دانلود رایگان مقاله اثر مقایسه حسابداری در مدیریت درآمد واقعی

چکیده

این مطالعه بررسی می کند چطور و چگونه فعالیت های مدیریت سود فرصت طلب مدیران با درجه ای از مقایسه حسابداری شرکت های خود با شرکت های دیگر را تحت تاثیر قرارمی دهند. با استفاده از نمونه های زیادی از شرکت های ایالات متحده، من متوجه شدم که مدیران مدیریت سود واقعی (REM) را افزایش می دهد. در حالی که مدیریت سود مبتنی بر اقلام تعهدی خود (AEM) با درجه ای از مقایسه حسابداری شرکت های خود با شرکت های دیگر را کاهش می دهد. من همچنین متوجه شدم که این رفتار فرصت طلبانه برای '' فرار "از AEM به REM مواجه با مقایسه حسابداری بیشتر کاهش می یابد زمانیکه اطلاعات 'محیط زیست شرکت ها و یا کیفیت حسابرسی بهتر است. این یافته ها برای آزمون حساسیت های مختلف قوی هستند از جمله جهت رسیدگی به درون زایی احتمالی از مقایسه حسابداری می باشد.

1. مقدمه

این مطالعه بررسی می کند چطور و چگونه فعالیت های مدیریت سود فرصت طلب مدیران با درجه ای از مقایسه حسابداری شرکت های خود با شرکت های دیگر را تحت تاثیر قرار می دهد . بسیاری از مطالعات اثر اتخاذ استاندارد حسابداری مشابه (به عنوان مثال، استانداردهای گزارشگری مالی بین المللی) در مقایسه ارقام حسابداری در سراسر شرکت در کشورهای مختلف را بررسی می کند (بارت و همکاران، 2008؛ لانگ و همکاران، 2010؛ دفاند و همکاران، 2011). محققان همچنین به طور گسترده اثر مقایسه حسابداری در نتایج مختلف مانند افشای مدیریت داوطلبانه، 'گسترش پوشش تحلیل گران و پیش بینی خواص، و ساختار سهام سرمایه گذاران نهادی را بررسی می کنند، (گونگ و همکاران، 2013؛ کینی و همکاران، 2009؛ دی فرانکو و همکاران، 2011؛ انگلبرگ و همکاران، 2016). با این حال، مقاله در مورد اثر مقایسه حسابداری، به ویژه در سراسر شرکت تحت نظام مشابه GAAP، در مدیریت درآمد مدیران اندک است. بنابراین این مطالعه قصد دارد تا این شکاف را از طریق بررسی که آیا میزان مدیریت سود فرصت طلب مدیران تحت تاثیر قرار می گیرد، پر کند یا خیر و چگونه انتخاب مدیران از روش مدیریت سود جایگزین، توسط مقایسه حسابداری تحت تاثیر قرار می گیرد.

