دانلود رایگان مقاله نظارت بانکداری و حسابرسان خارجی

چکیده

این مقاله نقش حسابرسان خارجی در نظارت بخش بانکداری را از چشم انداز سازمانی و تجربی بررسی می کند. اولا، یک چهارچوب کارگزار – کارفرما ساده را ارائه می دهیم که اهمیت چندین مشخصه سازمانی را در تعیین شمول بهینه حسابرسان خارجی در نظارت مورد تاکید قرار می دهد. آنگاه یک شاخص جدید را می سازیم که درجه ای از درگیری حسابرسان خارجی در نظارت بخش بانکداری در 115 کشور را بدست می آورد. سازگار با استدلال های نظری خود، در می یابیم، کشورهایی که نقش بانک های مرکزی را در نظارت افزایش می دهند، هم چنین بیشتر احتمال دارد، حسابرسان را بکار گیرند، این امر حاکی از این است، پیچیدگی مضاعف یک کارکرد نظارت، احتمالا از تخصص یک حسابرس خارجی بهره می برد. هم چنین تجربه داشتن یک بحران مالی به استفاده بالاتر حسابرسان وابسته است، به طور خاص در بین بانک های مرکزی دارای یک نقش فزاینده در نظارت است که برخی دغدغه های اعتبار ناظر را پیشنهاد می دهد. نهایتا، نشان می دهیم کیفیت حسابرسی بالاتر به یک مشارکت مضاعف حسابرسان در نظارت وابسته است.

1. مقدمه

پس از بحران مالی جهانی سال 2008، محققان و سیاستگذاران مثل هم، به ضعف چارچوب های نظارت بانکداری به عنوان یکی از دلایل پیشتاز این بحران اشاره نموده اند. یک فناوری نظارت موثر باید کاملا پیش از تهدیدهای بالقوه برای امنیت و سلامت بخش بانکداری کشف شود. تحقیقات قبلی، ابعاد گوناگون مقررات بانکداری را بررسی نموده اند که میتواند چنین اهدافی را بدست آورد من جمله شرایط لازم سرمایه بانکداری، تدابیر نظارتی وام های ناکارامد، و مقررات یا شرایط لازم افشا. با این حال، به بعد مهم دیگر بخش نظارت، توجه اندکی شده است، یعنی استفاده از حسابرسان خارجی در اجرای وظایف نظارت بانکی ویژه.

مشارکت حسابرسان به عنوان دروازه بانان مالی خصوصی میتواند اعتبار فضای نظارت کلی را بهبود دهد زیرا عموما حسابرسان از یک تاثیر مفید بر رفتار شرکت های نظارت شده یا بانک ها در این مورد برخوردارند. به این خاطر، ابتکار عمل های بیشماری در زمینه چارچوب نظارتی جهانی (همانند کمیته بیسل در زمینه نظارت بانکداری، 2008، 2014)، یک رابطه تنگ بین ناظران بانکداری و حسابرسان خارجی، یک تبادل اطلاعات موثر را توصیه نموده اند. ناظر، می تواند از حسابرسان خارجی، انجام انواع مختلف تکالیف را درخواست نماید، گاهی اوقات از گزارش حسابرسی استاندارد، فراتر رود. با این حال، درگیری بازیگران خصوصی در اجرای وظایف عمومی می تواند خطراتی را در بر داشته باشد. به عنوان مثال، ممکن است ناظر، هزینه های اعتباری را ببار آورد، با فرض اینکه حسابرسان، شرکت های خصوصی دارای روابط نزدیک به طور بالقوه برای موسسات مالی نظارت شده هستند. به طور مشابه، کیفیت مورد انتظار گزارشات حسابرسی، اطمینان نسبی را تعریف می کند که با آن ناظران می توانند به اطلاعاتی اعتماد کنند که حسابرسان منتشر می کنند.

