دانلود رایگان مقاله دوسو توانی سازمانی، مدیریت عملکرد و دانش

هدف: انواع مختلفی از دوسو توانی سازمانی پیشنهاد شده در نوشته های مربوطه در این مقاله از نظر کمیتی مورد تجزیه و تحلیل قرار گرفت. استراتژی های در نظر گرفته شده دوسو توانی با انواع مختلفی از مدیریت دانش توجیه شد که به خاطر پیاده سازی موفق آنها, می توان در هر موردی آنها را اعمال نمود. مدیریت دانش, یک سیستم نهادی محسوب می شود که تقریباً در همه شرکت ها وجود دارد اما به شیوه ای متفاوت از آن استفاده می شود. با این حال، مدیریت دانش مؤثر, محرک اصلی توسعه پایدار شرکت است، این یکی از عناصر اساسی برای استفاده موثر از دانش و شایستگی شرکت ها و نیز برای توسعه استراتژی و هوش رقابتی است.

طراحی / روش شناسی / رویکرد: تجزیه و تحلیل تجربی استراتژی های مختلف دوسو توانی برای بخش های انرژی و داروسازی در این مقاله ارائه شده است. روش تحلیل پوششی داده ها (DEA) برای برآورد دوسو توانی سازمانی با استفاده از معیارهای عملکرد نوآوری به کار برده شد. امتیاز DEA مبتنی بر ورودی شدت کارآفرینی و عملکرد کوتاه مدت و بلند مدت به عنوان نماینده ای برای دوسو توانی سازمانی عمل نمود. دوسوتوانی محصول و پایداری نیز به عنوان اصلی ترین عوامل دوسو توانی سازمانی در نظر گرفته شدند.

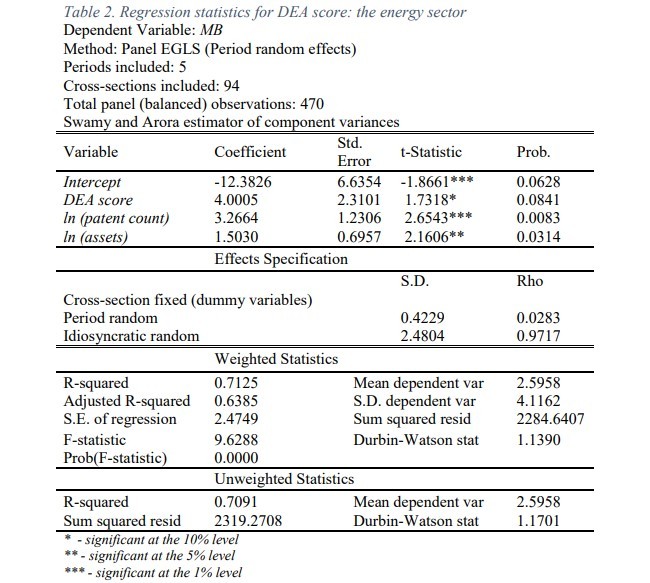

نتایج: برآوردها قویاً دوسو توانی سازماني را با كارايي شركت در هر دو بخش كه در اينجا مورد بررسي قرار گرفته است، مرتبط نشان می دهند. رابطه مثبت بین عملکرد و دوسو توانی سازمانی برای بخش انرژی کشف شد. در عین حال گرایش به سوی پایداری عملکرد شرکتهای دارویی را مختل می کند. تجزیه و تحلیل ارائه شده در این مقاله، نشانه ای برای ارتباطمدیریت دانش و دوسوتوانی سازمانی ارائه می دهد.

اصالت / ارزش: رویکرد جدید برای اندازه گیری دوسو توانی سازمانی با استفاده از DEA در این مقاله پیشنهاد شده است. استراتژی های مختلفی از جمله دوسو توانی و پایداری محصول تخمین زده می شود و عملکرد آنها با هم مقایسه می شود. شیوه های مدیریت دانش برای توجیه انتخاب استراتژی های دوسو توانی استفاده می شوند.

