دانلود رایگان مقاله توسعه مدل مفهومی تاثیرات پیرامون گزارشگری یکپارچه

چکیده:

هدف: در این مقاله به یک مدل مفهومی برای تعیین توسعۀ گزارشگری یکپارچه، مقالات موجود در نشریۀ Accounting Research Meditari در موضوع گزارشگری یکپارچه روی مدل و شناسایی حوزه های تحقیقاتی آتی پرداخته خواهد شد.

طرح/روش/رویکرد:در این مقاله از سبک روایتی/استدلالی برای خلاصه سازی یافته های کلیدی و مهم حاصل از مقالات ارائه شده در این ویژه نامه و یک دستورکار پژوهشی اصولی بهره گرفته می شود.

یافته ها:یافته های پژوهش های قبل و همچنین مقالات ارائه در این موضوع خاص، مدل مفهومی ارائه شده در این مقاله را تأیید می کنند. این مدل مفهومی جدید را می توان به شیوه های گوناگون مورد استفاده قرار داد.

ابتکار/ارزش:در این ویژه نامه برخی از آخرین پیشرفت های موجود در زمینۀ گزارشگری یکپارچه از چندین حوزه قضایی بررسی می گردد. روش ها و چهارچوب های نظری مختلف به همراه شواهد اولیه پیرامون تجربۀ گزارشگری یکپارچه منجر به یک ارزیابی کثرت گرایانه از گزارشگری یکپارچه می گردد که می تواند به عنوان پایه و اساسی برای پژوهش های آینده استفاده گردد. این مدل مفهومی جدید ارائه شده در این مقاله را می توان به عنوان یک چهارچوب سازمان یافته، روشی برای درک و فهم تأثیرات گوناگون، روشی برای شناسایی دیگر عوامل کنترل در یک مطالعه و روشی برای شناسایی سئوالات تحقیقاتی جدید، جذاب و کشف نشده مورد استفاده قرار داد.

مقدمه

گزارشگری یکپارچه (IR) عملا در اوایل هزارۀ سوم آغاز شد. این گزارشگری پاسخی بود به بحرانی مالی جهانی و سلسله شکست هایی که اعتماد به صورت وصعیت های مالی مرسوم را از پایه تخریب کرد و بر محدودیت گزارشگری بازنگرانه در اقدام واحد عملکرد سازمانی (IIRC, 2013) تأکید داشت. نقاط ضعف گزارشگری تداوم پذیری نیز مرتبط بود. گزارشات تدام پذیری سنتی عدم افشاهای محیطی، اجتماعی و اطلاعاتی (ESG) را به صورت مجزا از اطلاعات مالی ارائه داد و ارتباط بین استراتژی، خطرات و اشکال مختلف سرمایه تحت کنترل یک سازمان را نشان نمی داد (De Villiers et al., 2014, 2017).

در این زمینه، IR تکامل بخش اطلاعات مالی و محیطی اجتماعی را به فرمتی که انواع مختلف عدم افشاها متصل به یکدیگرند ارائه داد (. De Villiers et al.,2014, 2017; Solomon and Maroun, 2012). براساس فلسفۀ تفکر یکپارچه، IR را می توان به عنوان یک ضرورت برای گزارشگری و مدیریت کسب و کار شفاف و مسئول تلقی کرد که هدف آن ارائه اطلاعات باکیفیت تر است و این اطلاعات روابط متقابل بین ابعاد اجتماعی، محیطی و اقتصادی یک سازمان را توضیح می دهد و همچنین ارتقای کیفیت اطلاعات ارائه شده به سهامداران و ارتقای شیوه های کسب و کاری پایدار از اهداف آن است (Maroun and De Villiers, 2017).

آنچه قابل بحث است این است که آغاز IR به انتشار King-I در سال 1994 برمی گردد. King-I در آفریقای جنوبی در پاسخ به لزوم اثبات اعتبار بازار سرمایۀ محلی و ارائۀ یک مدل مرکزی سهامداری جهت مسئول نگه داشتن شرکت ها در قبال عملکردشان توسعه داده شد. بعد از انتشار King-II در سال 2002 بود که ایدۀ گزارشگری فعالیت اجتماعی، محیطی و اقتصادی و نقش پیشگام آفریقا در گزارشگری اطلاعاتی (نظارتی) شرکتی را به شدت اثبات کرد (De Villiers et al., 2014; Dumay et al., 2016 ). در سال 2009، در سال 2009، King-III آماده سازی یک گزارش یکپارچه را ایجاب کرد که "یک بازنمایی کل نگر و یکپارچه از عملکرد شرکت بر حسب هم فایننس و هم دوام پذیری آن" ارائه می دهد (IOD, 2009). آفریقای جنوبی در سال 2009 اولین حوزۀ حوزۀ قضایی شد که شرکت های موجود در لیست را ملزم کرد تا یک گزارش یکپارچه براساس complyor-explain به همرا اولین مقالۀ بحث که مولفه های یک گزارش یکپارچه منتشر شده در سال 2011 طرح ریزی کرده بود ارائه دهند(IRCSA, 2011).

