دانلود رایگان مقاله نسبت های مالی بین شرکت های جعلی و غیر جعلی

تقلب مفهوم گسترده ای از دو نوع اساسی دیده شده در عمل است. اولین مورد سوء استفاده از دارایی و دومین مورد گزارشگری مالی متقلبانه است. گزارشگری مالی متقلبانه معمولا به شکل تحریف صورتهای مالی در جهت به دست آوردن برخی از مزایا رخ می دهد. پژوهش حاضر نسبتهای مالی بین شرکت های جعلی و غیر جعلی را برای شرکت های پذیرفته شده در بورس اوراق بهادار تهران مقایسه می کند. نمونه شامل 134 شرکت از 2009 تا 2014 است و برای آزمایش این فرضیه، آزمون t مستقل اعمال شد. نتایج نشان می دهد که اختلاف معنی داری بین متوسط دارایی های جاری به کل دارایی، موجودی به کل دارایی ها و درآمد به نسبت کل دارایی وجود دارد. این بدان معنی است که مدیریت شرکت های تقلبی ممکن است کمتر از مدیریت شرکت های غیر تقلبی در استفاده از دارایی برای تولید درآمد رقابتی باشند. مدیریت ممکن است موجودی را دستکاری کند. این شرکت ممکن نیست فروش را با هزینه های مربوط به کالاهای فروخته شده مطابقت دهد، بنابراین سود ناخالص را افزایش می دهد. علاوه بر این، درآمد خالص و تقویت ترازنامه، دستکاری یا موجودی در قالب پرسشنامه، با هزینه کمتر یا ارزش بازار گزارش شده است و شرکت ها موجودی منسوخ را ضبط نمی کنند. حاشیه بالاتر یا پایین تر به صدور گزارشگری مالی متقابل مربوط است. علاوه بر این، نتایج نشان می دهد که بین استفاده از کل بدهی به مجموع حقوق صاحبان سهام، بدهی کلی به دارایی کلی، سود خالص به درآمد و سرمایه در حال کار به نسبت کل دارایی تفاوت معنی داری وجود ندارد.

مقدمه

تقلب مالی مفهوم حقوقی گسترده ای است، با این حال، طیف گسترده ای از فعالیت ها را پوشش می دهد. موسسه آمریکایی حسابداران رسمی (اعلامیه استانداردهای حسابرسی "شماره 82) و دفتر پاسخگویی ایالات متحده دو نوع تحریف مالی را تعریف کرده اند. مورد اول، به عنوان تقلب مدیریتی شناخته شده است که ناشی از تحریفهای عمدی و یا حذفیات مقادیر و اطلاعات افشا شده در صورتهای مالی است. این موارد توسط مدیریت با قصد فریب صورت گرفته است. مورد دوم ناشی از سوء استفاده از دارایی ها است، به عنوان تقلب کارمند و یا اختلاس شناخته شده است. اکثر تحقیقات بر روی مدل های گزارشگری مالی متقلبانه در نوع اول از تقلب متمرکز هستند (پرسونس ، 1995). گزارشگری مالی متقلبانه یک نوع تقلب با اثرات قابل توجهی منفی، از دست دادن اعتماد سرمایه گذاران، آسیب به شهرت، جریمه بالقوه و اعمال جنایتکارانه است (ارنست و یانگ ، 2009). گزارشگری مالی متقلبانه ممکن است از تلاش برای مخفی کردن اقدامات دیگر تقلب شرکت ها حاصل شوند و یا برای بهبود ظاهر مالی شرکت مقصر باشند (حسنان و همکاران، 2013). گزارشگری مالی متقلبانه به احتمال زیاد در شرکت هایی که دچار مشکلات مالی هستند، در مقایسه با شرکت های طبیعی بیشتر رخ می دهد (بیسلی و همکاران، 1999؛ کینی و مک دانیل، 1989؛ میشرا و دریتنا،2004).