دوره جاری درآمد را گزارش می دهد که می تواند به دو روش مختلف اداره می شود. اول، مدیران می توانند سود گزارش شده از طریق انتخاب تعهدی اختیاری کنترل کنند که تحت اصول پذیرفته شده حسابداری (GAAP) اجازه گزارش شده است. این مدیریت سود در مبنای تعهدی GAAP (آخرت AEM) عمدتا در انتهای یک دوره حسابداری رخ می دهد، پس از فعالیت های عملیاتی واقعی کامل می شود (زانگ، 2012). در حالی که آن بطور مستقیم میزان اقلام تعهدی حسابداری را تحت تاثیر قرار می دهد، AEM هیچ تأثیر مستقیمی بر جریان های نقدینگی ندارد. دوم، مدیران همچنین می توانند درآمد گزارش شده را با تنظیم فعالیت های واقعی کنترل کنند. به طور خاص، آنها می توانند زمان و مقیاس فعالیت های واقعی مانند فروش، تولید، سرمایه گذاری، و تامین مالی در سراسر دوره حسابداری در چنین شیوه هایی را تغییر دهد که هدف درآمد خاص می تواند برآورده شود. به عنوان مثال، گزارش درآمد می تواند به طور موقت با شتاب دادن به زمان تولید و برنامه فروش، با کاهش مخارج اختیاری، و / یا به تعویق انداختن زمان وقوع آنها افزایش یابد ( (2006، فعالیت های مدیریت عملیات واقعی مذکور که از شیوه های کسب و کار عادی با هدف اولیه کنترل درآمد دوره جاری منحرف و به مدیریت سود واقعی ارجاع داده می شود (پس از آن REM). بر خلاف AEM، REM می تواند عواقب مستقیم بر جریان های نقدی فعلی و آینده (و همچنین تعهدات حسابداری) داشته باشد، برای سرمایه گذاران به طور متوسط برای درک مشکل تر است، و به طور معمول کمتر منوط به نظارت خارجی و بررسی توسط حسابرسان، تنظیم کنندگان، و سایر ذینفعان بیگانه می شود (کوهن و همکاران، 2008).

در چارچوب های مفهومی خود برای گزارشگر مالی، FASB (2010) و IASB (2010) مقایسه را به عنوان مشخصه های کیفی اطلاعات مالی شناسایی می کنند که به کاربران امکان شناسایی و درک شباهت ها در، و تفاوت های میان، اقلام می دهد. با وجود این واقعیت که مقایسه حسابداری یکی از ویژگی های مهم کیفی است، تحقیقات تجربی انجام شده بر روی آن نسبتا کمیاب در مقایسه با دیگر ویژگی های در حسابداری است. یک دلیل این است که آن یک مفهوم نسبی یا تطبیقی، نه یک معیار مطلق و یا مستقل مانند دیگر ویژگی های حسابداری است. در نتیجه، آزمون تجربی برای مقایسه قابل پیگری است، به ویژه برای نمونه های زیادی از شرکت ها در داخل یک کشور، قبل از د فرانکو و همکاران (2011) یک اقدام قابل عملیاتی را توسعه دهند. من روش خود را به منظور بررسی اثر مقایسه حسابداری در مدیریت درآمد شرکت ها در این مقاله اتخاذ کردیم.

من انتظار دارم که فعالیت مدیران AEM محدود می شود زمانیکه حسابداری شرکت خود قابل مقایسه تر با آن از شرکت های عملیاتی دیگر در همان صنعت است. هدف اصلی مدیران انجام AEM فرصت طلب عملکرد واقعی خود با توجه به پنهان کردن مزایای کنترل خصوصی خود مبهم است (زینگالس، 1994؛ شلایفر و ویشنی، 1997؛ لوز و همکاران، 2003؛ هاو و همکاران، 2004). اگر مقدار حسابداری یک شرکت بیشتر قابل مقایسه با کسانی که از همسالان صنعت آن است، هزینه های نهایی برای خارجی ها (به عنوان مثال، سهامداران، بستانکاران، و تنظیم کننده) جمع آوری و روند اطلاعات حسابداری این شرکت های همکار کوچکتر می شود. در نتیجه، آنها می توانند عملکرد واقعی شرکت را با دقت بیشتری ارزیابی کنند به این دلیل که اطلاعات حسابداری شرکت های قابل مقایسه، ورودی اضافی با ارزش برای تجزیه و تحلیل اصول کسب و کار یک شرکت مورد سوال است. به عبارت دیگر، اطلاعات حسابداری شرکت برای شرکت کنندگان در بازار خارج شفاف تر می شود اگر مقایسه حسابداری خود را افزایش می دهد در نتیجه مشوق، و امکانات، فعالیت های AEM مدیران را کاهش می دهد.

