewards or sanctions, but must instead be internalized (Noreen, 1988). This requires a better understanding of the multidimensional factors involved in influencing ethical judgment. These shared values are inculcated through an adult socialization process (Goode, 1957) and guidance with ethical dilemmas provided through professional standards. Research indicates, for example, that ethical behavior is strongly influenced by individual’s professional environment, even when the behavior is inconsistent with the individual’s ethical standards (Shaub, Finn & Munter, 1993). Professionalism has also been described as motivating a self-concept of a high performing, competent individual (Kalbers & Fogarty, 1995). This self-concept is expected to extend to shared ethical values. Individuals’ levels of professionalism are therefore expected to be related to their ethical decision making. The current study explored this relationship. Although 80% of accounting students have management accounting careers and most accountants work in corporate accounting (Isaacs, 2016) very few studies have examined management accounting professionalism and only one of those has used a multidimensional concept of professionalism (Shafer, Park, & Liao, 2002). This study investigates a potential benefit of professionalism for constituents of management accounting. Understanding these issues will assist in determining what attributes the management accounting profession should foster in encouraging the ethical judgment of management accountants and as well highlight a benefit of specific management accounting professional attributes.

Conclusion

Ethical behavior is a cornerstone of the management accounting profession and this is directly related to making ethical judgments (Flory et al., 1992; Reidenbach & Robin, 1990). This report suggests that promoting four attributes of professionalism: social obligation, professional autonomy, professional community affiliation, and professional dedication will encourage the use of three ethical rationales identified as playing important roles in making ethical judgments: moral equity, relativism, and contractualism. As the IMA and as individual members promote professionalism, they are motivating ways of thinking that lead to more ethical decisions. Understanding these links will help guide the profession in preparing its members to be more ethical decision makers within their organizations. Knowing the relationships between the activities and benefits of the management accounting profession and the ethical decision-making process will be invaluable in this regard.

(جهت بزرگ نمایی روی عکس کلیک نمایید)

H1: When making ethical judgments, management accountants’ beliefs in professional autonomy, professional affiliation, self-regulation, and professional dedication are positively associated with their use of the relativism rationale.

H2: When making ethical judgments, management accountants’ belief in social obligation is positively associated with their use of the contractualism and moral equity rationales.

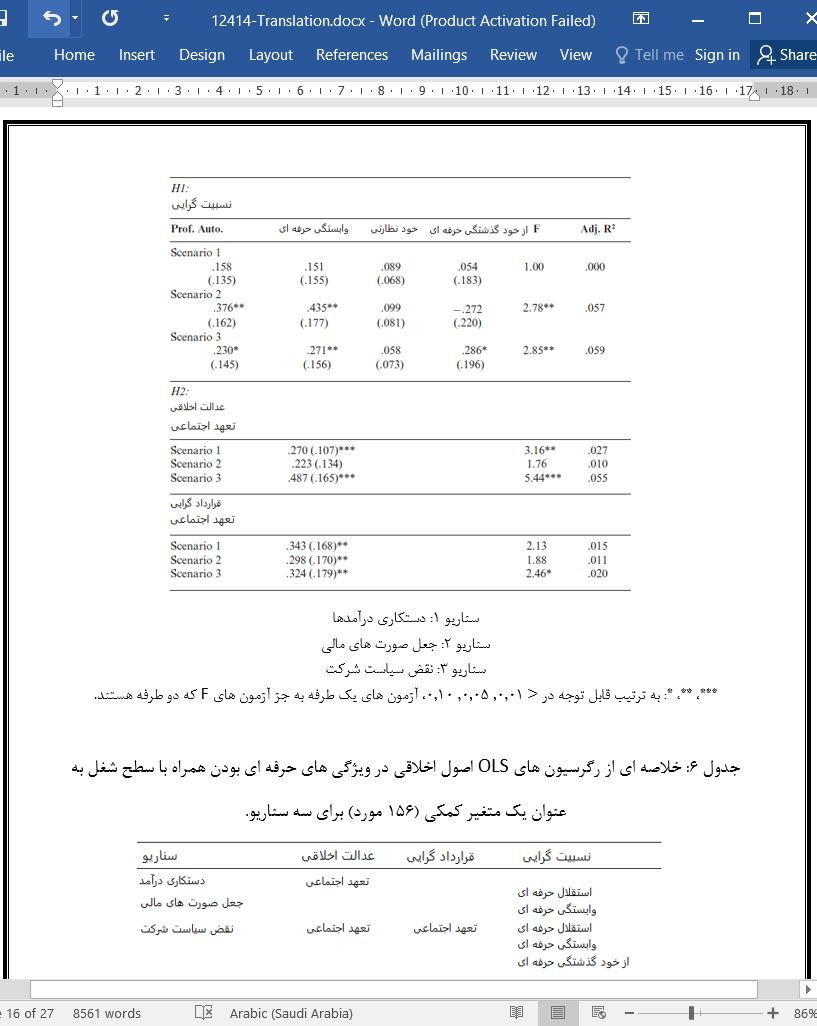

H1: هنگام قضاوت اخلاقی، اعتقاد حسابداران مدیریت به استقلال حرفه ای، وابستگی حرفه ای، خود نظارتی و تعهد حرفه ای، دارای ارتباط مثبت با استفاده آن ها از اصول نسبیت گرایی است.

H2: در هنگام قضاوت اخلاقی، اعتقاد حسابداران مدیریت به تعهد اجتماعی دارای ارتباط مثبت با استفاده آن ها از اصول قرارداد گرایی و عدالت اخلاقی است.

چکیده

مقدمه

بررسی ادبیات و توسعه فرضیات

روش تحقیق

نتایج

نتیجه گیری

منابع

Abstract

Introduction

Literature Review and Hypothesis Development

Research Methodology

Results

Conclusion

References

- اصل مقاله انگلیسی با فرمت ورد (word) با قابلیت ویرایش

- ترجمه فارسی مقاله با فرمت ورد (word) با قابلیت ویرایش، بدون آرم سایت ای ترجمه

- ترجمه فارسی مقاله با فرمت pdf، بدون آرم سایت ای ترجمه