دانلود رایگان مقاله رابطه بین عوامل ریسک کنترل و ریسک ذاتی و تعدیلات حسابرسی

خلاصه

در این مقاله به تجزیه و تحلیل این موضوع خواهیم پرداخت که آیا تعدیلات حسابرسی از نظر سیستماتیک با ریسکهای کنترل و ذاتی متفاوت است یا خیر. تجزیه و تحلیل این مقاله بر اساس دادههای مالکیت یک نمونه جدید بزرگ از تعدیلات حسابرسی یافتشده در حسابرسی صورتهای مالی توسط شرکت حسابرسی چهار بزرگ در آلمان است. ما محدوده مطالعات پیشین را با ترکیب برنامهریزی اهمیت مختص مشتری در طرح خود گسترش دادیم و این موضوع ما را قادر ساخت تا مقدار نسبی تعدیلات را مورد تجزیه و تحلیل قرار دهیم. یافتههای ما نشان میدهد که تعدیلات حسابرسی از نظر سیستماتیکی متفاوت است و این موضوع توسط مدل ریسک حسابرسی مطرح شده است. به طور خاص، صداقت و صلاحیت مدیریت مشتری، موقعیت اقتصادی، قدرت کنترل سطح واحد تجاری و سیستم کنترل داخلی با تعداد و مقدار نسبی تعدیلات حسابرسی در ارتباط است. نتایج همچنین پیشنهاد میدهند که عوامل ریسک کنترل و ریسک ذاتی بهشدت با تعدیلات تاثیرگذار بر سود در ارتباط هستند.

مقدمه

در این مقاله به تجزیه و تحلیل این موضوع خواهیم پرداخت که آیا تعدیلات حسابرسی از نظر سیستماتیک با ریسکهای کنترل و ذاتی متفاوت است یا خیر، زیرا مدل ریسک حسابرسی (ARM) این رابطه را ارائه کرده است، تجزیه و تحلیل ما بر اعتبار تجربی ARM تکیه دارد. تجزیه و تحلیل ما بر اساس دادههای مالکیت یک نمونه جدید بزرگ از تعدیلات حسابرسی شناسایی شده (n= 1 148) در صورتهای مالی حسابرسی شرکت 4 بزرگ آلمانی بوده است که شامل 255 مشتری بوده است. نمونه شامل دادههایی در مورد تعدیلهای حسابرسی شخصی مانند اندازه و تاثیر بر سود مشتری بوده است و همچنین ویژگیهای مختلفی از مشارکتهای حسابرسی که مرتبط با تعدیلات بوده است که از جمله آنها میتوان به عوامل ریسک کنترل و ریسک ذاتی، اندازه مشتری، ورودی حسابرسی و آستانه اهمیتی که توسط حسابرس برای مشارکت خاص تعیین شده است، اشاره کرد. حسابرسی مطابق با استانداردهای بینالمللی حسابرسی (ISA) توسط شرکت حسابرسی 4 بزرگ انجام شده است. نتایج ما باید قابل تعمیم به حوزههای غیراروپایی، از جمله ایالات متحده امریکا باشد؛ زیرا از شرکت 4 بزرگ انتظار میرود که رویکرد حسابرسی یکنواختی را در سطح جهانی اعمال کند و همچنین زیرا ISA مرتبط با تجزیه و تحلیل ما مشابه با استانداردهای موسسه امریکایی خبرههای حسابداران عمومی (AICPA) است.