در این مقاله یک چارچوب کارفرما – کارگزار (وکیل و موکل) ساده را ارائه می نماییم که هزینه ها و منافع مشارکت حسابرسان خارجی در نظارت بانک را مورد تاکید قرار می دهد. نشان می دهیم، مشارکت بهینه حسابرسان خارجی به چندین عامل سازمانی و ویژه کشور بستگی دارد. اعم از : 1) مزایای مورد انتظار بر حسب نظارت بخش مالی موجب شده توسط حسابرس، 2) کیفیت کارکرد حسابرسی و 3) هزینه های ادراک شده مشارکت حسابرس، همانند نگرانی های اعتباری. آنگاه این فرضیه را به لحاظ تجربی محک می زنیم، با اتخاذ یک رویکرد مثبت و بررسی این مساله که آیا سطح واقعی درگیری حسابرس در مجموعه وسیعی از کشورها به مشخصات سازمانی ویژه – کشور مورد تاکید در مدل خود، مربوط است یا خیر.

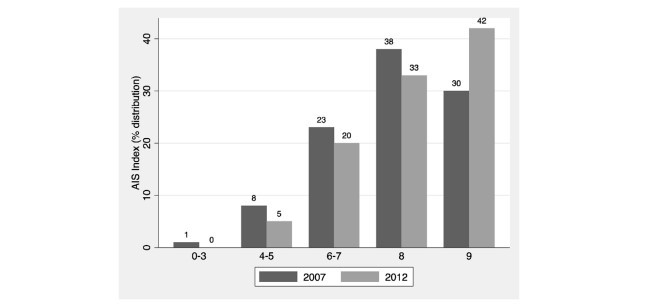

بدین منظور، اولا، یک سنجش جدید را گسترش می دهیم که میزان درگیری حسابرسان در نظارت را حساب می کند که آن را شاخص AIS می نامیم. این شاخص جدید مبتنی بر نه مشخصه سازمانی حسابرسی خارجی در بخش بانکداری در سرتاسر دنیا است همانطور که توسط بانک جهانی در سال های 2007 و 2012 بررسی شد. شاخص AIS را برای ارزیابی اصولی وضعیت نظارت بانک در یک نمونه وسیع متشکل از 115 کشور بکار می گیریم.

پی می بریم، کشورها عموما، سطوح بالای درگیری حسابرس را در نظارت می پذیرند، به طور متوسط 7.7 از حداکثر 9 امتیاز را در سال 2007 بدست می آوردند. با این وجود، این مشارکت حتی در سال 2012 افزایش هم پیدا کرد. کشورها، عموما نیاز دارند، حسابرسان خارجی با ناظر همکاری نزدیک داشته باشند، با این وجود، شرایط لازم، در زمینه اساسنامه و صلاحیت حسابرسان، کمتر واقع بینانه هستند.

آنگاه یک مجموعه از جایگزین ها (پروکسی) را برای هزینه ها و منافع مشارکتی حسابرسان در نظارت در چارچوب نظری ما، مورد تاکید قرار گرفت و اهمیت نسبی توضیح مشارکت مضاعف حسابرسان در نظارت بانکی مشاهده شده بین دو زمینه یابی بانک جهانی را مورد تاکید قرار می دهد. به این ترتیب، مدل مبنای ما، یک مدل لاجیت ترتیبی است که به تغییرات در شاخص AIS بین سالهای 2007 تا 2012 می نگرد. تحلیل ما، چندین دترمینان (عامل تعیین کننده) مشارکت حسابرسان در نظارت را مورد تاکید قرار می دهد. اولا، نشان می دهیم، کشورهای توصیف شده توسط سطوح پایین مشارکت حسابرس در سال 2007، بیشتر احتمال دارد آن را افزایش دهد که تمایل به سوی یک همکاری حتی بالاتر بین ناظران و حسابرسان خارجی را تایید می نماید. سپس، پی می بریم، کشورهایی که نقش بانک های مرکزی را در نظارت از سال 2007 تا 2012 افزایش داده اند، بیشتر احتمال دارد، دارای یک مشارکت بالاتر حسابرسان در نظارت باشند، حاکی از این امر است، پیچیدگی مضاعف یک کارکرد نظارت، احتمالا از تخصص یک حسابرس خارجی بهره می برد.