1. مقدمه

رویکردهای ایجاد ارزش سنتی, دیگر تمام چالشهای نوظهور برای شرکتهای مدرن را کاملاً برطرف نمی کنند. در طی دو دهه گذشته, شدت کارآفرینی (EI) به عنوان یک مسئله کلیدی مدیریت استراتژیک به همراه انواع فعالیت های نوآوری (Morris and Sexton، 1996) پدید آمده است. EI به تصمیمات استراتژیک مختلفی از جمله نوآوری محصول، نوآوری فرایند، گسترش به بازارهای جدید و نوآوری مدل تجاری اشاره دارد.

با این وجود, تهیه تصمیمات مربوطه مستلزم جمع آوری و تجزیه و تحلیل داده های به خوبی ساختاریافته و نظام مند است. این کار به نوبه خود بخشی از ویژگیهای اصلی مدیریت دانش شرکت را تشکیل می دهد. مدیریت دانش (KM) نباید با فناوری اطلاعات اشتباه گرفته شود: IT یک عامل توانمند مهم است، به عنوان مثال در ارائه راه حل های مدیریت اسناد، اما مدیریت دانش, موضوعی بسیار گسترده تر است. این مقوله یک رویکرد فعال در شناسایی، استفاده و ارتقای توانمندی ها و تجربیات ضمنی, صریح و مجسم شده یک سازمان نشان می دهد. یک تلاش منظم و سازمان یافته برای استفاده از دانش درون یک سازمان برای تحقق اهداف سازمانی و ارتقای ارزش آن برای ذینفعان (KM سازمانی) است (Becerra-Fernandez 2001). این مقوله می تواند با تغییر قابلیت آن در ذخیره سازی و استفاده از اطلاعات و توسعه دارایی های سازمان، محصولات و فرآیندهای جدید (KM فن آورانه) ارتقا یابد (Hit et al 2000؛ Gold and Arvind Malhotra 2001؛ Bonifacio et al 2000). علاوه بر نوشته های KM سازمانی و فناورانه، اغلب از KM محیطی نقل قول می شود که بیشتر, منابع طبیعی و تحولات زیست محیطی در طی زمان را برای یک هدف کاملاً متفاوت از KM سازمانی و فناوری هدف می گیرد (Berkes et al 2000؛ Moller et al 2004؛ Usher 2000). دامنه کار KM زیست محیطی در نظارت بر منابع زیست محیطی و طبیعی و توسعه, به جای نتایج اقتصادی با دوام است که مدنظر مدیریت فنی و سازمانی می باشد.

به طور کلی، KM مستلزم اینست که کل سازمان برای حمایت از تولید و به اشتراک گذاری دانش همراستا شوند (Kakabadse و همکاران 2003). از توضیحات وظایف پایه اصلی KM اینطور بر می آید که KM, نقش حمایتی را برای فعالیت های نوآوری شرکت در توسعه استراتژیک بلند مدت شرکت ایفا می کند. با این حال, نوآوری یک رویداد یک زمانه نیست بلکه نیاز به تلاش مستمر برای ایجاد و حفظ مجرای پروژه نوآوری بی عیب دارد که پتانسیل بهره برداری و تولید ارزش اقتصادی را دارد. هنوز هم نوآوری اغلب به افراد و دانش ضمنی مرتبط و گره خورده است که KM را به یک دارایی مهم برای شرکت هایی تبدیل ساخته است که علاقه ذاتی دارند که افراد منفرد و کمتر وابسته و دانش آنها را به منظور حفاظت از جریان نوآوری سازگار به کار گیرند. در این راستا، KM به عنوان رویکردی در نظر گرفته شده است که با رمزگذاری و ذخیره اطلاعات و دانش تا حد ممکن، از فعالیت های نوآوری حمایت می کند و برای افراد دخیل در فعالیت های نوآوری, ابزار پشتیبانی به منظور استفاده در عملیات های روزانه را فراهم می کند.

