دانلود رایگان مقاله آیا در چین مدیران مستقل میتوانند کیفیت کنترل داخلی را بهبود بخشند؟

چکیده

این مطالعه قدرت نظارت مدیران مستقل (IDS) را بعنوان ترکیبی از تخصص متخصص و یا شایستگی، انگیزه، قدرت حفظ تعادل و سعی و کوشش مفهومی سازی میکند. پس از آن به صورت تجربی بررسی تاثیر قدرت نظارت ID بر کیفیت کنترل داخلی (ICQ)، را بررسی میکند که توسط افشای داوطلبانه گزارش حسابرسان درمورد کنترل داخلی و بیانیه های مالی منتشر شده توسط شرکتهای سهم A چینی در طول 2006-2010 پروکسی خواهد شد. ما می بینیم که شاخص قدرت نظارت ID ترکیبی دارای اثر مثبت و معنادار بر ICQ است، که برای پروکسی های مختلف برای ICQ قوی است، و اجزای آن نیز بطور مثبت و معنادار با هم و یا (در اکثر موارد) هر دو اقدامات ICQ مرتبط است. در مجموع، شواهد ما نشان می دهد که قدرت نظارت ID ها، نقش مثبتی در بهبود ICQ در چین بازی می کند.

1. مقدمه

از زمان افشای رسوایی بزرگ شرکت های بزرگ مانند موارد موثر بر انرون و ورلدکام، تنظیم کننده های اوراق بهادار در بسیاری از کشورها توجه دقیقی به چگونگی ایجاد یک سیستم کنترل داخلی موثر کرده اند. به عنوان مثال، در جولای 2002، کنگره آمریکا قانون آکسلی ساربنز (SOX) را تصویب کرد. بخش 404 از قانون مدیریت شرکتهای دولتی را ملزم به ارزیابی اثربخشی کنترل داخلی خود و روش های گزارشگری مالی و ارائه گزارش حسابرسان در اثربخشی کنترل داخلی کرده است. فراوانی شواهد تجربی نشان می دهد که کنترل داخلی مؤثر می تواند کیفیت گزارشگری مالی را ارتقاء دهد.

در راستای این روند بین المللی اخیر، تنظیم کننده های چینی ایجاد سیستم های کنترل داخلی در شرکت های عمومی را تسریع بخشیدند. آنها یک سری از قوانین و مقررات را از سال 2006 صادر کرده اند. همراه با صدور این مقررات و در دسترس بودن اطلاعات مربوط، محققان در چین به طور فزاینده ای در عوامل موثر بر اثربخشی کنترل داخلی علاقه مند شدند.

یک رشته از متون کنترل داخلی به بررسی اثر حاکمیت شرکتی بر کیفیت کنترل داخلی (ICQ) می پردازد. ( برای مثال، Bronson, Carcello, and Raghunanhan 2006; Doyle, Ge, and McVay 2007; Fang, Sun, and Jin 2009; Goh 2009; Owusu-Ansah and Ganguli 2010; Johnstone, Li, and Purley 2011). حاکمیت شرکتی مؤلفه ی اصلی محیط کنترل است، پایه و اساس کنترل داخلی است. با این حال، ادبیات بر نقش مدیران مستقل (IDS) در هیئت نظارت بر مدیران (BoDs) و کمیته حسابرسی (به عنوان مثال کریشنان 2005) تمرکز دارد؛ ژانگ، ژو، و ژو 2007)، از نسبت شناسه در هیئت ها و کمیته حسابرسی برای اندازه گیری استقلال خود استفاده کردند. مطالعات قبلی نشان داده است که ویژگی هایی غیر از مدارک شناسایی، مانند پس زمینه های آموزشی، تجربه کاری، سعی و کوشش و شهرت، نقش مهمی در عملکرد شرکت های در چین دارند (به عنوان مثال تنگ، دو، و شن 2010؛ و همکاران 2011). با این حال، هیچ مطالعه ای این مسئله را آزمایش نکرده است که که آیا این ویژگی بر ICQ هم تاثیر می گذارد. این مطالعه نشان دهنده اولین گام به سوی رسیدگی به این مسئله است.

