دانلود رایگان مقاله بررسی مطالعات اثر رویداد کوتاه مدت در عملیات و مدیریت زنجیره تامین

چکیده

متد مطالعه اثر رویداد کوتاه مدت ، که زمینهای برای فرضیه بازار کارآمد بود، یکی از ابزارهایی است که به صورت گسترده برای سنجش تاثیر یک رویداد خاص بر ارزش سهامداران شرکت استفاده میشود. از آنجا که متد مطالعه اثر رویداد کوتاه مدت به شدت توسط محققین در راستای بررسی رویدادهای مربوط به عملیات و مدیریت زنجیره تامین (OSCM) گوناگون استفاده میشود، وقت آن رسیده است که یک بررسی سیستماتیک بر این متد از نظر اینکه چگونه این متد در ادبیات موضوعی OSCM استفاده شده است و برای استفاده در پژوهش OSCM آینده چگونه میتواند بهبود بخشیده شود، انجام دهیم. با تحلیل 29 مطالعه بر اثر رویداد کوتاه مدت که در ژورنالهای OSCM بین سالهای 1995 و 2017 منتشر شده است، دریافتیم که محققین OSCM معمولا از رویههای استانداردی در انجام مطالعات اثر رویداد تبعیت میکنند، اما توجه کمی به برخی از مسائل متدلوژیکال مانند بررسی رویدادهای مبهم برای بسط پنجرههای رویداد دارند. بر اساس این تحلیل، چند توصیه را برای مطالعات رویداد آینده در OSCM ارائه میدهیم، مانند فرصتی برای مطالعه رویدادهای خارجی در موارد غیر امریکایی، احتیاط در گسترش پنجرههای رویداد، و نیاز به پرداختن به سوگیریهای خود انتخاب.

1. مقدمه

در طی چند دهه گذشته، شناخت در حال رشدی از اهمیت استراتژیک عملیات و مدیریت زنجیره تامین (OSCM) در ایجاد ارزش سهامداران بوجود آمد. OSCM از طریق مکانیزم رشد درآمد، کاهش هزینه عملیاتی، و استفاده کارآمد از سرمایه در حال کار و ثابت، نقش مهمی را در ایجاد ارزش سهامداران بازی میکند (Martin and Lynette, 1999). به دنبال این منطق نظری، محققین مطالعات تجربی گوناگونی را برای تحلیل ارتباط بین OSCM و ارزش سهامداران انجام دادند، که در میان آنها متد مطالعه اثر رویداد یکی از متداول ترین متدلوژیهایی بود که در ادبیات موضوعی پذیرفته شد. با زمینه شدن به فرضیه بازار کارآمد (Malkiel and Fama,1970)، متد مطالعه اثر رویداد کوتاه مدت بر این وعده متکی است که ارزش اطلاعات بازار اغلب کاملا در قیمت سهام در بازارهای مالی منعکس خواهد شد. با تشخیص تغییرات غیرعادی قیمت سهام در پاسخ به اطلاعات بازاری جدید موجود در بازار مالی، متد مطالعه بر اثر رویداد کوتاه مدت محققین را قادر کرد که تاثیر یک رویداد خاص بر ارزش سهامداران شرکتی را بسنجند (MacKinlay, 1997).

با شهرت رو به رشد این متد در ادبیات موضوعی OSCM، متد مطالعه اثر رویداد کوتاه مدت توسط پژوهشگران برای بررسی موضوعات OSCM گوناگون مانند اختلالات زنجیره تامین (Hendricks and Singhal, 1997; Zhao et al., 2013)، مدیریت محیط (Jacobs,2014; Klassen and McLaughlin, 1996)، و مدیریت کیفیت (Lin and Su, 2013; McGuire and Dilts, 2008) استفاده شد. علاوه بر این، مطالعات اثر رویداد کوتاه مدت در نتیجه پیشرفت در مدلهای قیمت گذاری دارایی و تحلیل آماری در حال تکامل است. این متد برای بررسی مسائل آماری بالقوه خاص محیطهای پژوهشی متفاوت اصلاح شده است (Fama and French, 2015; Kothari and Warner, 2007). در بررسی شهرت فزاینده و بهبودهای متدلوژیکال اخیر، وقت آن است که یک بررسی سیستماتیک بر این متد انجام دهیم و بررسی کنیم که چگونه در ادبیات موضوعی OSCM اجرا میشود و برای استفاده در مطالعات OSCM آینده چگونه میتواند بهبود بخشیده شود.

