دانلود رایگان مقاله هدفگذاری تورمی و توازن نرخ بهره واقعی

چکیده

چکیده

این مقاله به بررسی این که آیا هدفگذاری تورمی از طریق یک رویکرد اصلاح جهت گیری تحت وابستگی مقطعی بر توازن نرخ بهره ی واقعی تاثیر (RIP) می گذارد، می پردازد. روش تنظیم متوسط بازگشتی (RMA) که توسط و سو و شین (1999) و شین و سو (2001) پیشنهاد شده است برای اصلاح جهت گیری رو به پایین در آزمون های ریشه واحد پانل و در برآوردهای نیمه عمر تفاوت های نرخ بهره ی واقعی برای کالاهای معامله شده و غیر معامله شده استفاده شده است. یافته های تجربی بسته به اینکه آیا مااز روش RMA استفاده کنیم یا خیر متفاوت است. از همه مهمتر اینکه، نتایج تجربی نشان می دهد که زمانی که اقتصادهای همگن بیشتری در شرایط رژیم هدفگذاری تورمی درگیر می شوند، متوسط بازگشت قوی تر و فاصله ی اطمینان بسیارکم تر می شود. بنابراین، هدف قرار دادن تورم نقش مهمی در ارائه یشواهد و مدارک مناسب برای RIP در بلندمدت بازی می کند.

مقدمه

مقاله ی حاضر به بررسی این که آیا تأثیرات هدفگذاری تورمی از طریق رویکرد اصلاح جهت گیری تحت وابستگی مقطعی توازن نرخ بهره ی واقعی (RIP) را تحت تاثیر قرار می دهد یا خیر پرداخته است. RIP از توازن بهره ی پوشش داده نشده(UIP) و توازن قدرت خرید (PPP)تشکیل شده است که با هم متضمن توازن نرخ های واقعی سود در بازارهای ارز خارجی است. در واقع، فرض توازن نرخ بهره واقعی در تمام کشورهایی که درجه بالایی از تحرک سرمایه بعلاوه ی سطح بالایی از نفوذ فن آوری دارند وجود دارد که به عنوان یک فرض مهم در روش پولی اولیه برای تعیین نرخ ارز عمل می کند. RIP همچنین به منظور بررسی مجموعه ای از پرسش های کلیدی در اقتصادهای کلان اقتصاد باز در مورد کارآمدی تخصیص سرمایه، نوسانات مصرف و رشد اقتصادی استفاده شده است. اگر چه اهمیت نظری RIP و همچنین اعتبار آن برای مسائل تجزیه و تحلیل مربوط به سیاست های پولی و مالی مهم هستند، حمایت وتایید تجربی RIP در پیشینه ی تحقیقات دشوار است.

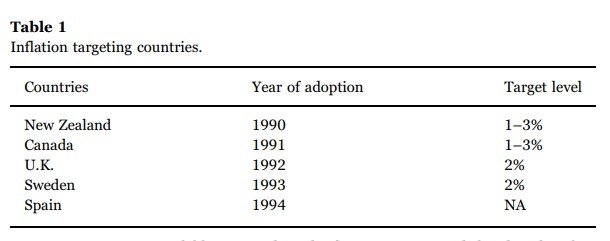

تعدادی از مطالعات کشورهای OECD ازRIP بلندمدت در داده های پانل حمایت کرده اند. یک توضیح مشترک برای این یافته این است که افزایش مقدار اطلاعات درمورد نرخ های بهره ی واقعی معمولا قدرت آزمون های ریشه واحد را افزایش می دهد و بر موضوع قدرت کم مطالعات اولیه ی ریشه واحد تک متغیره غلبه می کند. از سوی دیگر، رز (2014) نشان می دهد که وجود بازار اوراق قرضه تحت هدف گذاری تورم با تورم پایدار ارتباط دارد زیرا این سیاست از تورم پایین به طور موثر حفاظت می کند. همانطور که توسط سونسون(2000) ، میشکین و اشمیت-هبل (2007)، و کیم (2014) نشان داده شده است درجه ی بالای شفافیت و پاسحگویی سیاست پولی نه تنها اختلاف در نرخ تورم بلکه در نرخ ارز واقعی در یک افق بلند را محدود می کند، در نتیجه نرخ های ارز واقعی به یک مقدار معنی دار نسبت به موارد دیگر حکومت های پولی ثبات پیدا می کنند. از زمانی که در زلاندنو هدفگذاری تورمی در سال 1990به تصویب رسید.