در کشورهای غربی مانند انگلستان، که در آن کنترل شرکت های بزرگ و سرمایه گذاران نهادی باعث ایجاد تابع نظارت قوی تر می گردد، شناسه ها در انجام وظایف نظارت تاثیر کمتری دارند(Guest 2009). در مقابل، در چین، مکانیسم های کنترل خارجی (برای مثال حفاظت از سرمایه گذار، قانون و اجرای قانون، حسابرسان خارجی) ضعیف در نظر گرفته می شوند (لی و همکاران 2012). در نتیجه، مکانیسم های داخلی به خصوص برای حاکمیت موثر شرکت های بزرگ حائز اهمیت هستند. شناسه شامل مکانیزم داخلی می شود. طبق قانون شرکت در چین، یک شرکت نیاز به هر دو ی BOD و هیئت ناظران دارد. وظیفه ی اصلی هیئت مدیره ی ناظران بررسی گزارش مالی شرکت می باشد؛ با این حال، هیئت ناظران در چین تا حد زیادی بی تاثیر هستند (شیائو، Dahya، و لین 2004؛ وو و همکاران 2013)، که به افزایش می دهد انتظارات از نقش ID ها در حاکمیت شرکتی و کنترل داخلی است.

برخی از مطالعات اخیر شواهدی مبنی بر تاثیر شناسه در چین فراهم می آورد. به عنوان مثال، شناسه برای افزایش کارایی بانک و کیفیت دارایی ها (لیانگ، خو، و Jiraporn 2013)، افزایش دقت پیش بینی های مدیریتی (آهنگ، جی، و لی 2013)، انجام وظایف نظارت بر هیئت مدیره اجرایی و مدیریت ارشد ( بو، تائو، و Sun 2013) و حفاظت از منافع سرمایه گذاران خارج (تنگ، رقیق، و هو 2013) مورد استفاده قرار می گیرد. با این حال، شواهدی وجود دارد که نشان می دهد که آنها بی اثر هستند. به عنوان مثال، لیو و لو (2004) اثبات می کنند که شناسه رای دادن در برابر دوستان مدیر اجرایی خود را در فرهنگ guanxi در چین را دشوار می سازد. وجود رسوایی های شایع بسیار شرکت این مشاهدات (چن، هو، و شیائو 2010) را تائید می کند. با توجه به شواهد مختلط، دامنه ای برای بررسی اثربخشی شناسه در حاکمیت شرکتی وجود دارد. این مطالعه، مطالعات قبلی شناسه را به موضوع مهم ICQ بسط می دهد.

واضح است که بسیاری از شناسه های لیست شده در شرکت های ذکر شده چینی دانشگاهیان هستند و صاحب صنعت و کسب و کار خاص و یا متخصص دانش نیستندکه برای انجام وظایف حاکمیت شرکتی آنها ضروری است (لی و همکاران 2012). به عنوان مثال، در مورد Zhenzhou Baiwen بدنام، استاد انگلیسی دانشگاه که وظایف ID خود را انجام نداد و 100.000 یوان جریمه شد. استاد اقرار کرد که هیچ دانش کسب و کار، و مخصوصا دانش حسابداری نداشته است (چن، هو، و شیائو 2010). آیا چنین دانشی از عوامل مهم مؤثر به حساب می آید بر نقشی که ID در کنترل داخلی بازی می کند؟ ما این مسئله را با بررسی رابطه بین پس زمینه مالی از شناسه و ICQ ذکر می کنیم. در همین حال، مشاهده می کنیم که اگر چه ممکن است شناسه از شرکتی که در آنها کار کرده غرامت دریافت کنند، که خسارت تا حد زیادی متفاوت است، اعم از 2000 تا 780000 یوان در هر سال در سال 2006. علاوه بر این، کمترین پرداخت شناسه بطور قابل توجهی مربوط به حضور کم در جلسات مربوط بود. این نشان می دهد که شناسه کم پرداخت ممکن است انگیزه برای تحقق نقش نظارتی خود را از دست بدهند. ما در مورد این که آیا و تا چه حد شناسه برای جبران انگیزه برای نقش آنها موثر است، تحقیق می کنیم.

تاریخ انتصاب شناسه در شرکت های چینی نسبتا کوتاه است. اوراق بهادار چین کمیسیون تنظیم مقررات (CSRC) یک، راهنمای جامع رسمی در شناسه از شرکت های داخلی ذکر شده تا سال 2001 تصویب نشده است. مقررات تصریح شده است که هیئت مدیره باید حداقل دو شناسه تا 30 ژوئن سال 2002، و حداقل یک سوم از اعضای هیئت مدیره باید تا 30 ژوئن 2003 دارای شناسه باشند. یکی از عوارض جانبی این شرط اجباری است که شرکت های ذکر شده ممکن است به سادگی شناسه مطابق با مقررات (چن و آل Najja 2012) منصوب کند. به عنوان یکی از اقدامات اخیر، شناسه نیز به یک فرایند یادگیری است، اما لازم است که به ارائه شواهد تجربی در مورد اینکه آیا افزایش سهم شناسه در هیئت مدیره می تواند به افزایش تعادل ICQ فراهم می کند.