علاوه بر این، KM و ارتباط آن با نوآوری نیز می تواند در پرتوی دوسو توانی سازمانی (OA) مشاهده شود که توانایی سازمان برای پیگیری چندین هدف رقابتی در یک زمان است (Adler و همکاران، 1999 ؛ Porter، 1996). به عنوان مثال، شرکت می تواند همزمان در نوآوری فرایند و محصول درگیر شود و منابع را بین آنها توزیع کند. این بدان معناست که می توان فرآیندهای تجاری را کارآمدتر کرد و در عین حال می توان مشتریان بیشتری نیز پیدا کرد و جایگاه های جدید بازار با محصولات جدید را کاوش کرد. در این حالت, KM می تواند به عنوان یک عنصر ضروری از استراتژی هایی به کار گرفته شود که استفاده از اطلاعات مربوط به محصولات اصلی به منظور توسعه و توزیع محصولات جدید را میسر می سازند.

چارچوب دوسوتوانی سازمانی توسط March (1991) معرفی شد. March, فعالیت های بهره برداری و اکتشاف شرکت ها و رقابت بین آنها را در نظر می گرفت. فعالیت های بهره برداری به صورت افزایشی تدریجی و نسبتاً به سرعت فناوری ها و فرآیندهای تجاری موجود را با هدف بالا بردن راندمان و کاهش ریسک بهبود می بخشد. در مقابل، March اظهار داشت كه اكتشاف به فرصتهای جدید در آینده دور اشاره می كند، که عدم قطعیت و فضا برای انعطاف پذیری مدیریتی را افزایش می دهد. اکتشاف نزدیک به رویکرد گزینه-واقعی در شیوه مدیریت استراتژیک است (به عنوان مثال، Dortland و همکاران، 2014). نوآوری و ریسک پذیری به موفقیت فعالیت های نوآوری قبلی بستگی دارد. تعادل یا موازنه مطلوب بین بهره برداری و اکتشاف، دوسوتوانی سازمان را تعیین می کند.

با توسعه ایده های March, Gupta و همکارانش (2006) استدلال كردند كه اكتشاف و بهره برداري به طور متقابل عملكرد سازماني را ارتقا می دهند. بسیاری از محققان (Gibson و Birkinshaw ، 2004 ؛ He و Wong, 2004; Lubatkin et al., 2006; Raisch et al., 2009; Simsek ، 2009) با آنها موافق هستند و به طور تجربی نشان می دهند که دوسو توانی سازمانی برای بهره وری یک شرکت سودمند است. با این حال، برخی از مطالعات (Atuahene-Gima، 2005) یک اثر منفی را مستندسازی کردند. پیرو رویکرد March و نوشته های فوق، در این مقاله, ما تأثیر OA را مطالعه می کنیم و اثرات کوتاه مدت و بلند مدت برای شرکت ها را متمایز می کنیم.

رویکردهای زیادی برای سنجش تأثیر بر کارآیی وجود دارد. با استفاده از معیارهای عملکرد سازمانی می توان آن را تخمین زد (Murphy و همكاران، 1996). با نگاه به معیارهای عملکرد حسابداری مانند حاشیه های سود، بازگشت دارایی ها، بازده سرمایه گذاری و غیره, می توان اثرات کوتاه مدت را کشف کرد. عملکرد محصول را می توان از طریق رشد فروش و سهم بازار آشکار کرد. معیارهای پیچیده تر نگاه کننده به عقب، از جمله بازده کل سهامداران، ارزش افزوده اقتصادی و غیره, مبتنی بر ارزش هستند و ریسک های سهامداران را در نظر می گیرند. معیارهای بازار مالی نظیر پیگیری EPS و سرمایه گذاری بازار, آینده نگرانه هستند، اما عمدتاً اثرات کوتاه مدت را طبق انتظارات سرمایه گذاران مشخص می کنند. Richard و همکاران (2009), معیارهای ترکیبی را متمایز می کنند: جریان نقدی تقسیم بر تعداد سهام (CF در هر سهم)، ارزش بازار-به-دفتر و Q Tobin. Maditinos و همکاران. (2011) ویژگیهای قابل قبول ارزش بازار-به-دفتر را در مقایسه با معیارهای حسابداری مالی و بازار برجسته می کنند زیرا نه تنها آینده نگرانه است بلکه می تواند یک نماینده برای فرصت های رشد آینده باشد.