آرشیوهای موجود در پیشینه تحقیق مبتنی بر داده عمدتا اکتشافی است یا به طور یکنواخت به تجزیه و تحلیل اثر عوامل ریسک فردی بر تعدیلات حسابرسی پرداختند. تنها سه مطالعه (جانسن 1987 ، وایس و کروتزفلدت1961، 1995 ) بر اساس دادههای جمعآوری شده در دهه 1980 بوده است که نتایج حاصل از یک طراحی تحقیقاتی چندمتغیره را گزارش میدهند. سهم مقاله ما در پیشینه تحقیق این حوزه از دو جهت است. نخست، تحقیق ما مکملی بر تحقیقات پیشین است و تجزیه و تحلیل چندمتغیره پیش از این را با استفاده از دادههای جدیدی که به طور عمومی در دسترس نیستند گسترش میدهد. دوم طراحی تحقیق ما دارای دو تفاوت مهم از تحقیقات قبلی است. ما اهمیت برنامهریزی خاص مشتری را در طرح تحقیق خود گنجاندهایم که این موضوع ما را قادر میسازد تا به محاسبه مقدار نسبی تعدیلات حسابرسی بپردازیم. دو تحقیق پیشینی که تجزیه و تحلیل میزان تعدیلات پرداختهاند (جانسن 1987، وایس و کروتزفلدت1991) از درآمدهای اولیه یا کل داراییها به عنوان جایگزینی برای اهمیت استفاده کردند و از خود اهمیت داشتن استفاده نکردند. علاوه بر این، ما زیرمجموعههای مختلی از تعدیلات حسابرسی را تجزیه و تحلیل کردیم و تعدیلاتی که بر روی سود یا زیان تاثیرگذار هستند را مشخص کردهایم یعنی عواملی که سبب افزایش سود یا زیان میشوند و عواملی که سبب کاهش سود یا ضرر میشوند را به همراه تعداد تعدیلات مشخص کردهایم.

یافتههای ما نشان میدهد که تعداد و میزان تعدیلات حسابرسی به طور سیستماتیک با عوامل ریسک کنترل و ذاتی تفاوت دارد که این موضوع توسط ARM پیشنهاد شده است. به طور خاص، کیفیت (یعنی صداقت و صلاحیت) مدیریت مشتری و موقعیت اقتصادی مشتری (عوامل ریسک ذاتی)، کنترلهای سطح نهاد، عملکرد حسابرسی داخلی و قدرت کلی سیستم کنترل داخلی (عوامل ریسک کنترل) به طور قابل توجهی در ارتباط با مقدار تعدیلات حسابرسی است. نتایج ما سبب آگاهیبخشی به تنظیمکنندههای استاندارد حسابرسی میشود تا آنها پشتیبانی برای تیکه بر ARM و کمک به شرکتهای حسابرسی در طراحی و ساختاردهی به رویکردهای حسابرسی را ارائه دهند.

ادامه مقاله بدین شرح تدوین شده است که در بخش دوم سوالات تحقیقاتی ما و ارتباط بین ARM، اهمیت و تفاوت حسابرسی توضیح داده میشود . پس از یک مرور کلی از پیشینه تحقیق، بخش سوم، طرح تحقیق و نمونه ما را توصیف میکند. در بخش چهارم یافتههای ما و محدودیتهای مطالعه مورد بحث قرار میگیرد. بخش پنجم نتایج ما را خلاصه میکند و پیشنهاداتی برای تحقیقات بیشتر را ارائه میدهد.

سوال و پیشینه تحقیق

در این مقاله به سوال تحقیق زیر پاسخ میدهیم:

سوال تحقیقاتی: آیا تعدیلات حسابرسی از نظر سیستماتیک با عوامل ریسک کنترل و ذاتی متفاوت است؟

این سوال تحقیقاتی دارای مفاهیمی برای اعتبار تجربی قسمتهایی از ARM است.

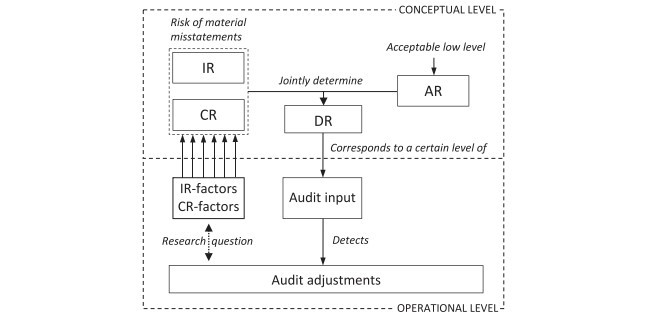

ARM معمولا به شرح زیر تعریف میشود: ریسک حسابرسی (AR)= ریسک تحریفات مواد (RMM) × ریسک شناسایی (DR). RMM ریسک این است که صورتهای مالی قبلی به درستی حسابرسی نشده باشند. RMM را میتوان به ریسک ذاتی × ریسک کنترل تجزیه کرد. ریسک کنترل و ذاتی را میتوان از عوامل مختلفی بدست آورد. ARM رابطه مثبتی بین تحریفات و عوامل مختلف ریسک کنترل و ریسک ذاتی را نشان میدهد. تحریفات و تعدیلات حسابرسی که توسط حسابری برای اصلاح تحریفات ارائه شده است ممکن است همراه با مقداری (اندازهگیری) طبقهبندی و یا افشای یادداشت باشد (کنی2000، 216) .