مقررات حاکمیت شرکتی نیاز به شناسه برای انجام وظایف خود دارد. مواردی وجود دارد که در آن ها شناسه با شکست مواجه شده است به انجام این کار، چنانکه در مورد Zhenzhou Baiwen مذکور به همین صورت است. داده های نمونه ما حاکی از این است که اگر چه شناسه از برخی از اعضای هیئت مدیره در تمامی جلسات حضور داشتند، سایرین تنها در یک سوم جلسات حضور داشتند. آیا با استفاده از شناسه می توانند وظایف خود را انجام دهند؟ برای پاسخ به این سوال، ما رابطه سعی و کوشش و ICQ را بررسی می کنیم.

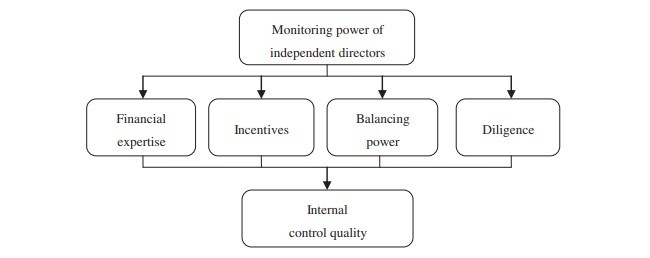

این مشاهدات برخی از ویژگی های جالب از شناسه در شرکت های ذکر شده چینی را برجسته می کند. این ویژگی ها و انتظارات بالا از نقش ID در حاکمیت شرکتی و کنترل داخلی آن را برای مطالعه مهم و جالب ساخته است این که آیا شناسه واقعا موثر است و می تواند نقش مورد انتظار خود را در حفظ و بهبود ICQ را انجام دهد. علاوه بر این، این ویژگی هر دو مربوط به قدرت و نظارت شناسه می شود. بنابراین، ما شاخص قدرت نظارتی برای شناسه، از چهار بعد ایجاد کردیم: تخصص مالی شناسه، انگیزه، حفظ تعادل قدرت و سعی و کوشش.

Abstract

This study conceptualises the monitoring power of independent directors (IDs) as consisting of specialist expertise or competence, incentives, balancing power and diligence. It then empirically investigates the influence of IDs’ monitoring power on internal control quality (ICQ), which is proxied by the voluntary disclosure of auditors’ reports on internal control and financial restatements released by China’s A-share firms during 2006–2010.We find that the combined ID monitoring power index has a positive and significant effect on ICQ, which is robust to different proxies for ICQ, and that its components are also positively and significantly associated with either or (in most cases) both measures of ICQ. Overall, our evidence indicates that IDs’ monitoring power plays a positive role in improving ICQ in China.

1. Introduction

Since the exposure of major corporate scandals such as those affecting Enron and WorldCom, securities regulators in many countries have paid close attention to how to establish an effective internal control system. For example, in July 2002, the US Congress enacted the Sarbanes– Oxley Act (SOX). Section 404 of the Act requires the managements of public firms to assess the effectiveness of their internal control and financial reporting procedures and to provide auditors’ reports on the effectiveness of internal control. There is an abundance of empirical evidence demonstrating that effective internal control can enhance financial reporting quality (e.g. Doyle, Ge, and McVay 2007; Ashbaugh-Skaife et al. 2008).

In line with this recent international trend, China’s regulators are hastening the construction of internal control systems in public firms. They have issued a series of rules and regulations since 2006. Along with the issuance of these regulations and the availability of related data, researchers in China are becoming increasingly interested in the factors that influence the effectiveness of internal control.

One strand of the internal control literature explores the effect of corporate governance on internal control quality (ICQ) (e.g. Bronson, Carcello, and Raghunanhan 2006; Doyle, Ge, and McVay 2007; Fang, Sun, and Jin 2009; Goh 2009; Owusu-Ansah and Ganguli 2010; Johnstone, Li, and Purley 2011). Corporate governance is a basic element of the control environment, which is the foundation of internal control. However, the literature focuses on the role of independent directors (IDs) in monitoring boards of directors (BoDs) and audit committees (e.g.Krishnan 2005; Zhang, Zhou, and Zhou 2007), and uses the proportion of IDs on boards and audit committees to measure their independence. Previous studies have found that other characteristics of IDs, such as educational background, work experience, diligence and reputation, have important effects on corporate performance in China (e.g. Tang, Du, and Shen 2010; Ye et al. 2011). However, no studies have tested whether these characteristics also affect ICQ. This study represents a first step towards addressing that issue.