از این گذشته، بررسی می کنیم آیا یک بحران بانکداری سیستمیک، به عنوان یک جایگزین برای دغدغه های بالاتر ناظر، بر احتمال مشارکت حسابرسان خارجی در نظارت تاثیر دارد یا خیر. در می یابیم، این مساله صادق است، لیکن تنها در کشورهایی که مسئولیت نظارت بیشتری را به بانک های مرکزی خود تفویض نموده اند، مبنی بر اینکه پیچیدگی مضاعف یک کارکرد نظارت، احتمالا از تخصص یک حسابرس خارجی بهره می برد. این نتایج در ادبیاتی همبخشی دارد که نقش بحرانهای مالی در شکل دهی فضاهای نظارتی و سازمانی را مورد مطالعه قرار می دهد (آثار Masciandaro et al., 2013, Masciandaro Romelli, 2018 و Abascal and Gonzales, 2019 را در بین سایر آثار، ملاحظه نمایید). در نهایت، همراستا با مدل نظری، هم چنین نشان می دهیم، کیفیت حسابرسی بالاتر جایگزین از طریق یک نظارت دقیق اقدامات حسابرسان به یک مشارکت بیشتر حسابرسان در نظارت بخش بانکداری وابسته است.

این نتایج برای مجموعه ای از بررسی های حساسیت من جمله تعاریف گوناگون شاخص AIS، مشخصات تجربی دیگر و راهبردهای تحریف، قوی هستند. طبق دانش ما، این مقاله، اولین مقاله ای است که رابطه بین حسابرسی خارجی و نظارت بانکداری را از یک چشم انداز نظری، سازمانی و تجربی تحلیل می نماید. یافته های ما، شباهتها و تفاوتها در فضای نظارت پیرامون دنیا را آشکار می سازند. چنین دانشی میتواند به طور خاص برای ارزیابی درجه همگرایی بین معماری های نظارت ملی در جوامع تازه تاسیس شده ناظران بانکداری، مفید باشد، همانطور که این مساله در اتحادیه اروپا صدق می کند.

Abstract

This paper investigates the role of external auditors in banking sector supervision from a theoretical, institutional and empirical perspective. We first present a simple principal-agent framework that highlights the importance of several institutional characteristics in determining the optimal involvement of external auditors in supervision. We then construct a new index that captures the degree of involvement of external auditors in the oversight of the banking sector in 115 countries. Consistent with our theoretical arguments, we find that countries that increase the role of central banks in supervision are also more likely to involve auditors, suggesting thatthe added complexity of a supervisory function is likely to benefit from the expertise of an external auditor. Having experienced a financial crisis is also associated with a higher use of auditors, particularly among central banks with an increasing role in supervision, which suggests some reputational concerns of the supervisor. Finally, we show that higher audit quality is associated with an increased involvement of auditors in supervision.

1. Introduction

In the aftermath of the 2008 Global financial crisis, researchers and policymakers alike have pointed to the weakness of banking supervisory frameworks as one of the leading causes of the crisis (see Merrouche and Nier, 2010; Kupiec et al., 2017). An effective supervision technology ought to detect, well in advance, potential threats to the safety and soudness of the banking sector. Previous research has explored various aspects of banking regulation that can achieve such objectives, including bank capital requirements, regulatory treatments of non-performing loans and provisions or disclosure requirements.1 However, little attention has been directed towards another important aspect of financial sector oversight, i.e. the use of external auditors in the implementation of specific banking supervisory tasks.

The involvement of auditors, as private financial gatekeepers, can improve the credibility of the overall supervisory setting, as auditors generally have a beneficial influence on the behaviour of regulated firms, or banks in this case.2 For this reason, numerous initiatives on the global regulatory framework (such as the Basel Committee on Banking Supervision, 2008, 2014) have recommended a tight relationship between banking supervisors and external auditors to enable an effective information exchange. The supervisor can request external auditors to perform different kinds of tasks, at times going beyond the standard audit report. However, the involvement of private actors in implementing public tasks can carry risks. For example,the supervisor can incur reputational costs given that auditors are private firms with potentially close ties to the regulated financial institutions. Similarly, the expected quality of the auditing reports defines the relative confidence with which supervisors can trust the information that auditors release.