چنین گزارش جعلی یک مشکل بحرانی برای حسابرسان خارجی است، هر دو به دلیل مسئولیت قانونی بالقوه برای عدم شناسایی صورتهای مالی نادرست و به دلیل آسیب به شهرت حرفه ای است که از نارضایتی عمومی در مورد تقلب غیر قابل تشخیص است (کامینسکی و همکاران). سیستم تجزیه تحلیل آماری (SAS)شماره 53 برای کاهش شکاف بین انتظارات مشتریان در مورد مسئولیت حسابرس به منظور کشف تقلب در جریان حسابرسی و آنچه که در واقع مسئولیت است، طراحی شده است (لوی، 52 ، 1989). سیستم تحلیل آماری شماره 82 تقلب در حسابرسی صورت های مالی را بررسی می کند، راهنمایی در مورد مسئولیت حسابرس ارائه می کند طرح و اجرای ممیزی برای کسب اطمینان معقول درباره این مسئله است که آیا صورتهای مالی عاری از تحریف هستند، آیا تحریف ها به وسیله خطا ایجاد می شوند یا تقلب" ( بل و کارسلو،2000).

هاو (1999) پیشنهاد کرد که شرکت ها زمانی به سمت گزارشگری مالی متقلبانه می روند که آنها از تهاجمی ترین اصول عمومی پذیرفته شده حسابداری بهره ببرند.

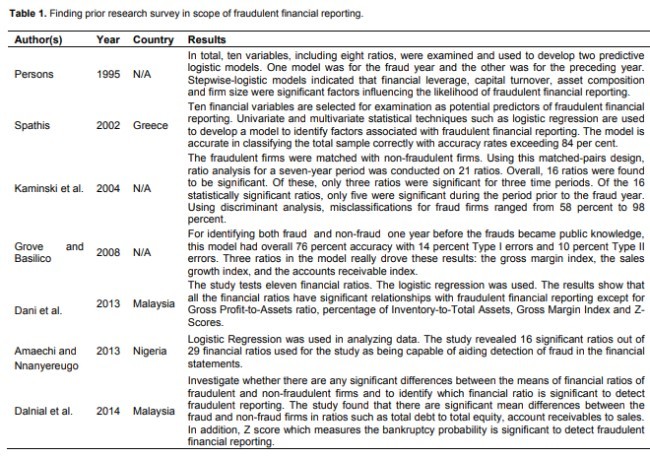

"تجزیه و تحلیل نسبت های ترازهای حساب یک روش نظارتی-هدایتی است که به طور گسترده اعمال می شود، اما هنوز اطلاعات کمی از توانایی تجزیه و تحلیل نسبت به شناسایی خطای پولی مواد در داده های حسابداری واقعی شناخته شده است"(کینی، 60: 1987). چنین تجزیه و تحلیل مالی اغلب فرض می شود که ابزار مفیدی برای شناسایی بی نظمی ها و / یا تقلب هستند (تورنهیل، 1995). به عنوان مثال اهرم مالی، گردش سرمایه، ترکیب دارایی ها و اندازه شرکت با گزارشگری مالی متقلبانه در ارتباط است (اشخاص، 1995).

تشخیص تقلب یکی از وظایف خاص اختصاص داده شده به حسابرسان است که در استانداردهای بین المللی در حسابرسی بیان شده است. حسابرسان معمولا از ابزار شناخته شده به عنوان روش های تحلیلی کمک به آنها در کشف تقلب استفاده می کنند (تورنهیل، 1995؛ آلبرشت و همکاران، 2009). "کمیسیون تریدوی توصیه می کند که امنیت ASB به استفاده از روشهای تحلیلی در ممیزی به منظور بهبود تشخیص گزارشگری مالی متقلبانه نیاز دارد" (ویلر و پنی، 1996: 558). روش تحلیلی نام برده شده برای انواع مختلفی از تکنیک های حسابرسی برای ارزیابی خطر تحریفهای بااهمیت در پرونده های مالی استفاده شده است. این روش شامل تجزیه و تحلیل روند، نسبت، و آزمون های معقول حاصل از داده های مالی و عملیاتی یک واحد تجاری است. سیستم تحلیل آماری شماره 56 مستلزم آن است که روشهای تحلیلی در برنامه ریزی حسابرسی با هدف شناسایی وجود وقایع غیر معمول، مقدار، نسبت و روند اجرا شوند که ممکن است به مسائلی اشاره کند که صورت های مالی و پیامدهای برنامه ریزی حسابرسی را داشته باشند (AICPA ،1988 ). با توجه به سیستم تحلیل آماری شماره 99، استاندارد تقلب جاری، حسابرس باید نتایج حاصل از روشهای تحلیلی را در شناسایی خطرهای تحریف بااهمیت ناشی از تقلب بررسی کند (AICPA،2002). در حالی که این روش ها به خوبی شناخته شده اند و به طور گسترده ای استفاده می شود، عدم درک کلی از چگونگی اعمال درست آنها و مقدار اعتماد جلب شده به آنها وجود دارد. بنابراین، شرکت ها، حسابرسان و تنظیم کننده ها تمرکز خود را بر فهم گزارش های جعلی و نحوه کاهش وقوع آنها افزایش داده اند (لیو و همکاران، 2014).