با بررسی بر 29 مطالعه در زمینه اثر رویداد کوتاه مدت منتشر شده در ژورنالهای OSCM بین سالهای 1995 تا 2017، به مشاهداتی دست یافتیم: (1) اکثریت مطالعات اثر رویداد کوتاه مدت در OSCM بر رویدادهای داخلی شرکت در امریکا تمرکز میکنند. (2) در حالی که بیشتر مطالعات، پنجره رویداد استاندارد را حول سه روز رویداد تنظیم کردند، برخی مطالعات پنجره رویداد طولانی تری داشتند. (3) پژوهشگران اغلب برای شناسایی رویدادهای تحت مطالعه بر منابع داده متعدد تکیه کردهاند، و کمتر به مسائل رویدادهای مبهم توجه کردهاند. (4) مدل بازار یک مدل تخمین مشهور در ادبیات OSCM است، اما برخی از پژوهشگرن از مدلهای تخمین متعددی برای افزایش مقاومت تحلیل استفاده کرده اند. (5) پژوهشگران در مورد نقضهای ممکن فرضیات برای آزمون معنی دار بودن محتاط بودند، لذا اصلاحات گوناگون آزمون-t سنتی را در زمینههای پژوهشی متفاوت میپذیرفتند. (6) محققین اغلب رگرسیون متقابل متوالی و ANOVA را برای کاهش عوامل تعیین کننده عملیاتی تغییرات در بازدههای غیرعادی انجام میدادند.

بر اساس این تحلیل، چند توصیه گوناگون را برای مطالعات اثر رویداد آینده در OSCM ارائه میدهیم. ابتدا، استدلال کردیم که محققین OSCM مزایای رویدادهای خارجی را برای شرکتهای مرتبط و مواردی که خارج از زمینه امریکا رخ میدهد در نظر میگیرند، و درک ما از تاثیر مالی این رویدادهای تحت مطالعه را ارتقا میبخشند. دوم، محققین باید در مورد بسط پنجرههای رویداد دقت کنند، و بررسیهای نظری را برای توجیه طولهای پنجره ارائه دهند. سوم، حذف تاثیرات مبهم، یک مرحله مهم در انجام مطالعات اثر رویداد کوتاه مدت است. چهارم، از سوگیری خود انتخاب نباید چشم پوشی شوند، به خصوص زمانی که رویداد تحت مطالعه توسط شرکتها به صورت داوطلبانه اغاز میشوند. پنجم، استفاده از مدلهای جایگزین برای تخمین بازدههای مورد انتظار میتواند مقاومت تحلیل را افزایش دهد. ششم، اصلاحات آزمون-t سنتی در برخی از محیطهای پژوهشی مانند مطالعه اثر رویداد خارجی و مطالعات خاص صنعت ضروری هستند. سرانجام، استقلال یک فرض مهم در آزمون معنی دار بودن بازدههای غیرعادی تجمعی است. این بنابراین برای بررسی مسائل بروز کرده از خوشه بندی صنعتی و زمانی مهم است.

پژوهش ما از چند نظر مهم است. ابتدا، به عنوان راهنمای عملی برای محققین OSCM علاقمند به استفاده از متد مطالعه اثر رویداد کوتاه مدت در پژوهش آنها استفاده میشود. ما مراحل دقیق انجام یک مطالعه رویداد کوتاه مدت را مستند کردیم و بر برخی از مسائل مشترکی که در هر مرحله با آنها مواجه میشویم بحث میکنیم، بنابراین محققین OSCM قادر هستند که درک بهتری از اینکه چگونه مطالعه اثر رویداد کوتاه مدت باید انجام شود داشته باشند. به هر حال، تا انجا که میدانیم، این اولین بررسی مقایسهای از مطالعات اثر رویداد در ادبیات OSCM است. با توجه به شیوع بیشتر مطالعات اثر رویدادی در OSCM، ارائه یک بررسی بر حالت جاری دانش و بهترین شیوههای پذیرفته شده در ادبیات OSCM ضروری است. سرانجام، پژوهش ما چند مسئله طراحی پژوهشی مهم را شناسایی میکند که اغلب توسط محققین مطالعه اثر رویداد کوتاه مدت گذشته در OSCM چشم پوشی شده اند، و همچنین برخی از فرصتهای نوظهور خاص زمینه OSCM هستند، لذا به پیشرفت پذیرش متد مطالعه رویداد برای پژوهش OSCM کمک میکنند.