برای فراهمسازی اطمینانی منطقی برای اینکه گزارشهای مالی به لحاظ اهمیت تحریف نشده باشند، حسابرسها باید هر گونه تحریفات را مستند سازند تا بدین شکل نشان دهند که این انحراف «به وضوح جزئی نیست» یا «نسبتا کوچک» است زیرا یک تحریف بیاهمیت به همراه سایر تحریفات بیاهمیت منجر به یک تحریف مهم در صورتهای مالی خواهند شد . بنابراین، حسابرسها باید کل تحریفات حسابرسی (برای مثال مقدار تجمعی آنها را) نیز در رابطه با اهمیت در نظر بگیرند.

مفهوم اهمیت به شکل ذاتی مرتبط با ARM و تمامی اجزای ARM است (RMM، DR و AR). حسابرسها مفهوم اهمیت را در زمان برنامهریزی و انجام حسابرسی و همچنین در پایان حسابرسی که در آن به ارزیابی اهمیت تعدیلات تصحیح نشده میپردازند، اعمال خواهند کرد . هنگام تعیین اهمیت، حسابرسها باید هم عوامل کمیتی و هم عوامل کیفی را در نظر گیرند.

تنها سه تحقیق پیش از این، رگرسیون چندمتغیره را برای تجزیه و تحلیل رابطه بین عوامل ریسک کنترل و ذاتی و تعدیلات حسابرسی در نظر گرفتهاند. این تجزیه و تحلیلها بر اساس دادههای نسبتا قدیمی هستند. مطالعهای که توسط جانسن در سال 1987 صورت گرفته است از دادههای حسابرسی 55 مشتری در صنعت تولید انگلستان کسب شده است و وی نشان داده است که مسائل شخصی، از جمله شایستگی، با میزان نسبی تعدیلات حسابرسی شخصی مرتبط است (که با تقسیم مقدار مطلق توسط درآمد محاسبه شده است). انگیزههای مدیریتی، مانند مسئال مرتبط با بودجه و پاداش، مرتبط با بزرگی و جهای سود تعدیلات حسابرسی است. عوامل کنترل ریسک به طور کلی مرتبط با تعدیلات نیستند. جانسن در سال 1987 مقادیر R2 تعدیل شده از 34 .0 –18 .0 را کسب کردهاند که این مقدار وابسته به نوع تحریفات بوده است.

SUMMARY

This paper analyzes whether audit adjustments vary systematically with inherent and control risk factors. The analysis is based on proprietary data from a large recent sample of audit adjustments detected in the financial statement audits conducted by a Big 4 audit firm in Germany. We extend the scope of prior studies by incorporating client-specific planning materiality in our design, enabling us to analyze the relative magnitude of adjustments. Our findings show that audit adjustments vary systematically, as proposed by the audit risk model. Specifically, the integrity and competence of the client’s management, economic position, entity-level control strength, and internal control system are associated with the number and relative magnitude of audit adjustments. The results also suggest that inherent and control risk factors are particularly strongly associated with income-affecting adjustments.

INTRODUCTION

This paper analyzes whether audit adjustments1 vary systematically with inherent and control risk factors. Because the audit risk model (ARM) also proposes this relationship, our analysis has a bearing on the empirical validity of the ARM. The analyses are based on proprietary firm data from a large recent sample of audit adjustments (n ¼ 1,148) detected in the 2007 financial statements audits of a German Big 4 audit firm’s sample of 255 clients. The sample includes data on individual audit adjustments such as size and effect on client income, as well as various attributes of the audit engagements to which the adjustments relate, such as inherent and control risk factors, client size, audit input, and the materiality threshold determined by the auditor for a specific engagement. The audits were conducted in accordance with International Standards on Auditing (ISA) by a Big 4 audit firm. Our results should also be generalizable to non-European jurisdictions including the U.S., because a Big 4 audit firm can be expected to apply the audit approach in a uniform manner globally and because the ISA relevant to our analysis are similar to the American Institute of Certified Public Accountants (AICPA) standards.