همچنین انتظار دارم که فعالیت های REM مدیران در مقایسه شرکت های حسابداری خود افزایش خواهد یافت. مطالعات قبلی برشواهدی مستند می کند که شرکت از AEM تبدیل به REM در یک محیط نظارتی دقیق تر (به عنوان مثال، قانون ساربن-آکسلی) جهت برآورد اهداف درآمد خاص می شود ( اورت و واگن هوفر، 2005 کوهن و همکاران، 2008؛؛ کوهن و زارووین 2010). گسترش منطق در این مطالعه، مدیران تا حد زیادی به REM متکی خواهند بود اگر توانایی خود را برای AEM استفاده کنند که به طور قابل توجهی توسط مقایسه زیاد حسابداری شرکت های خود محدود می شود. با توجه به سطح سود گزارش شده برای پنهان کردن مزایای کنترل خصوصی خود لازم است، مدیران انگیزه قوی برای کاهش AEM داشته باشند با توجه به اینکه مقایسه حسابداری بالاتر با استفاده از افزایش REM آماده می شود.

اقدامات رگراسیون AEM و REM در برآورد مقایسه حسابداری توسط د فرانکو و همکاران (2011) توسعه یافته و دیگر عوامل تعیین کننده مدیریت سود از نمونه های زیادی از شرکت های ایالات متحده در طول دوره 1983-2012 استفاده می کند، من متوجه شدم که AEM کاهش می یابد اما REM با درجه ای از مقایسه حسابداری یک شرکت افزایش می یابد. این یافته برای استفاده از متغیرها AEM / REM امضا و یا بدون علامت قوی است. من همچنین متوجه شدم که این رفتار با '' فرار "از AEM به REM با توجه به مقایسه حسابداری بالاتر کاهش یافته است زمانیکه اطلاعات محیط زیست موسسه و / یا کیفیت حسابرسی بهتر شد.

این مطالعه به پیشینه موجود در مقایسه حسابداری و مدیریت سود به شیوه های مختلف کمک می کند. اول، به اعتقاد من، این اولین مطالعه برای تاثیر مقایسه حسابداری در مدیریت درآمد است. مقایسه حسابداری بر اساس تاثیر آن بر افشای داوطلبانه، خواص پیش بینی تحلیلگر و یا انتخاب سهام سرمایه گذار بررسی شده است. همچنین مقالات فراوان عوامل تعین کننده مختلف مدیریت سود را تجزیه و تحلیل می کند. با این حال، شواهد محدود در مورد رابطه بین مقایسه حسابداری و مدیریت سود، تا حدی به دلیل مشکل در اندازه گیری تجربی مقایسه حسابداری وجود دارد. با استفاده از برآورد تجربی د فرانکو و همکاران (2011)، این مطالعه بطورنسبی عرصه تحقیقات بهره برداری نشده را توضیح می دهد. دوم، این مقاله پیشینه تحقیق در مورد REM را غنی می کند. در مقایسه با AEM، REM یک موضوع جدید است که محققان به طور فزاینده به آن توجه می کنند. گروهی از عوامل انتخاب و یا تجارت مدیران را بین AEM و REM در مطالعات قبلی تحت بررسی قرار می گیرد اما مجموعه ای جامع از عوامل تعین کننده برای تعویض و یا متمم خود هنوز شناسایی نشده است. این مقاله یک عامل جدید یعنی - مقایسه حسابداری - به عنوان یک علت یا انگیزه مهم برای جایگزینی REM برای AEM به توده ای از شواهد قبلی می افزاید. سوم، این مطالعه دامنه تحقیقات مقایسه حسابداری را گسترش می دهد. تا کنون، مقایسه حسابداری به طور عمده از نظر ورودی حسابداری مانند استانداردهای حسابداری یا روش های مطالعه قابلیت قیاس برای مقایسه ویژگی های حسابداری شرکت در یک کشور تحت یک رژیم GAAP خاص با مواردی که در کشور های دیگر تحت یک رژیم GAAP مختلف مفید است. به هر حال، آن برای مقایسه ویژگی های حسابداری و یا پیامدهای اقتصادی در سراسر شرکت در یک کشور تک (به عنوان مثال، ایالات متحده) در رژیم GAAP مشابه با استفاده از این مقایسه مبتنی بر ورودی سخت است. د فرانکو و همکاران (2011) تلاش کردند تا این محدودیت را با بهره برداری اندازه گیری مقایسه حسابداری مبتنی بر خروجی بررسی کنند و متوجه شدند اینکه آن بخوبی کار می کند تا رفتار انتخاب شرکت تحلیلگران و خواص پیش بینی آنها را توضیح دهد. این مطالعه سودمندی اندازه گیری مقایسه خود را با بررسی اثر آن بر روی یک موضوع حسابداری سنتی محبوب تست می کند، یعنی، مدیریت سود، و اعتبار تجربی از اندازه گیری را تأیید می کند.