2. بررسی بر ادبیات موضوعی

اولین مطالعه رویداد گزارش شده در ادبیات موضوعی شاید توسط James Dolley در سال 1933 انجام شده باشد. بر اساس یک نمونه از 95 سهام از سال 1921 تا 1931، Dolley (1933) تغییرات قیمت سهام اسمی را در زمان تجزیه سهام بررسی کردند. مطالعات اثر رویداد مدرن در دو مورد از کارهای پیشگامانه Ball and Brown (1968) و Fama و همکاران (1969) اغاز شدند. مطالعات اثر رویدادی مهم در گروههای متفاوتی از نظر طول پنجره رویداد و سنجش عملکرد توسعه یافتند. مطالعات اثر رویداد بلند مدت بازدههای سهام غیرعادی را در طول یک دوره معمول از یک تا هشت سال با بازده غیرعادی پرتفوی تقویم-زمانی (CTAR) یا بازده غیرعادی خرید و نگهداشت (BHAR) (Barber and Lyon, 1997; Lyon et al., 1999) تشخیص دادند، در عین حال مطالعات اثر رویداد کوتاه مدت بازدههای سهام غیرعادی را در یک طول پنجره حداکثر 40 روز بررسی کردند (Brown and Warner, 1985; MacKinlay, 1997). یک تعریف گسترده تر از مطالعه اثر رویداد به فراتر از دامنه واکنش بازار سهام میرود چرا که دیگر نتایج سطح شرکتی مانند عملکرد عملیاتی را میسنجد (Barber and Lyon, 1996). در موازات با پیشرفت در مدلهای قیمت گذاری دارایی و تحلیل آماری، متد مطالعه اثر رویداد هنوز برای حساب کردن انحرافات ممکن از فرضیات اصلی در حال تکامل است. به هر حال، مفهوم مطالعات اثر رویداد مدرن همچنان همان است، که اهمیت بازدههای غیرعادی تجمعی و میانگین اوراق بهادار نمونه را حول دوره رویداد اندازه میگیرد (Kothari and Warner, 2007).

در اصل با استفاده از این متد در حسابداری و امور مالی، مطالعه اثر رویداد کاربرد خود را تقریبا در همه رشتههای تجاری از جمله مدیریت، سیستمهای اطلاعاتی، بازاریابی، مدیریت زنجیره تامین و عملیات بسط داده است. برای مثال، در ادبیات موضوعی بازاریابی، محققین متد مطالعه اثر رویداد را برای بررسی تاثیر مالی رویدادهای بازاریابی با انتشار محصول جدید، انتساب CMo، خرید و فروش برند، و افزودن کانال اینترنتی میپذیرند (Sorescu et al., 2017)، در حالی که رویدادهایی که توجه پژوهشگران سیستمهای اطلاعاتی را به خود جلب کرده است شامل برون سپاری IT، سرمایه گذاری IT، جوایز برتری IT، آسیب پذیری نرم افزری و نقض امنیت است (Konchitchki and O'Leary, 2011).

جدول 1 بررسیهای مطالعات اثر رویداد ادبیات موضوعی گذشته را در رشتههای تجاری متفاوت بررسی کرده است. این جدول نشان میدهد که بررسیهای ادبیات موضوعی در حسابداری و امور مالی بر مبانی آماری و اقتصادی تاکید دارد و راهنماهایی را برای کاربرد در این زمینهها ارائه میدهد. برای نمونه، MacKinlay (1997) و Binder (1998) استفاده از مطالعات اثر رویداد را در امور مالی، که در رویههای استاندارد برای مطالعات اثر رویداد نشان داده شده است را بررسی کردند، و بر قدرت تحلیل و تحلیل رگرسیون متعاقب بحث کردند. Corrado (2011) تغییراتی را در متد مطالعه پایه برای تنظیماتی برای نوسانات ناشی از رویداد، و غیر عادی بودن و مقیاسهای مقطعی بررسی کردند. Kothari and Warner (2007) یک بررسی جامع را بر بیش از 500 مطالعه انجام شده در پنج ژورنال حسابداری و مالی برتر از سال 1974 تا 2005 انجام دادند. آنها دریافتند که ویژگیهای مطالعات اثر رویداد بررسی شده بسته به دوره زمانی و مشخصههای شرکت نمونه متفاوت بودند. آنها همچنین نشان دادند که، در مقایسه با مطالعات اثر رویداد کوتاه مدت، مطالعات اثر رویداد بلند مدت از چند محدودیت مهم رنج میبرند.