پیشرفت های مهمی تقریبا در همان زمان در انگلیس و امریکا در حا وقوع بود. در سپتامبر سال 2009، سر مایکل پیت (از پروژۀ حسابداری دوام پذیری شاه ولز )، پاول دروکمان ( از Global Reporting Initiative (GRI)) و مروین کینگ ( پس از وی کدهای راهبری شرکتی آفریقای جنوبی گفته می شوند) برای توضیح و بحث در مورد شیوۀ یکپارچه سازی انواع مختلف گزارشاتی که معمولا توسط سازمان های بزرگ تولید می شوند با هم ملاقات کردند (Dumay et al., 2016). در سال 2010، مراکز آکادمیک وابسته به هاروارد دیدگاه های خود پیرامون IR به عنوان ابزار تشریح تأثیر منابع مالی و غیرمالی بر یکدیگر ارائه دادند (Eccles and Krzus, 2010; Eccles و Serafeim, 2014). کمیتۀ بین المللی گزارشگری یکپارچه که بعدها به شورای بین المللی گزارشگری یکپارچه (IIRC) تغییر نام داد در سال 2010 بنیانگذاری شد و اولین چهارچوب بین المللی خود در خصوص IR را در سال 2013 منتشر کرد (به IIRC, 2013 مراجعه کنید).

هدف IR را می توان به صورت زیر خلاصه کرد:

IR یک رویکرد منجسم تر و کارامد جهت گزارشگری شرکتی ارتقا می دهد و هدفش ارتقای کیفیت اطلاعات موجود برای فراهم کنندگان سرمایۀ مالی در راستای امکان تخصیص کارآمدتر و مولدتر سرمایه می باشد. هدف اولیه یک گزارش یکپارچه این است که به فراهم کنندگان سرمایۀ مالی توضیح دهند که یک سازمان در طول به ارزش می رسد (IIRC, 2013، ص 4).

ثابت شده که تهیۀ یک گزارش یکپارچۀ باکیفیت چالش آور است. افشاهای نوعی و تکراری ارتباط ارزشی گزارشات را از اساس تخریب می کند. شرکت ها تلاش می کردند تا استراتژیف خرات و مدیریت سرمایه های غیرمالی خود را به وضوح گزارش کنند (PwC, 2015). ارتباط بین چیزی که سازمان ها گزارش می دهند و چه روشی برای مدیریت و عملیاتی سازی دارند نیز مورد بحث و سئوال بوده است (Brown and Dillard, 2014؛ Stubbs and Higgins, 2014). شاید قابل توجه تر از همه این واقعیت است که IR همچنان متمرکز بر فراهم کنندگان سرمایۀ مالی است، انتقاد برجسته ای که IR تعهدی به جوابگویی و دوام پذیری اصیل ندارد (Milne و Gray، 2013؛ Flower, 2015).

در این مقاله مزیت این انتقادات یا پتانسیل تغییر IR به بحث گذاشته نمی شود. در عوض، بر ساخت یک مدل مفهومی جهت بیان چهارچوب تحقیقات IR که حتمی هستند تمرکز خواهد شد. بدنۀ وسیع و عظیم پژوهش های IR را می توان به شیوۀ منسجم تر با این مدل به صورت فرمول یا چهارچوبی سازمان یافته ارائه داد. توسعۀ مدل در بخش بعد توضیح داده خواهد شد.

یک مدل مفهومی تأثیرات حول گزارشگری یکپارچه

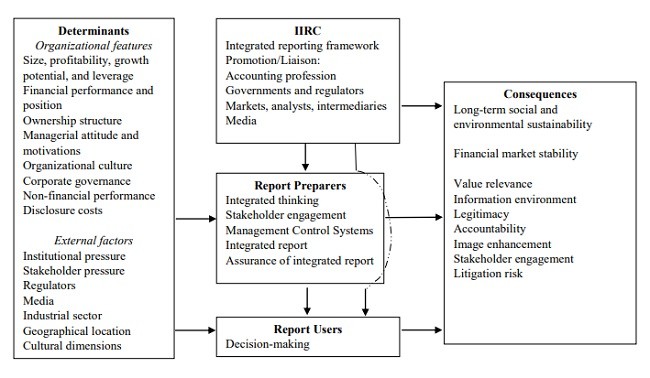

در شکل 1 یک مدل مفهومی از کل پروسۀ IR ارائه شده است. این مدل جامع است و و منشا آن در یکی از روش های حسابداری است که محققان حسابداری در گذشته تحقیقات خود در مورد گزارشگری مفهوم سازی کرده اند: بر اساس دترمینان های انتخاب های خاص حسابداری و پیامدهای آن (Alraziet al., 2015; De Villiers and Maroun, 2017). این مدل براساس ادبیات IR است و شامل پروسه های داخلی کاربران و IIRC است.