کشورهای مختلف صنعتی و در حال ظهور به صراحت با از یک هدف تورمی به عنوان لنگر اسمی خود استفاده کرده اند. همانطور که توسط سونسون (2000) و میشکین و اشمیت-هبل (2007) نشان داده شده است آنچه ساخته شده این رژیم سیاست های پولی را ویژه و خاص کرده است تعهد دولتی صریح و روشن به ثبات تورم به عنوان هدف اصلی سیاست و تاکید بر شفافیت سیاست پولی و پاسخگویی بود. از ویژگیهای این رژیم سیاست پولی جدید: (1) اهداف تورمی کمّی صریح ،(2)یک رویکرد سیاست مبتنی بر یک ارزیابی از آینده ی پیش رو ، یعنی استفاده از پیش بینی تورم مشروط داخلی به عنوان واسطه ی هدف قرار دادن متغیرها، و (3) درجه بالایی از شفافیت و پاسخگویی.

سونسون (2000) یک چارچوب نظری برای اقتصاد باز کوچک با کانال های نرخ ارز برای انتقال سیاست پولی به تورم ارائه می کند و شواهدی نشان می دهد مبنی بر این که هدفگذاری تورمی اختلاف در قیمت های نسبی را کاهش می دهد ،واریانس های بلند مدت بی قید و شرط نرخ های ارز واقعی در موارد هدفگذاری تورمی انعطاف پذیرکوچکتر از واریانس های دیگر موارد هستند. علاوه بر این، شواهد تجربی از جمله میشکین و اشمیت-هبل (2007) در مورد ارتباط بین هدفگذاری تورمی و اقدامات خاص عملکرد اقتصادی نیز نشان می دهد که هدف قرار دادن نرخ تورم با بهبود عملکرد اقتصاد کل در آن سطوح تورم مرتبط است ، نوسانات تورم و نرخ های بهره پس از آن که کشورها هدف گذاری تورم را به تصویب رساندند کاهش یافته است. فرضیه ی مهم در مطالعه ی حاضر این است که اگر نظریه و شواهد درست باشند و در همان زمان اگر PPPبهتر نگه داشته شده بود و بازار اوراق قرضه با تورم کم در کشورهای تحت هدف گذاری تورم در ارتباط بود ، هدفگذاری تورمی نقش مهمی در ارائه ی شواهد و مدارک مناسب برای RIP بازی می کند.

یک مسئله اساسا و تجربی مهم تا مطالعه ی حاضر میزانی است که می توان حرکات کالاها و بازارهای سرمایه را در سراسر کشورها از طریق سطح یکپارچگی اقتصادی اندازه گیری کرد. پاسخ به این سوال به درجه ی یکپارچگی اقتصادی بین بازارهای سراسر اقتصادها بستگی دارد. بدلیل تداوم بالای نرخ بهره و همچنین قیمت کالاها، حداقل مجذور (LS)برآوردهای توازن ممکن است به نظر رسد از یک جهت گیری رو به پایین در ضریب همبستگی مداوم رنج می برند ، که این متضمن این نکته است که شرایط توازن از آنچه که حقیقتا هست با ثبات کمتری برآورد شده است. به منظور اصلاح این جهت گیری، اندروز (1993)، اندروز و چن (1994) و هانسن (1999) روش هایی مانند برآوردگر متوسط-جهت گیری نشده و روش های بوت استرپ شبکه پیشنهاد کرده اند. با این حال، در حالی که این جهت گیری بالقوه در پیشینه ی تحقیقات از زمان یافته های بدوی کندال (1954) به رسمیت شناخته شده است هیچ مطالعه ی تجربی تا کنون برآورد تصحیح جهت گیری را به منظور بررسی تاثیر هدفگذاری تورمی بر RIP را انجام نداده است.