با تکامل متد مطالعه در طول زمان، ویژگیهای آماری آن به خوبی تعریف شدند و کاربردهای آن به صورت گسترده شناخته شدند. بررسیهای ادبیات موضوعی در دیگر رشتههای تجاری تاکید بیشتری بر مسائل طراحی پژوهشی و تفسیرهای اقتصادی نتایج مطالعه دارد. McWilliams and Siegel (1997) یک بررسی بر 29 مطالعه اثر رویداد در شش ژورنال مدیریتی برتر از سال 1986 تا 1995 انجام دادند. آنها بر چندین نگرانی متعدد در مورد اعتبار مفروضات و مسائل طراحی پژوهشی بحث کردند. با تکرار سه مطالعه در مدیریت با طراحیهای پژوهشی جایگزین، آنها توجهات کافی را به سمت نگرانیهای فوق الذکر جلب کردند. آنها نشان دادند که بازدههای غیر عادی تنها تاثیر بر ثروت سهامداران را، به جای رفاه همه سهامداران منعکس میکنند. Konchitchki and O'Leary (2011) استفاده از متد مطالعه اثر رویداد را بر بیش از 50 مطالعه سیستم اطلاعاتی بررسی کردند. آنها بر مسائل طراحی پژوهشی بدون بررسی نتایج حقیقی و نتایج کلی در مطالعات خاص تمرکز کردند. Sorescu و همکاران (2017) بیش از 40 مطالعه اثر رویداد منتشر شده در ژورنالهای بازاریابی را شناسایی کردند که شامل لیستی از 50 ژورنال کسب و کار برتر مالی هستند. علاوه بر طراحیهای پژوهشی، بررسیهای آنها تفسیری از مطالعات اثر رویداد را ارائه دادند. آنها نتیجه گیری اقتصادی از مطالعات اثر رویداد را با خلاصه کردن یافتههای اصلی و عوامل تعیین کننده مشترک بازدههای غیرعادی را در ادبیات بازاریابی ارائه دادند.

ABSTRACT

The short-term event study method, grounded in the Efficient Market Hypothesis, is one of the most widely used tools for quantifying the impact of a specific event on a firm's shareholder value. As the short-term event study method has been increasingly employed by researchers to investigate various operations and supply chain management (OSCM) events, it is timely to conduct a systematic review of the method to examine how it has been implemented in the OSCM literature and what could be improved to deploy it for future OSCM research. Analyzing 29 short-term event studies published in renowned OSCM journals between 1995 and 2017, we find that OSCM researchers generally follow the standard procedures in conducting event studies, but pay less attention to some methodological issues ranging from addressing the confounding events to expanding the event windows. Based on our analysis, we provide several recommendations for future event studies in OSCM, such as the opportunity for studying external events in the non-U.S. context, the caution of expanding the event windows, and the need to deal with the self-selection bias.

1. Introduction

Over the past few decades, there is growing recognition of the strategic importance of operations and supply chain management (OSCM) in creating shareholder value. OSCM plays a vital role in generating shareholder value through the mechanisms of revenue growth, operating cost reduction, and efficient use of fixed and working capital (Martin and Lynette, 1999). Following this theoretical logic, researchers have conducted various empirical studies to analyze the connection between OSCM and shareholder value, among which the event study method represents one of the most popular methodologies adopted in the literature. Grounded in the Efficient Market Hypothesis (Malkiel and Fama, 1970), the short-term event study method relies on the premise that the value of market information will be reflected almost completely in the equity prices in financial markets. By detecting the abnormal equity price changes in response to new market information available in the financial market, the short-term event study method enables researchers to quantify the impact of a specific event on a firm's shareholder value (MacKinlay, 1997).

With its growing popularity in the OSCM literature, the short-term event study method has been employed by researchers to investigate various OSCM topics such as supply chain disruptions (Hendricks and Singhal, 1997; Zhao et al., 2013), environmental management (Jacobs, 2014; Klassen and McLaughlin, 1996), and quality management (Lin and Su, 2013; McGuire and Dilts, 2008). In addition, short-term event studies in OSCM are evolving as a result of advances in asset pricing models and statistical analysis. The method has been modified to address potential statistical issues specific to different research settings (Fama and French, 2015; Kothari and Warner, 2007). In view of its increased popularity and recent methodological improvements, it is timely to conduct a systematic review of the method to examine how it has been implemented in the OSCM literature and what could be improved to deploy it for future OSCM research.