روی هم رفته، این مدل 1) دترمینان های بالقوۀ IR را شناسایی می کند 2) پروسه های و تأثیرات IIRC را تصدیق می کند 3) پروسۀ IR سازمان را منعکس می کند 3) تأثیر بالقوۀ IR و کاربرد خارجی گزارشات یکپارچه را نشان می دهد و 4) پیامدهای احتمای ناشی از IR را شناسایی می کند. پیکان های موجود در این مدل جهت تأثیرات سببی اصلی است. بااینحال، سبب ممکن است در جهت عکس باشد مثل کاربران گزارش که بر تهیه کنندگان گزارش تحت شرایط قطعی تأثیر می گذارند. مفاهیم درون هر کادر نیز می توانند بر یکدیگر تأثیر بگذارند. به عنوان مثل، در کادر تهیه کنندگان گزارش، تفکر یکپارچه ممکن است منجر به دخالت و تعهد سهامدار گردد که بر سیستم های کنترل مدیریت منتخب جهت پشتیبانی گزارش یکپارچه که منتشر می شود تأثیر می گذارد و به نوبۀ خود منجر به تضمین گزارش یکپارچه می شود. به هر روی، جریان تضمین می تواند با پافشاری تهیه کنندگان تضمین بر شواهد شنیداری بر مدیریت تأثیر بگذارد. برخی روابط موجود در این مدل براساس مزایای اظهار شدۀ IIRC گزارشگری یکپارچه و برخی برساس تئوری می باشد در حالی که سایر رابط مورد تأیید شواهد تجربی هستند. از انجا که IR یک حوزۀ نوظهور است، انتظار می رود این مدل در مقام شواهد تجربی جدید ارائه گردد.

Abstract

Purpose:

This article develops a conceptual model for examining the development of integrated reporting, relates the articles in this Meditari Accountancy Research special issue on integrated reporting to the model, and identifies areas for future research.

Design/methodology/approach:

The article uses a narrative/discursive style to summarise key findings from the articles in the special issue and develop a normative research agenda.

Findings:

The findings of the prior literature, as well as the articles in this special issue, support the conceptual model developed in this article. This new conceptual model can be used in multiple ways.

Originality/value:

The special issue draws on some of the latest developments on integrated reporting from multiple jurisdictions. Different theoretical frameworks and methodologies, coupled with primary evidence on integrated reporting experience, construct a pluralistic assessment of integrated reporting which can be used as a basis for future research. The new conceptual model developed in this article can be used as an organizing framework, a way of understanding and thinking about the various influences, a way of identifying additional factors to control for in a study, and/or a way to identify new, interesting, and underexplored research questions.

Introduction

Integrated reporting (IR) started in practice in the early years of the millennium. It was a response to the global financial crisis and string of corporate failures which undermined confidence in conventional financial statements and highlighted the limitation of retrospective reporting on a single measure of organisational performance (IIRC, 2013). The weaknesses in sustainability reporting were also relevant. Traditional sustainability reports presented environmental, social and governance (ESG) disclosures separately from financial information and did not always explain the interconnection between strategy, risks and the multiple forms of capital under an organisation‟s control (De Villiers et al., 2014, 2017).

In this context, IR represented an evolution of the provision of social environmental and financial information in a format where the different kinds of disclosures are interconnected (De Villiers et al., 2014, 2017; Solomon and Maroun, 2012). Grounded in an integrated thinking philosophy, IR can be seen as a call for transparent and responsible business management and reporting, aiming to provide better quality information that explains the interconnection between social, environmental, and economic dimensions of an organisation, to improve the quality of information provided to stakeholders and to promote sustainable business practices (Maroun and De Villiers, 2017).