تأثیر بر عملکرد سازمانی را نیز می توان از منظر فعالیتهای نوآورانه و EI در نظر گرفت. بنابراین چنین تأثیری, عملکرد نوآورانه نامیده می شود که یک معیار از بهره وری EI است. Griliches (1981) اظهار داشت که نوآوری محصول و فرایند تأثیر مثبتی بر عملکرد عملیاتی بلندمدت دارد و باید ارزش بازار را افزایش دهد. شواهد تجربی, تأثیر مثبت نوآوری های اندازه گیری شده از طریق شاخص های ثبت اختراع بر ارزش و عملکرد بلند مدت را نشان داده اند (Bessler و Bittelmeyer ، 2008). مخارج R&D (Coombs و Bierly III، 2006)، شمار ثبت اختراع، مقالات ثبت اختراع (نارین و همکاران، 1987)، اعلامیه های محصول جدید (Iversen و همکاران، 2007), نماینده های مفیدی برای نوآوری کردن هستند. Coombs وIII Bierly (2006) بر رابطه بین هزینه های R&D و ثبت اختراع تأکید می کنند، زیرا ثبت اختراعات در مراحل اولیه پروژه های R&D حاصل می شوند. Narin و همکاران. (1987، صفحه 144) اظهار داشتند كه تعداد ثبت اختراعات نسبت به میزان واقعي نوآوري,"شاخص بهتری برای تعهد شركت در پیگیری نوآوري است". Hagedoorn و Cloodt (2003) استدلال نمودند كه رویكرد تک-شاخص برای صنایع فناوری-پیشرفته مناسب تر است، اگرچه برای نشان دادن چندبعدی بودن عملکرد نوآورانه, شرکت های دارویی نیاز به یك شاخص ترکیبی دارند.

اثربخشی سازمانی می تواند فراتر از عملکرد سازمانی و نوآورانه, شامل اقدامات خارجی شود که با ارزش گذاری اقتصادی برای ذینفعان سنتی: سهامداران، مدیران یا مشتریان, مرتبط هستند (Richard و همکاران، 2009). این معیارهای خارجی می توانند مسئولیت اجتماعی شرکت باشد. بازده بلند مدت نیز می تواند به توسعه پایدار مرتبط باشد. این ایده در نوشته های مربوط منعکس شده است. به عنوان مثال، Chen و همکاران. (2014) مصاحبه هایی را با مدیران انجام دادند و تأثیر مثبت اهداف پایداری بر عملکرد سازمانی و ابتکاری را نشان دادند. Du et al. (2013) نیز بر تمرکز جدید سازمانها بر توسعه پایدار تأکید کردند.

Purpose: Several types of organizational ambidexterity proposed in the relevant literature were quantitatively analyzed in the paper. Considered ambidexterity strategies was justified by different types of knowledge management that may be applied in each case for their successful implementation. Knowledge Management is considered an institutional system which is in place in almost all companies but used differently. Yet effective knowledge management is a major driver of sustainable company development, it’s among the essential ingredients for effective use of companies knowledge and competencies as well as for strategy development and competitive intelligence.

Design/methodology/approach: Empirical analysis of different ambidexterity strategies for the energy and pharmaceuticals sectors was provided. Data envelopment analysis (DEA) method was applied to estimate organizational ambidexterity using innovation performance measures. The DEA score based on entrepreneurial intensity input and short term and long term performance acted as a proxy for organizational ambidexterity. Sustainability and product ambidexterity were also considered as the key factors of organizational ambidexterity.