Reviewing 29 short-term event studies published in renowned OSCM journals between 1995 and 2017, we have the following observations: (1) The majority of the short-term event studies in OSCM focus on internal corporate events in the U.S. context. (2) While most studies set standard event windows including at most three days around the event, theoretical justifications are not commonly provided for short-term event studies with longer event windows. (3) Researchers often rely on multiple data sources to identify the events under study, but pay less attention to the issue of confounding events. (4) The market model is the most popular estimation model in the OSCM literature, but some researchers also employ multiple estimation models to increase the robustness of the analysis. (5) Researchers are wary of possible violations of the assumptions for the significance test, so adopting various modifications of the traditional t-test according to different research contexts. (6) Researchers often conduct subsequent cross-sectional regression and ANOVA to probe into the operational determinants of variations in abnormal returns.

Based on our analysis, we provide several recommendations for future event studies in OSCM. First, we urge OSCM researchers to take advantage of events external to the firms concerned and occurring outside the U.S. context, advancing our understanding of the financial impacts of these under-studied events. Second, researchers should be careful about expanding the event windows, and provide theoretical explanations to justify the window lengths. Third, removing confounding effect is a critical step in conducting short-term event studies. Fourth, the possible self-selection bias should not be ignored, especially when the events under study are initiated by firms voluntarily. Fifth, employing alternative models to estimate the expected returns could enhance the robustness of the analysis. Sixth, modifications of the traditional t-test might become necessary in some research settings such as external events and industry-specific studies. Finally, independence is a vital assumption in testing the significance of cumulative abnormal returns. It thus is important to address the issues arising from time and industry clustering.

Our research is important in several ways. First, it serves as a practical guide for OSCM researchers interested in employing the short-term event study method in their research. We document the detailed steps of conducting a short-term event study and discuss some common issues encountered in each step, thus enabling OSCM researchers to have a better understanding of how a short-term event study should be conducted. Moreover, to the best of our knowledge, this is the first comprehensive review of event studies in the OSCM literature. Given the increased prevalence of event studies in OSCM, it is imperative to provide an overview of the current state of knowledge and best practices adopted in the OSCM literature. Finally, our research identifies several important research design issues that are often ignored by researchers of past shortterm event studies in OSCM, as well as some emerging opportunities specific to the OSCM context, so helping advance the adoption of the event study method for OSCM research.

2. Literature review

The first event study reported in the literature was perhaps conducted by James Dolley in 1933. Based on a sample of 95 stock splits from 1921 to 1931, Dolley (1933) investigated the nominal stock price changes at the time of the stock splits. Modern event studies were initiated in the two seminal works of Ball and Brown (1968) and Fama et al. (1969). Modern event studies are developed into different categories in terms of the event window length and performance measurement. Long-term event studies detect abnormal stock returns over a period normally ranging from one to eight years with calendar-time portfolio abnormal return (CTAR) or buy-and-hold abnormal return (BHAR) (Barber and Lyon, 1997; Lyon et al., 1999), while short-term event studies examine abnormal stock returns over a maximum window length of 40 days (Brown and Warner, 1985; MacKinlay, 1997). A broader definition of event study goes beyond the scope of stock market reaction as it also measures other firm-level outcomes such as operating performance (Barber and Lyon, 1996). In parallel with advances in asset pricing models and statistical analysis, the event study method is still evolving to account for possible deviations from the fundamental assumptions. However, the gist of modern event studies remains the same, which is measuring the significance of sample securities' mean and cumulative abnormal returns around an event period (Kothari and Warner, 2007).

Originally applied in accounting and finance, the event study method has expanded its application to virtually all the business disciplines including management, information systems, marketing, operations and supply chain management (MacKinlay, 1997; McWilliams and Siegel, 1997). For example, in the marketing literature, researchers adopt the event study method to examine the financial impact of such marketing events as new product release, CMO appointment, brand acquisition and disposal, and Internet channel addition (Sorescu et al., 2017), while events attracting information systems researchers' attention include IT outsourcing, IT investment, IT excellence award, software vulnerability, and security breaches (Konchitchki and O'Leary, 2011).