Arguably, the beginning of IR can be traced to the release of King-I in 1994. King-I was developed in South Africa in response to the need to establish the credibility of the local capital market and provide a stakeholder-centric model for holding companies accountable for their performance. It was followed by the release of King-II in 2002, which firmly established the idea of reporting on social, environmental and economic activity and South Africa‟s leading role in corporate governance and reporting (De Villiers et al., 2014; Dumay et al., 2016). In 2009, King-III called for the preparation of an integrated report, which provides “a holistic and integrated representation of the company‟s performance in terms of both its finance and its sustainability” (IOD, 2009). In 2010, South Africa became the first jurisdiction to require listed companies to prepare an integrated report on a complyor-explain basis, with the first discussion paper outlining the elements of an integrated report published in 2011 (IRCSA, 2011).

A number of important developments were taking place in the UK and the USA at roughly the same time. In September 2009, Sir Michael Peat (of the Prince of Wales‟ Accounting for Sustainability Project (A4S)), Paul Druckman (of the Global Reporting Initiative (GRI)) and Mervyn King (after whom South African codes of corporate governance are named) met in London to discuss how to integrate the multiple types of reports typically produced by large organisations (Dumay et al., 2016). During 2010, Harvard-based academics presented their views on IR as a means of explaining the impact of financial and non-financial resources on each other (Eccles and Krzus, 2010; Eccles and Serafeim, 2014). The International Integrated Reporting Committee, later renamed the International Integrated Reporting Council (IIRC), was formed in 2010 and issued the first international framework on IR in 2013 (see IIRC, 2013).

The objective of IR can be summarised as:

IR “promotes a more cohesive and efficient approach to corporate reporting and aims to improve the quality of information available to providers of financial capital to enable a 3 more efficient and productive allocation of capital… The primary purpose of an integrated report is to explain to providers of financial capital how an organization creates value over time.” (IIRC, 2013, p.4)

Preparing a high quality integrated report has proven challenging. Repetition and generic disclosures undermine the value relevance of the reports (Solomon and Maroun, 2012). Companies have struggled to report clearly on their strategy, risks and the management of non-financial capitals (PwC, 2015). The connection between what organisations report and how they are actually managed/operated has also been questioned (Brown and Dillard, 2014; Stubbs and Higgins, 2014). Perhaps most significant is the fact that IR remains focused on the providers of financial capital, leading critiques that IR lacks a commitment to genuine accountability and sustainability (Milne and Gray, 2013; Flower, 2015).

This article does not debate the merit of these criticisms or the change potential of IR. Instead, the article focuses on constructing a conceptual model to frame the IR research that has emergence. The large and expanding body of IR research can be presented in a more coherent fashion with this model as the organising frame. The development of the model is discussed in the next section.

A conceptual model of influences around Integrated Reporting

Figure 1 presents a conceptual model of the overall IR process. This model is general in nature and finds its origins in one of the ways accounting researchers have traditionally conceptualized research on reporting: in terms of determinants of certain accounting choices and their consequences (Alrazi et al., 2015; De Villiers and Maroun, 2017). The model is based on the IR literature and includes the IIRC‟s and users‟ internal processes.

Overall, the model: (1) identifies potential determinants of IR, (2) acknowledges the IIRC‟s processes and influences, (3) reflects organisation‟s IR process, (3) shows the potential effect of IR and external use of integrated reports, and (4) identifies possible consequences arising from IR. The arrows in the model show the direction of the main causal effects. However, causation may run in the reverse direction, such as report users influencing report preparers under certain circumstances. The concepts within each box can also influence each other. For example, within the report preparers‟ box, integrated thinking may lead to stakeholder engagement, which may influence the management control systems chosen to support the integrated report that is published, which may in turn lead to assurance of the integrated report. However, the assurance process can influence the management control systems through the insistence of assurance providers on „auditable‟ evidence. Some of the relationships in the model are based on the IIRC‟s stated advantages of IR and some on theory, while others have been backed up by empirical evidence. As IR is an emerging field, the model is expected to evolve as new empirical evidence moves our current patchwork of knowledge to more solid and shared understandings.

چکیده:

مقدمه

یک مدل مفهومی تأثیرات حول گزارشگری یکپارچه

پشتیبانی مدل مفهومی گزارشگری یکپارچه از ادبیات موجود

دترمینان ها

IIRC

تهیه کنندگان گزارش

کاربران گزارش

پیامدها

سهم این ویژه نامه در درک مدل مفهومی گزارش دهی یکپارچه

تهیه کنندگان گزارش

کاربران گزارش

پیامدها

نتیجه گیری و الگوهایی برای تحقیقات آتی حول گزارش دهی یکپارچه

Abstract

Introduction

A conceptual model of influences around Integrated Reporting

Backing for the Conceptual model for Integrated Reporting from the literature

Determinants

IIRC

Report preparers

Report users

Consequences

Contributions of this special issue to our understanding of the Conceptual model

for Integrated Reporting

Report preparers

Report users

Consequences

Conclusion and directions for future research on Integrated Reporting

References