این مقاله یک مفهوم سیاست نیز است. مقایسه ویژگی های کیفی مهم است که تنظیم کننده گان نگران هستند. آن هزینه مقایسه صورتهای مالی یک شرکت را با دیگران کاهش می دهد، به موجب آن در نتیجه شفافیت گزارش مالی شرکت را افزایش دهد. آیا در نظر گرفته شده است یا خیر، افزایش مقایسه کاهش AEM را به ارمغان می آورد که، با این حال، توسط REM جایگزین می شود. اگر تنظیم کننده گان استانداردهای حسابداری و یا سیاست ها را برای افزایش قابلیت مقایسه تنظیم کنند، آنها نیاز دارند تا اثر آن بر مدیریت سود را به طور کلی بدانند، و در جایگزین بین AEM و REM در خاص، تا هدف مقررات حاصل شود.

Abstract

This study investigates whether and how managers’ opportunistic earnings management activities are affected by the degree of their firms’ accounting comparability with other firms. Using a large sample of U.S. firms, I find that managers’ real earnings management (REM) increases whereas their accrual-based earnings management (AEM) decreases with the degree of their firms’ accounting comparability with other firms. I also find that this opportunistic behavior to ‘‘escape” from AEM to REM facing higher accounting comparability is mitigated when firms’ information environment and/or audit quality are better. These findings are robust to various sensitivity tests including the one to address the possible endogeneity of accounting comparability.

1. Introduction

This study investigates whether and how managers’ opportunistic earnings management activities are affected by the degree of their firms’ accounting comparability with other firms. Many studies examine the effect of adopting the same accounting standard (e.g., International Financial Reporting Standards) on the comparability of accounting numbers across firms in different countries (Barth et al., 2008; Lang et al., 2010; DeFond et al., 2011). Researchers also extensively investigate the effect of accounting comparability on various outcomes such as management’s voluntary disclosure, analysts’ coverage expansion and forecast properties, and institutional investors’ portfolio structure (Gong et al., 2013; Kini et al., 2009; De Franco et al., 2011; Engelberg et al., 2016). However, the paper on the effect of accounting comparability, especially across firms under the same GAAP regime, on managers’ earnings management is scant. This study thus aims to fill this gap by exploring whether the extent of managers’ opportunistic earnings management is influenced, and how managers’ choice of alternative earnings management methods is affected, by accounting comparability.

Current-period reported earnings can be managed in two different ways. First, managers can manipulate reported earnings through discretionary accrual choices that are allowed under the Generally Accepted Accounting Principles (GAAP). This within-GAAP accrual-based earnings management (hereafter AEM) typically occurs toward the end of an accounting period, after most real operating activities are completed (Zang, 2012). While it directly influences the amount of accounting accruals, AEM has no direct effect on cash flows. Second, managers can also manipulate reported earnings by adjusting real activities. Specifically, they can alter the timing and scale of real activities such as sales, production, investment, and financing throughout the accounting period in such a way that a specific earnings target can be met. For example, reported earnings can be temporarily boosted by accelerating the timing of production and sales schedules, by cutting discretionary expenditures, and/or by deferring the timing of their occurrences. Following Roychowdhury (2006), these real operation management activities that deviate from normal business practices with the primary objective of manipulating current-period earnings are referred to as real earnings management (hereafter REM). Unlike AEM, REM can have direct consequences on current and future cash flows (as well as accounting accruals), are more difficult for average investors to understand, and are normally less subject to external monitoring and scrutiny by auditors, regulators, and other outside stakeholders (Cohen et al., 2008).