Table 1 summaries previous literature reviews of event studies in different business disciplines. It indicates that the literature reviews in accounting and finance emphasize the econometric and statistical fundamentals and provide guidelines for applications in other fields. For instance, MacKinlay (1997) and Binder (1998) reviewed the use of event studies in finance, outlined the standard procedures for conducting event studies, and discussed the power of analysis and the subsequent regression analysis. Corrado (2011) reviewed variations in the basic short-term event study method to adjust for non-normality, event-induced volatility, and cross-sectional weighting. Kothari and Warner (2007) conducted a comprehensive survey of over 500 studies published in five of the top finance and accounting journals from 1974 to 2005. They found that the properties of the event studies reviewed were different depending on the time period and sample firm characteristics. They also indicated that, compared with short-term event studies, long-term event studies suffer from several important limitations.

As the event study method evolves over time, its statistical properties become well-defined and its applications are widely acknowledged. Literature reviews in other business disciplines place a greater emphasis on the research design issues and economic interpretations of the study results. McWilliams and Siegel (1997) conducted a survey of 29 event studies in three of the top management journals from 1986 to 1995. They discussed several concerns about the validity of the assumptions and research design issues. By replicating three studies in management with alternative research designs, they called for adequate attention towards the aforementioned concerns. They also indicated that the abnormal returns only reflect the effect on the shareholder wealth, rather than the welfare of all the stakeholders. Konchitchki and O'Leary (2011) examined the use of the event study method in over 50 information systems studies. They focused on the research design issues without investigating the actual results and conclusions in specific studies. Sorescu et al. (2017) identified over 40 event studies published in the marketing journals included in the list of Financial Times' 50 top business journals. In addition to research designs, their review examines interpretations of event studies as well. They provided economic inferences from the event studies by summarizing the main findings and common determinants of abnormal returns in the marketing literature.

چکیده

1. مقدمه

2. بررسی بر ادبیات موضوعی

3. دامنه این پژوهش

4. دادهها

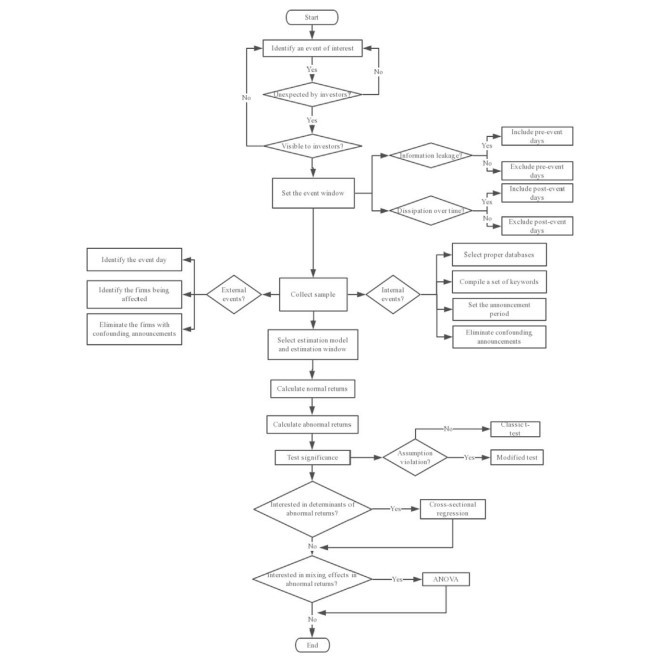

5. شیوههای جاری مطالعات اثر رویداد کوتاه مدت در OSCM

5.1 شناسایی یک رویداد مورد نظر

5.2 پنجره رویداد

5.3 جمع اوری داده

5.4 پیش بینی بازدههای نرمال

5.5 تست بازدههای غیر عادی

5.6 تحلیل مقطعی

6. توصیههایی برای مطالعات اثر رویداد کوتاه مدت در آینده در OSCM

6.1 رویدادهای خارجی و غیر امریکایی

6.2 تنظیم پنجره رویداد

6.3 اعلانهای مبهم

6.4 سوگیری خود انتخابی

6.5 مدل تخمین

6.6 آزمون معنی دار بودن

6.7 خوشه بندی صنعتی و زمانی

7. نتایج و محدودیت ها

منابع

ABSTRACT

1. Introduction

2. Literature review

3. The scope of this research

4. Data

5. Current practices of short-term event studies in OSCM

5.1. Identify an event of interest

5.2. Event window

5.3. Collect data

5.4. Predict normal returns

5.5. Test abnormal returns

5.6. Cross-sectional analysis

6. Recommendations for future short-term event studies in OSCM

6.1. External events and non-U.S. context

6.2. Justify the event window

6.3. Confounding announcements

6.4. Self-selection bias

6.5. Estimation model

6.6. Significance tests

6.7. Time and industry clustering

7. Conclusions and limitations

References