In this paper, we present a simple principal-agent framework that highlights the costs and benefits of involving external auditors in banking supervision.We show thatthe optimal involvement of external auditors depends on several institutional and countryspecific factors. These include: (i) the expected benefits in terms of financial sector oversight brought on by the auditor, (ii) the quality ofthe auditing function and (iii)the perceived costs of auditor involvement, such as reputational concerns. We then test this hypothesis empirically by taking a positive approach and investigating whether the actual level of auditor involvement in a broad set of countries is related to the country-specific institutional characteristics underlined in our model.

To this end, we first develop a new measure that captures the level of Auditors’ Involvementin Supervision, which we callthe AIS Index. This new index is based on nine institutional characteristics of external auditing in the banking sector across the world, as surveyed by the World Bank in 2007 and 2012. We employ the AIS Index to systematically assess the state of banking supervision in a large sample of 115 countries.

We find that countries generally adopt high levels of auditor involvement in supervision, scoring on average 7.7 out of a maximum of 9 points, in 2007. Nonetheless, this involvement has increased even further in 2012. Countries generally require that external auditors cooperate closely with the supervisor, however less stringent requirements are in place regarding the statute and qualification of the auditors.

We then provide a series of proxies for the costs and benefits of involving auditors in supervision highlighted in our theoretical framework and investigate their relative importance in explaining the increased involvement of auditors in banking supervision observed between the two World Bank surveys. As such, our baseline model is an ordered logit model that looks at the changes in the AIS index between 2007 and 2012. Our analysis highlights several key determinants of auditors’ involvementin supervision. First, we show that countries characterized by lower levels of auditor involvement in 2007 are more likely to increase it, confirming the tendency towards an ever-higher collaboration between supervisors and external auditors. Next, we find that countries that have increased the role oftheir central banks in supervision from 2007 to 2012 are also more likely to have a higher involvement of auditors in supervision, suggesting that the added complexity of a supervisory function is likely to benefit from the expertise of an external auditor.

We also investigate if having experienced a systemic banking crisis, as a proxy for higher reputational concerns of the supervisor, affects the likelihood of involving external auditors in supervision. We find that this is the case, but only in countries that also assigned more supervisory responsibility to their central bank, suggesting that the added complexity of a supervisory function is likely to benefit from the expertise of an external auditor. These results contribute to the literature that studies the role of financial crises in shaping supervisory and institutional settings (see Masciandaro et al., 2013, Masciandaro and Romelli, 2018 and Abascal and Gonzales, 2019, among others). Lastly, in line with our theoretical model, we also show that higher audit quality, proxied by a tight oversight of auditors’ actions, is associated with an increased involvement of auditors in banking sector supervision.

These results are robustto a series of sensitivity checks including various definitions of the AIS index, alternative empirical specifications and falsification strategies. To the best of our knowledge, this is the first paper to analyse the relationship between external auditing and banking supervision from a theoretical, institutional and empirical perspective. Our findings shed light on the similarities and differences in the supervisory setting around the world. Such knowledge can be particularly useful to assess the degree of convergence among national supervisory architectures in newly established communities of banking supervisors, as it is the case in the European Union (Masciandaro et al., 2011).

چکیده

1. مقدمه

2. طراحی بهینه فضاهای نظارت

2.1 بازیگران: سیاستگذاران، ناظران، بانک ها و حسابرسان

2.2 نظارت بدون حسابرسی

2.3 نظارت با حسابرسی

3. چارچوب سازمانی

3.1 مشارکت حسابرسان در شاخص نظارت

3.2 مشارکت حسابرسان در نظارت: یک مرور کلی

4. تجربیات

4.1 نتایج اصلی

4.2 تحلیل مولفه اصلی

4.3 نقش استقلال بانک مرکزی

4.4 بررسی های نیرومندی و علیت

5. نتیجه گیری

منابع

ABSTRACT

1. Introduction

2. Optimal design of supervisory settings

2.1. The players: policymakers, supervisors, banks and external auditors

2.2. Supervision without auditing

2.3. Supervision with auditing

3. Institutional Framework

3.1. The auditors’ involvement in supervision index

3.2. Auditors’ involvement in supervision: an overview

4. Empirics

4.1. Main results

4.2. Principal component analysis

4.3. The role of central bank independence

4.4. Robustness checks and causality

5. Conclusion

References