با توجه به اهمیت موضوع انتشار گزارشگری مالی جعلی، هدف از این مقاله بررسی تفاوت معنی داری بین میانگین نسبت های مالی شرکت ها با تقلب و بدون تقلب است.

باقی مقاله به شرح زیر است: بخش 2 گزارشگری مالی متقلبانه را مورد بحث قرار داده و تحقیق قبلی را برجسته می سازد، بخش 3 هشت فرضیه ایجاد می کند و بخش 4 طرح پژوهش و روش آن را توصیف می کند. بخش 5 نتایج حاصل از پژوهش را توصیف و در نهایت، بخش 6 نتیجه گیری را ارائه می کند.

پیش زمینه تحقیق

تمرکز افزایش یافته در کنترل های داخلی توسط سازمان به عنوان یک مکانیسم برای جلوگیری از رفتار غیر اخلاقی سازگار با تقلب، یک چارچوب گسترده ای را شناسایی می کند تا برای درک عواملی مورد استفاده قرار گیرد که پیش بینی گزارش های جعلی و در نتیجه به عنوان ابزاری برای شناسایی راه هایی برای کاهش تقلب است (AICPA ، 2002؛ کمیته سازمانهای حامی"، 1999). چارچوب سه گانه تقلب، سه عامل گسترده را شناسایی می کنند که احتمال تقلب را افزایش می دهد: مشوق ها، فرصت ها، و عقلانی بودن. تاثیر گزارشگری مالی متقلبانه اغلب فراتر از ضرر و زیان سرمایه گذاران و کلاس های انتخاب شده از طلبکاران است. تجزیه و تحلیل اقتصادی و اخلاقی کافی مستلزم توجه به پیامدهای رفتار غیراخلاقی در سهامداران متعدد است و حتی به عنوان یک کل اثر موج داری بر اقتصاد و جامعه دارد (کالبرس ،2009 ).

Fraud is a broad concept with two basic types seen in practice. The first is the misappropriation of assets and the second is fraudulent financial reporting. Fraudulent financial reporting usually occurs in the form of falsification of financial statements in order to obtain some forms of benefit. The current research compares the financial ratios between fraudulent and non-fraudulent firms for the companies listed on Tehran Stock Exchange. The sample consists of 134 companies from 2009-2014 and for testing the hypothesis Independent sample t-test was exerted. The results show that there is a significant difference between the means of Current Assets to Total Assets, Inventory to Total Assets and Revenue to Total Assets ratios. This means that management of fraud firms may be less competitive than management of non-fraud firms in using assets to generate revenue. Management may manipulate inventories. The company may not match sales with corresponding cost of goods sold, thus increasing gross margin, net income and strengthening the balance sheet. In addition, manipulation of inventory is in form of reporting inventory lower than cost or market value, and companies choosing not to record the obsolete inventory. Higher or lower margins are related to the issuing of fraudulent financial reporting. In addition, the results show that there is not a significant difference between the means of Total Debt to Total Equity, Total Debt to Total Asset, Net Profit to Revenue, Receivables to Revenue and Working Capital to Total Assets ratios.

INTRODUCTION

Financial fraud is a broad legal concept, however, covering a wide range of activities. The American Institute of Certified Public Accountantsi (Statement on Auditing Standardsii No. 82) and the USA Government Accountability Office have defined two types of financial misstatement. The first, known as management fraud, arises from intentional misstatements or omissions of amounts and disclosures in financial statements. These are perpetrated by management with the intent to deceive. The second arises from the misappropriation of assets, and is known as employee fraud or defalcation. The majority of research on fraudulent financial reporting models focuses on the first type of fraud (Persons, 1995). Fraudulent financial reporting is one type of fraud with substantial negative impacts, loss of investor confidence, reputational damage, potential fines and criminal actions (Ernst and Young, 2009). Fraudulent financial reporting may result from an attempt to hide other acts of corporate fraud or be perpetrated to improve the company’s financial appearance (Hasnan et al., 2013). Fraudulent financial reporting is more likely to occur in companies experiencing financial difficulties than in normal companies (Beasley et al., 1999; Kinney and McDaniel, 1989; Mishra and Drtina, 2004).