In their conceptual frameworks for financial reporting, the FASB (2010) and IASB (2010) identify comparability as the qualitative characteristic of financial information that enables users to identify and understand similarities in, and differences among, items. Despite the fact that accounting comparability is one of important qualitative characteristics, the empirical research on it is relatively scarce compared with that on other accounting attributes. One reason is that it is a relative or comparative concept, not an absolute or independent criterion like other accounting characteristics. As a result, the empirical test for comparability has been intractable, especially for large sample of firms within a country, before De Franco et al. (2011) develop an operationalizable measure. I adopt their methodology to investigate the effect of accounting comparability on firms’ earnings management in this paper.

I expect that managers’ AEM activities are constrained when their firms’ accounting is more comparable with that of other firms operating in the same industry. The primary objective of managers conducting opportunistic AEM is to obfuscate their true performance with a view to concealing their private control benefits (Zingales, 1994; Shleifer and Vishny, 1997; Leuz et al., 2003; Haw et al., 2004). If a firm’s accounting amounts are more comparable with those of its industry peers, the marginal costs for outsiders (e.g., shareholders, creditors, and regulators) to collect and process accounting information of these peer firms become smaller. As a result, they can evaluate the firm’s true performance more accurately because the accounting information of comparable firms is a valuable additional input to analyze the business fundamentals of the firm in question. In other words, the accounting information of the firm becomes more transparent for outside market participants if its accounting comparability increases. The consequence is diminished incentives for, and possibilities of, managers’ AEM activities.

I also expect that managers’ REM activities will increase in their firms’ accounting comparability. Prior studies document the evidence that firms switch from AEM to REM under a more stringent regulatory environment (e.g., Sarbanes–Oxley Act) to meet certain earnings targets (Ewert and Wagenhofer, 2005; Cohen et al., 2008; Cohen and Zarowin, 2010). Extending this logic to this study, managers will rely on REM to a greater extent if their ability to use AEM is significantly curbed by their firms’ enhanced accounting comparability. Given the level of reported earnings necessary to conceal their private control benefits, managers have strong incentives to make up for the reduced AEM due to higher accounting comparability using the increased REM.

Regressing AEM and REM measures on the accounting comparability estimate developed by De Franco et al. (2011) and other earnings management determinants using a large sample of U.S. firms during 1983–2012 period, I find that AEM decreases but REM increases with the degree of a firm’s accounting comparability. This finding is robust to the use of signed or unsigned AEM/REM variables. I also find that this behavior of ‘‘escaping” from AEM to REM due to higher accounting comparability is mitigated when firms’ information environment and/or audit quality are better.

This study contributes to extant literature on the accounting comparability and earnings management in several ways. First, to my best knowledge, this is the first study for the impact of accounting comparability on earnings management. Accounting comparability has been examined in terms of its effect on voluntary disclosure, analyst forecast properties, or investor portfolio choice. There are also abundant papers to analyze various determinants of earnings management. However, there is limited evidence on the relation between accounting comparability and earnings management, partly due to the difficulty in empirical measurement of accounting comparability. Using the empirical estimate of De Franco et al. (2011), this study sheds light on the relatively unexploited research arena. Second, this paper enriches REM literature. Compared with AEM, REM is a new topic to which researchers have increasingly paid attention. A couple of factors to affect managers’ choice or trade-off between AEM and REM are explored in prior studies but a comprehensive set of determinants for their substitution or complementation has not yet been identified. This paper adds a new factor – accounting comparability – as an important trigger for the substitution of REM for AEM to the pile of previous evidence. Third, this study expands the scope of accounting comparability research. Thus far, accounting comparability has been studied mainly from the view point of accounting inputs such as accounting standards or methods. This comparability is useful to compare accounting attributes of the firms in one country under a certain GAAP regime with those in other country under a different GAAP regime. However, it is hard to compare accounting attributes or economic consequences across firms within a single country (e.g., the U.S.) under the same GAAP regime using this input-based comparability. De Franco et al. (2011) try to address this limitation by operationalizing an output-based accounting comparability measure and find that it works well to explain analysts’ firm selection behavior and their forecast properties. This study tests the usefulness of their comparability measure by investigating its effect on a traditionally popular accounting topic, i.e., earnings management, and corroborates the empirical validity of the measure.