Results: Estimations strongly associate organizational ambidexterity with efficiency of the company in both sectors examined here. Positive relation between performance and organizational ambidexterity for energy sector were discovered. At the same time orientation towards sustainability disrupts performance of pharmaceutical companies. The analysis provided in the paper provides indication for coupling knowledge management and organizational ambidexterity.

Originality/value: The new approach for measurement of organizational ambidexterity using DEA is proposed in the paper. Different strategies including product ambidexterity and sustainability are estimated and their performances are compared. Knowledge management practices are used to justify the choice of ambidexterity strategies.

1. Introduction

Traditional value creation approaches no longer address all the emerging challenges for modern enterprises fully. Over the last two decades Entrepreneurial intensity (EI) has emerged a key issue of strategic management along with all types of innovation activities (Morris and Sexton, 1996). EI refers to different strategic decisions including product innovation, process innovation, expansion to new markets and business model innovation.

Preparing related decisions however requires well-structured and systematic information collection and analysis. This in turn forms part of the core features of company knowledge management. Knowledge management (KM) should not be confused with information technology: IT is an important enabler, for example in providing document management solutions, but knowledge management is a far wider subject. It represents an active approach to identifying, using and enhancing the tacit as well as the explicit and embodied capabilities and experiences of an organization. It represents a systematic and organized attempt to use knowledge within an organization to fulfil organizational objectives and enhance its value to stakeholders (organizational KM) (Becerra-Fernandez 2001). This could be enhanced by transforming its ability to store and use information, and developing the assets of the organization, new products and processes (technological KM) (Hit et al 2000; Gold and Arvind Malhotra 2001; Bonifacio et al 2000). In addition to organizational and technological KM literature often quotes ecological KM which is more targeted on natural resources and ecological developments over time for a completely different purpose than organizational and technological KM (Berkes et al 2000; Moller et al 2004; Usher 2000). The scope of ecological KM is in monitoring of ecological and natural resources and development instead of economically viable outcomes which is the case for technological and organizational KM.

In general KM requires that the entire organization is aligned to support the generation and sharing of knowledge (Kakabadse et al 2003). From the KM main basic duties descriptions it becomes that KM fulfils a supporting role for company innovation activities thus for long term corporate strategic development.. However innovation isn’t a one-time event but requires a continuous efforts to build and maintain a healthy innovation project pipeline which has the potential of exploitation and economic value generation. Still innovation is often related and tied people and tacit knowledge initially which makes KM an important asset for companies who need have an inherent interest in getting less dependent on individual people and their knowledge in order to safeguard a consistent innovation stream. In this regard KM is considered an approach which supports innovation activities in a broader sense by codifying and storing information and knowledge as to the extent possible and to provide people involved in innovation activities a support tool to use in daily operations.

Furthermore KM and it’s relevance to innovation can also be viewed in light of the organizational ambidexterity (OA) which is an organization’s ability to pursue several competing objectives at the same time (Adler et al., 1999; Porter, 1996). For example, the firm can be involved in process and product innovation simultaneously, distributing resources among them. This means that business processes can be made more efficient while also finding more customers and exploring new market niches with new products. In this case KM can serve as a necessary ingredient of such strategy allowing to use information about core products for development and distribution of new ones.

The framework of organizational ambidexterity was introduced by March (1991). March considered exploitation and exploration activities of firms and the competition between them. Exploitation activities incrementally and relatively quickly improve existing technologies and business processes aiming at rising efficiency and risk reduction. On the contrary, March posited that exploration refers to new opportunities in the distant future, increasing uncertainty and room for managerial flexibility. Exploration is close to the real-option approach in strategic management practice (e.g. Dortland et al., 2014). Innovativeness and risk-taking depend on the success of previous innovative activities. An optimal balance or trade-off between exploitation and exploration determines organizational ambidexterity.