Such fraudulent reporting is a critical problem for external auditors, both because of the potential legal liability for failure to detect false financial statements and because of the damage to professional reputation that results from public dissatisfaction about undetected fraud (Kaminski et al). SAS No. 53 was designed to narrow the gap between clients’ expectations regarding the auditor’s responsibility to detect fraud during an audit and what that responsibility actually is (Levy, 1989: 52). SAS No. 82, Consideration of Fraud in a Financial Statement Audit, provides guidance on the auditor’s responsibility to “plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether caused by error or fraud” (Bell and Carcello, 2000).

Howe (1999) suggested that firms turn to fraudulent financial reporting when they have already taken advantage of the most aggressive Generally Accepted Accounting Principlesiii .

“Analysis of ratios of account balances is a widely applied attention-direction procedure, yet little is known of the ability of ratio analysis to identify material monetary error in actual accounting data” (Kinney, 1987: 60). Such financial analysis is frequently posited to be a useful tool for identifying irregularities and/or fraud (Thornhill, 1995). For example financial leverage, capital turnover, asset composition and firm size are associated with fraudulent financial reporting (Persons, 1995).

Fraud detection is one of the specific tasks assigned to auditors as stated in International Standards on Auditingiv 240. Auditors commonly use tools known as analytical procedures to assist them in detecting fraud (Thornhill, 1995; Albrecht et al., 2009). “The Treadway Commission recommended that the ASB Security requires the use of analytical procedures on all audits to improve the detection of fraudulent financial reporting” (Wheeler and Pany, 1996: 558). Analytical procedure is the name used for a variety of techniques the auditor can use to assess the risk of material misstatements in financial records. These procedures involve the analysis of trends, ratios, and reasonableness tests derived from an entity’s financial and operating data. SAS No. 56 requires that Analytical procedures be performed in planning the audit with an objective of identifying the existence of unusual events, amounts, ratios and trends that might indicate matters that have financial statement and audit planning implications (AICPA, 1988). According to SAS No. 99, the current fraud standard, the auditor should consider the results of Analytical procedures in identifying the risks of material misstatement due to fraud (AICPA, 2002). While the procedures are well known and widely used, there is a general lack of understanding of how they are properly applied, and how much reliance should be placed on them. So, companies, auditors, and regulators have increased their focus on understanding fraudulent reporting and how to mitigate its occurrence (Liu et al., 2014).

Due to the importance of fraudulent financial reporting issue the objective of this paper is to investigate the significant differences between the mean of financial ratios of fraud and non- fraud companies.

The remainder of the paper is organized as follows: Section 2 discusses the fraudulent financial reporting and highlights the prior research, Section 3 develops eight hypotheses, and Section 4 describes the research design and methodology. Section 5 describes the results of research and finally, Section 6 provides conclusions.

LITERATURE REVIEW

The increased focus on internal controls by organizations as a mechanism to prevent unethical behavior is consistent with the Fraud Triangle, a widely recognized framework used to understand factors that are predictive of fraudulent reporting and thereby as a means to identify ways to mitigate fraud (AICPA, 2002; The Committee of Sponsoring Organizationsv , 1999). The framework of Fraud Triangle identifies three broad factors that increase the likelihood for fraud: incentives, opportunities, and rationalization. The impact of fraudulent financial reporting often goes far beyond losses for investors and selected classes of creditors. An adequate economic and ethical analysis requires consideration of the outcomes of unethical behavior on multiple stakeholders, and even the ripple effect on the economy and society as a whole (Kalbers, 2009).

مقدمه

پیش زمینه تحقیق

ساخت فرضیات

جمعیت آماری و نمونه برداری

روش تحقیق

اندازه گیری گزارشگری مالی متقلبانه

زی-اسکور آلتمن

تعریف "مدل بنیش"

روش آزمون

اندازه گیری متغیرها

احتمال گزارشگری مالی متقلبانه

نسبت های مالی

اهرم مالی

سودآوری

ترکیب دارایی

نقدینگی

گردش مالی سرمایه

نتایج تجربی

منابع

INTRODUCTION

LITERATURE REVIEW

Hypotheses development

Population and sampling

METHODOLOGY

Measuring fraudulent financial reporting

ALTMAN Z-score

Definition of “BENEISH MODEL”

Test method

Measurement of variables

Likelihood of fraudulent financial reporting

Financial ratio

Financial leverage

Profitability

Asset composition

Liquidity

Capital turnover

EMPIRICAL RESULTS

Conclusion

REFERENCES