This paper has a policy implication as well. Comparability is an important qualitative characteristic which regulators are concerned with. It reduces the cost of comparing the financial statements of a company with those of others, thereby enhancing the transparency of the company’s financial reporting. Whether intended or not, the increased comparability brings about the mitigation of AEM, which is, however, substituted by REM. If regulators set accounting standards or policies to increase comparability, they need to know its effect on earnings management in general, and on the substitution between AEM and REM in specific, to achieve the goal of the regulations.

چکیده

1. مقدمه

2. تحقیقات مرتبط و توسعه فرضیه

2.1 مقایسه حسابداری و AEM

2.2 مقایسه حسابداری و REM

3. اندازه گیری متغیرهای اصلی و مشخصات تجربی

3.1 مقایسه حسابداری

3.2 شدت AEM

3.3 شدت REM

3.4 مشخصات رگرسیون

4. نتایج تجربی

4.1 نمونه ها، منابع داده ها، آمار توصیفی

4.2آیا مقایسه حسابداری AEM را کاهش و REM را افزایش می دهد؟

4.3 موضوع درونزا

5. آزمون حساسیت و تجزیه و تحلیل اضافی

5.1 استفاده از اقدامات REM فرد

5.2 نقش محیط در اثر مقایسه حسابداری

5.3 نقش کیفیت حسابرسی در اثر مقایسه حسابداری

5.4 آزمون حساسیت دیگر

6. نتیجه گیری

منابع

Abstract

1. Introduction

2. Related research and hypothesis development

2.1. Accounting comparability and AEM

2.2. Accounting comparability and REM

3. Measurement of main variables and empirical specification

3.1. Accounting comparability

3.2. Intensity of AEM

3.3. Intensity of REM

3.4. Regression specification

4. Empirical results

4.1. Samples, data sources, and descriptive statistics

4.2. Does accounting comparability decrease AEM and increase REM?

4.3. Endogeneity issue

5. Sensitivity tests and additional analyses

5.1. Using individual REM measures

5.2. Role of information environment in the effect of accounting comparability

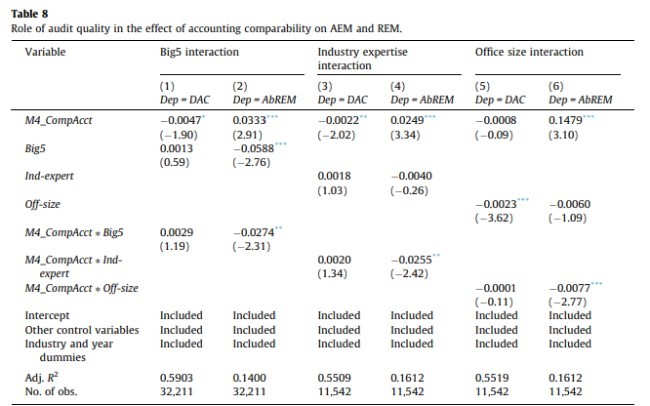

5.3. Role of audit quality in the effect of accounting comparability

5.4. Other sensitivity tests

6. Concluding remarks

References