Prior archival data-based literature is primarily explorative, or univariately analyzes the effect of individual risk factors on audit adjustments. Only three studies (Johnson 1987; Wallace and Kreutzfeldt 1991, 1995), all based on data gathered in the 1980s, report the results from a multivariate research design. Our paper contributes to the existing literature in two respects. First, our research complements and extends earlier multivariate analyses using recent data that are not publicly accessible. Second, our research design differs from that used in earlier studies in two important respects. We incorporate client-specific planning materiality into our research design, which enables us to compute the relative magnitude of the audit adjustments. The two previous studies that analyze the magnitude of adjustments (Johnson 1987; Wallace and Kreutzfeldt 1991) use either revenue or total assets as a proxy for materiality rather than materiality itself. Furthermore, we analyze different subsets of audit adjustments, distinguishing between adjustments that affect profit or loss, increase profit or loss, and those that decrease profit or loss, in addition to the number of adjustments.

Our findings demonstrate that the number and magnitude of audit adjustments vary systematically with inherent and control risk factors as proposed by the ARM. In particular, the quality (i.e., integrity and competence) of a client’s management and economic position (inherent risk factors), entity-level controls, internal audit function, and the overall strength of the internal control system (control risk factors) are significantly associated with the magnitude of audit adjustments. Our results are informative to audit standard setters in providing support for reliance on the ARM and assist audit firms in designing and structuring their audit approaches.

The remainder of the paper is organized as follows. The second section describes our research questions and the relationship among the ARM, materiality, and audit differences. After an overview of the previous literature, the third section describes our sample and research design. The fourth section discusses our findings and the limitations of the study. The fifth section summarizes our results and provides suggestions for further research.

RESEARCH QUESTION AND BACKGROUND

This paper addresses the following research question:

RQ: Do audit adjustments vary systematically with inherent and control risk factors? This research question has implications for the empirical validity of parts of the ARM.

The ARM is commonly defined as follows: audit risk (AR)¼the risk of material misstatements (RMM) 3 detection risk (DR). The RMM is the risk that financial statements are misstated prior to audit. The RMM can be decomposed3 into inherent risk 3 control risk. Inherent and control risk can be driven by various factors. The ARM suggests a positive relationship between misstatements4 and various inherent and control risk factors.5 The misstatement and the audit adjustment that the auditor proposes to correct the misstatement may be associated with an amount (measurement), classification, and/or note disclosure (Kinney 2000, 216).

To provide reasonable assurance that financial statements are not materially misstated, auditors must document every misstatement,7 provided that the deviation is ‘‘not clearly trivial’’ or ‘‘relatively small,’’8 because an immaterial misstatement can, together with other immaterial misstatements,9 result in a material misstatement of financial statements.10 Therefore, the auditor must consider the total audit adjustments (i.e., their aggregated magnitude) in relation to materiality.

The concept of materiality is inherent to the ARM and in all ARM components (RMM, DR, and AR). Auditors apply the concept of materiality when planning and performing an audit as well as at the end of the audit when they evaluate the effect of uncorrected adjustments.11 When determining materiality, auditors must consider both qualitative12 and quantitative13 factors.

Only three prior studies conduct multivariate regression to analyze the relationship between different inherent and control risk factors and audit adjustments. These analyses are based on fairly old data.14 A study by Johnson (1987) using data from the audits of 55 clients in the U.K. manufacturing industry finds that personnel problems, including competence, are associated with the relative magnitude of individual audit adjustments (calculated by dividing the absolute magnitude by revenue). Management incentives, such as bonus and budget issues, are associated with the magnitude and income direction of audit adjustments. Control risk factors are generally not associated with adjustments. Johnson (1987) obtains adjusted R2 values of 0.18–0.34, depending on the type of misstatement.

خلاصه

مقدمه

سوال و پیشینه تحقیق

طراحی نمونه و تحقیق

نمونه

طراحی تحقیق

متغیرهای وابسته

متغیرهای مستقل

تجزیه و تحلیل رگرسیون چند متغیره

یافتهها

آمار توصیفی

تجزیه و تحلیل چند متغیره

عوامل ریسکهای ذاتی و کنترل

متغیرهای کنترلی

تجزیه و تحلیلهای اضافی

جمعبندی

منابع

SUMMARY

INTRODUCTION

RESEARCH QUESTION AND BACKGROUND

SAMPLE AND RESEARCH DESIGN

Sample

Research Design

Dependent Variables

Independent Variables

Multivariate Regression Analysis

FINDINGS

Descriptive Statistics

Multivariate Analysis

Inherent and Control Risk Factors

Control Variables

Additional Analyses

CONCLUSION

REFERENCES