Developing March’s ideas, Gupta et al. (2006) argued that exploration and exploitation are mutually enhancing for organizational performance. Many researchers (Gibson and Birkinshaw, 2004; He and Wong, 2004; Lubatkin et al., 2006; Raisch et al., 2009; Simsek, 2009) agree with them and empirically show that organizational ambidexterity is beneficial for a firm’s efficiency. However, some studies (Atuahene-Gima, 2005) documented a negative effect. Following March’s approach and the above literature, in this paper we study the impact of OA and distinguish between the short-term and long-term effects for firms.

There are many approaches to measure the impact on efficiency. It can be estimated using organizational performance measures (Murphy et al., 1996). Short-term effects can be discovered by looking at accounting performance measures such as profit margins, return on assets, return on investment, etc. Narrower product performance can be revealed through sales growth and market share. More sophisticated back-looking measures, including total shareholder return, economic value added and etc. are value-based and take into account shareholders’ risks. Financial market measures such as trailing EPS and market capitalization are forward-looking, but capture mostly short -term effects according to investors’ expectations. Richard et al. (2009) distinguish mixed measures: cash flow divided by the number of shares (CF per share), marketto-book value, and Tobin’s Q. Maditinos et al. (2011) highlight the plausible properties of market-to-book value compared to financial accounting and market measures because it is not only forward-looking but can also be a proxy for future growth opportunities.

The impact on organizational performance can be also considered from the perspective of innovative activities and EI. Then such impact is called innovative performance which is a measure of EI efficiency. Griliches (1981) suggested that product and process innovation have a positive effect on the long-term operating performance and should increase the market value. Empirical evidence has showed a positive impact of innovations measured via patent indicators on value and long-term performance (Bessler and Bittelmeyer, 2008). R&D expenditures (Coombs and Bierly III, 2006), patent counts, patent citations (Narin et al., 1987), new product announcements (Iversen et al., 2007) are useful proxies for innovativeness. Coombs and Bierly III (2006) underline the lagged relationship between R&D expenses and patents, since patents are obtained at the earlier stages of R&D projects. Narin et al. (1987, p. 144) stated that the number of patents is “a better indicator of corporate commitment to pursue innovation than the actual amount of innovation”. Hagedoorn and Cloodt (2003) argued that a one-indicator approach is more appropriate for high-tech industries, although pharmaceuticals need a composite indicator to capture the multidimensionality of innovative performance.

Organizational effectiveness may go beyond organizational and innovative performance to include external measures that are not associated with economic valuation for traditional stakeholders: shareholders, managers, or customers (Richard et al., 2009). Such external measures may be corporate social responsibility. Long-term efficiency can be related also to sustainable development. This idea is reflected in the relevant literature. For example, Chen et al. (2014) conducted interviews with managers and showed a positive effect of sustainability goals on organizational and innovative performance. Du et al. (2013) also stressed organizations’ new focus on sustainable development.

1. مقدمه

2. رویکردها برای سنجش میزان دوسو توانی سازمانی در حوزه انرژی و داروسازی

2.1. راندمان کوتاه مدت و بلند مدت

2.2. سهم محصولات اصلی و مختل کننده

2.3 سودآوری در مقابل پایداری

3. شواهد تجربی از بخش انرژی

3.1 بازده کوتاه مدت و بلند مدت

3.2 سهم محصولات اصلی و مختل کننده

3.3 توسعه پایدار

4. شواهد تجربی از بخش داروسازی

4.1 بازده کوتاه مدت و بلند مدت

4.2. سهم محصولات اصلی و مختل کننده

4.3 توسعه پایدار و OA

5. نتیجه گیری و پیامدها

منابع

1. Introduction

2. Approaches to measuring Organizational Ambidexterity in Energy and Pharmaceuticals

2.1. Short-term and long-term efficiency

2.2. Share of core and disruptive products

2.3. Profitability vs. sustainability

3. Empirical evidence from the energy sector

3.1. Short and long term efficiency

3.2. Share of core and disruptive products

3.3. Sustainable development

4. Empirical evidence from the pharmaceutical sector

4.1. Short and long-term efficiency

4.2. Share of core and disruptive products

4.3. Sustainable development and OA

5. Conclusion and implications

References