نکته ی مهم دیگر برای درک شرایط توازن وابستگی مقطعی است. آزمون های ریشه واحد پنل به طور گسترده ای به منظور بررسی PPP و RIP به کار گرفته شده اند، با این حال، نتایج چنین آزمایشاتی با وابستگی مقطعی کمتر PPP و یا RIPرا در مقایسه با آزمون های بدون وابستگی مقطعی تایید می کنند. علاوه بر این، فیلیپس و سول (2003) نشان می دهند که اگر وابستگی مقطعی جدی در داده ها وجود داشته باشد و این در برآورد نادیده گرفته شده است، بهره وری برآورد می تواند کاهش یابد درنتیجه برآوردگر پانل LS ممکن است سود بهره وری کمی طی معادله ی تک LS ارائه کند. بنابراین، بررسی اینکه آیا هدف قرار دادن تورم برای RIP علاوه بر عوامل دیگر مانند شاخص های قیمت و وابستگی مقطعی جهت گیری اصلاح شده در داده های پانل نقش مهمی دارد یا خیر جالب است.

برای آزمودن نفوذ هدفگذاری تورمی در این زمینه و به منظور برآورد نیمه عمر، ما از تنظیم میانگین بازگشتی (RMA) که توسط سو و شین (1999)پیشنهاد شده است استفاده کرده ایم. طبق روش سو و شین، برآوردگر RMA از لحاظ محاسباتی مناسب و قدرتمند است و در بسیاری از مطالعاتبه کار گرفته شده است. به عنوان مثال، تیلور (2002)در میان بسیاری دیگر RMAمبتنی بر آزمون ریشه واحد فصلی را به کار گرفته است و سول و همکارانش (2005) از RMA برای برآورد ناهمسانی و همبستگی پایدار استفاده کرده اند. علاوه بر این، چوی و همکارانش (2010) یک RMA مبتنی بر روش اصلاح جهت گیری برای داده های پانل پویا طراحی کرده اند و چوادیک و پیسران (2015) از RMA به منظور روش اثرات همبستگی مشترک برای مدل های داده های پانل ناهمگن با متغیر وابسته عقب افتاده استفاده کرده اند. آنها درمی یابند که برآورد کننده های پیشنهادشده عملکرد رضایت بخشی برای اصلاح جهت گیری دارند

ABSTRACT

This paper investigates whether inflation-targeting influences real interest rate parity (RIP) by a bias correction approach under cross-sectional dependence. The recursive mean adjustment (RMA) method proposed by So and Shin (1999) and Shin and So (2001) is employed to correct the downward bias in the panel unit root tests and in the half-life estimates of real interest rate differentials for traded and non-traded goods. The empirical findings differ depending on whether we apply the RMA. More importantly, the empirical results show that as more homogeneous economies become involved in terms of inflation-targeting regime, stronger mean reversion and much a tighter confidence interval are present. Thus, inflation-targeting plays an important role in providing favorable evidence for long-run RIP.

Introduction

The present paper examines whether inflation-targeting influences real interest rate parity (RIP) by a bias correction approach under cross-sectional dependence. RIP comprises uncovered interest parity (UIP) and purchasing power parity (PPP), which together imply the equalization of real rates of return in foreign exchange markets. Indeed, the assumption of the equality of real interest rates across countries characterized by a high degree of capital mobility together with high levels of technology diffusion served as an important premise in early monetary approaches to exchange rate determination.1 RIP has also been used to investigate an array of key questions in openeconomy macroeconomics regarding the efficiency of capital allocation, the volatility of consumptions, and economic growth. Although the theoretical importance of RIP as well as its validity for analyzing issues related to fiscal and monetary policy are important, empirical support for RIP in the literature is elusive.