In Western countries such as the UK, where corporate control and institutional investors perform a stronger monitoring function, IDs are less effective in carrying out monitoring functions (Guest 2009). In contrast, in China, external control mechanisms (e.g. investor protection, law and law enforcement, external auditors) are considered weak (Li et al. 2012). As a result, internal mechanisms are particularly important for effective corporate governance. IDs comprise such an internal mechanism. Under China’s Company Law, a corporation is required to have both a BoD and a board of supervisors. The main functions of a board of supervisors are to review a company’s financial reports; to monitor its directors and managers to ensure they are not violating the Company Law or Charter; and to require the company to correct behaviour that may harm shareholder interests. However, boards of supervisors in China are largely ineffective (Xiao, Dahya, and Lin 2004; Wu et al. 2013), which raises the expectations of the role of IDs in corporate governance and internal control.

Some recent studies provide evidence that IDs are effective in China. For example, IDs are found to increase bank performance and asset quality (Liang, Xu, and Jiraporn 2013), increase the accuracy of management forecasts (Song, Ji, and Lee 2013), perform oversight functions over executive board directors and senior management (Bo, Tao, and Sun 2013) and protect the interests of outside investors (Tang, Du, and Hou 2013). However, there is also evidence to suggest that they are ineffective. For example, Liu and Lu (2004) document that IDs find it difficult to vote against their executive director friends in China’s guanxi culture. The existence of many highly publicised corporate scandals supports these observations (Chen, Hu, and Xiao 2010). Given the mixed evidence, there is scope for investigating the effectiveness of IDs in corporate governance. This study extends previous studies on IDs to the important issue of ICQ.

It is well known that many IDs in listed Chinese firms are academics and do not possess industry- and business-specific or specialist knowledge, which is essential for fulfilling their corporate governance roles (Li et al. 2012). For example, in the notorious Zhenzhou Baiwen case, a university English professor failed to perform his ID duties and was fined 100,000 yuan. The professor admitted to having no business knowledge, especially accounting knowledge (Chen, Hu, and Xiao 2010). Is such knowledge an important factor affecting the role an ID plays in internal control? We address this issue by exploring the relationship between the financial backgrounds of IDs and ICQ. Meanwhile, we observe that although IDs may receive compensation from the firms they serve, that compensation varies greatly, ranging from 2000 to 780,000 yuan per year in 2006. Further, the lowest paid IDs were significantly related to low attendance at meetings. This indicates that lowly paid IDs may lack the incentive to fulfil their monitoring roles. We investigate whether and to what extent IDs are incentivised to fill those roles.

The history of appointing IDs in Chinese firms is relatively short. The China Securities Regulatory Commission (CSRC) did not enact a formal, comprehensive guideline on IDs of domestically listed firms until 2001. The regulations stipulated that boards must have at least two IDs by 30 June 2002, and at least one-third of the board members should be IDs by 30 June 2003. One side effect of this compulsory requirement is that listed firms may simply appoint IDs to comply with regulations (Chen and Al-Najja 2012). As a recent practice, IDs are also subjected to a learning process, but it is necessary to provide empirical evidence on whether increasing the proportion of IDs on a board can provide more balancing power to improve ICQ.

The corporate governance regulations require IDs to perform their duties diligently. There have been cases in which IDs have failed to do so, as in the aforementioned Zhenzhou Baiwen case. Our sample data show that although the IDs of some boards attended every board meeting, others attended only one-third. Can IDs fulfil their duties by performing their duties diligently? To answer this question, we examine the relationship between diligence and ICQ.

These observations highlight some interesting features of the IDs in listed Chinese firms. These features and the high expectations of the role of ID in corporate governance and internal control make it interesting and important to study whether IDs are truly effective and can fill their expected roles in maintaining and improving ICQ. In addition, these features both relate to and constitute IDs’ monitoring power. Therefore, we construct an index of IDs’ monitoring power from four dimensions: IDs’ financial expertise, incentives, balancing power and diligence.

1. مقدمه

2. پیشینه نهادی و بررسی ادبیات

2.1 پیشینه نهادی

2.2. بررسی نوشته ها

3. تجزیه و تحلیل نظری و تدوین فرضیه

4. طرح پژوهش

4.1 مدل و متغیرهای

4.2 انتخاب نمونه

5. نتایج تجربی

5.1 آمار توصیفی

5.2 نتایج چند متغیره

6. چک پایداری

6.1 برآورد ابزاری متغیر

6.2 تست جفت نمونه

6.3 جایگزینی متغیر وابسته

6.4 جایگزینی متغیر مستقل

7. نتایج و الزامات

منابع

1. Introduction

2. Institutional background and literature review

2.1 Institutional background

2.2 Literature review

3. Theoretical analysis and hypothesis formulation

4. Research design

4.1 Models and variables

4.2 Sample selection

5. Empirical results

5.1 Descriptive statistics

5.2 Multivariate results

6. Robustness checks

6.1 An instrumental-variable estimation

6.2 Paired-sample test

6.3 Dependent variable substitution

6.4 Independent variable substitution

7. Conclusions and implications

References