A number of studies of OECD countries provide support for longrun RIP based on panel data.2 One common explanation for this finding is that increasing the amount of information on real interest rates typically increases the power of unit root tests and overcome the issue of the low power of early univariate unit root studies.3 On the other hand, Rose (2014) shows that the existence of bond market under inflation-targeting is associated with stable inflation because it creates an effective safeguard for low inflation.4 As shown by Svensson (2000), Mishkin and Schmidt-Hebbel (2007), and Kim (2014), the high degree of transparency and accountability of monetary policy limits not only variability in inflation but also that in the real exchange rate at a long horizon, thereby stabilizing real exchange rates to a significant amount relative to the cases under other monetary regimes.

Various industrial and emerging countries have explicitly used an inflation target as their nominal anchor since New Zealand adopted inflation-targeting in 1990.5 As shown by Svensson (2000) and Mishkin and Schmidt-Hebbel (2007), what made this monetary policy regime special was the explicit public commitment to stabilizing inflation as the main policy target and the emphasis on monetary policy transparency and accountability. This new monetary policy regime is characterized by (1) explicit quantitative inflation targets, (2) a policy approach based on a forward-looking assessment, namely use of an internal conditional inflation forecast as an intermediate target variables, and (3) a high degree of transparency and accountability.

Svensson (2000) provides a theoretical framework for a small open economy with exchange rate channels for the transmission of monetary policy to inflation and shows evidence that since inflation-targeting reduces variability in relative prices, the long-run unconditional variances of real exchange rates in flexible inflation-targeting cases are smaller than those in other cases.7 Further, empirical evidence including Mishkin and Schmidt-Hebbel (2007) on the link between inflation-targeting and particular measures of economic performance also shows that inflation-targeting is associated with an improvement on overall economic performance in that inflation levels, inflation volatility, and interest rates have declined after countries adopted inflation targeting. The important hypothesis in the present study is that if the theory and evidence were right and at the same time if PPP were to hold better and the bond market were correlated with low inflation in countries under inflation-targeting, inflation-targeting would play an important role to provide favorable evidence for RIP.

One fundamentally and empirically important issue to the present study is the degree to which the movements of goods and capital markets across countries can be measured by the level of economic integration. The answer to this question depends on the degree of economic integration between markets across economies. Because of the high persistence of interest rates as well as of goods' prices, least squares (LS) estimates of parity might appear to suffer from a downward bias in the persistent coefficient, implying that the parity condition is estimated spuriously to be less persistent than it actually is. In order to correct this bias, Andrews (1993), Andrews and Chen (1994) and Hansen (1999) have proposed approaches such as the median-unbiased estimator and grid bootstrap methods, respectively. However, while this potential bias has been recognized in the time series literature ever since the seminal findings of Kendall (1954), no empirical study has thus far carried out an estimation of bias-correction in order to examine the influence of inflation-targeting on RIP.

The other important point in question for understanding the parity condition is cross-sectional dependence. Panel unit root tests have been widely employed to investigate PPP and RIP, however, the results of such tests with cross-sectional dependence lend little support to PPP or RIP in contrast to tests without cross-sectional dependence.8 Furthermore, Phillips and Sul (2003) show that if there exists serious cross-sectional dependence in the data and it is ignored in estimation, estimation efficiency can decrease so that the panel LS estimator may provide little efficiency gain over the single equation LS. Thus, it is interesting to examine whether inflation-targeting has a significant role for RIP in addition to other factors such as price indices and biascorrected cross-sectional dependence in the panel data.

To test the influence of inflation-targeting in this regard and to estimate the half-life,9 we use recursive mean adjustment (RMA) proposed by So and Shin (1999). According to So and Shin, the RMA estimator is computationally convenient and powerful, and has been employed in many studies. For instance, among many others, Taylor (2002) employs the RMA based seasonal unit root test and Sul et al. (2005) use RMA for heteroscedasticity and autocorrelation consistent estimation.10 Further, Choi et al. (2010) develop a RMA based bias correction method for dynamic panel data and Chudik and Pesaran (2015) apply RMA to common correlated effects approach for heterogeneous panel data models with lagged dependent variable. They find that the proposed estimators have satisfactory performance to correct the bias.

چکیده

1. مقدمه

2. مدل اقتصاد سنجی و برآورد

3. نتایج تجربی

4. نتیجه گیری

- Abstract

- Introduction

- Econometric model and estimation

- Empirical results

- Conclusion