دانلود رایگان مقاله نحوه اندازه گیری فریم و تاثیر حالت ارزیابی سیستم اطلاعات حسابداری

چکیده

چگونه ارائه اطلاعات در یک سیستم اطلاعات حسابداری(AIS) قضاوت عملکرد زیست محیطی را تحت تاثیر قرار می دهد؟ تصمیم گیرندگان به طور کلی اجرای جایگزین را در یکی از دو حالت ارزیابی، به طور مشترک و یا به طور جداگانه، تجزیه و تحلیل می کند. حالت مشترک اقدامات ارزیابی را گسترده تر به دلیل مقایسه موجود بین تناوب ها ارائه می دهد. بنابراین، اطلاعات اضافی وزن تصمیم بیشتر در حالت جداگانه انبار می شود، که در آن اطلاعات متنی کمتری وجود دارد. با این حال، بسیاری از تنظیمات تصمیم زیست محیطی از حالت ارزیابی جداگانه به دلیل فقدان جایگزینی مناسب (به عنوان مثال، سرمایه گذاری کاهش آلودگی بزرگ) استفاده می شود. در این تنظیم، نظریه ارزیابی عمومی (گت؛ اسی و ژانگ، 2010) بررسی اندازه گیری کم را نشان می دهد زمانی که دانش ارزیابی کم و درک اقدامات غیر ذاتا هر دو ویژگی های مشترک در تنظیمات محیط زیست وجود دارد. این مطالعه ویژگی فریم برای چارچوب GET را معرفی می کند همانطورکه برای در نظر گرفتن در زمان تجزیه و تحلیل تفاوت تصمیم زیست محیطی در سراسر حالت مهم است، چون چارچوب اغلب یک عنصر حیاتی برای ارائه اطلاعات و توضیحات مختلف اغلب منجر به تصمیم گیری های مختلف می شود (دانگان 1993). شرکت کنندگان تجربی (تعداد = 206) اجرای کارخانه زیست محیطی را با حالت مشترک / جداگانه و فریم ویژگی مثبت / منفی ارزیابی می کند. یافته های طراحان AIS را اطلاع می دهد در نتیحه میانه رو حالت ارزیابی ارائه ویژگی چارچوب در تصمیم گیری نشان می دهد. به ویژه، ارزیابی بالاتر (پایین) رخ می دهد زمانیکه از چارچوب مثبت (منفی) استفاده می کند، و این اثر بیشتر (کمتر) در حالت جداگانه (مشترک) بیان می شود. یافته ها همچنین نشان می دهد که قضاوت بهتری در سراسر حالت ارزیابی ثبت نسبت به فریم منفی اندازه گیری عملکرد رخ می دهد .

1. مقدمه

سیستم اطلاعات حسابداری (AIS) طراحی شده اند تا داده ها را جمع آوری و ذخیره کنند و این اطلاعات به تصمیم گیرندگان به عنوان اطلاعات مربوطه و قابل اعتماد ارائه می شود (رامنی و استینبارت، 2015). تصمیم گیرندگان این اطلاعات در طیف گسترده ای از تنظیمات سازمانی ارزیابی می کنند. به طور فزاینده، طبق انتظار ماتریس داده AIS شامل اندازه گیری غیر متعارف، غیر مالی و نسبتا نا آشنا می باشد. تنظیمات تصمیم متشکل از نسبت زیادی از این نوع اطلاعات حسابداری شامل حسابداری ارزش منصفانه می باشد (بنستون، 2006)، حسابداری حسن نیت (وینز و همکاران، 2007)، و ارزیابی عملکرد از طریق کارت امتیازی متوازن (هامفریس) و تروتمن، 2011؛ کاپلان و ویزنر، ) تنظیم این تصمیم به ویژه با اطلاعات حسابداری زیست محیطی برجسته است، که اشخاص به طور فرایندهای تصمیم گیری با هدف بهبود اهداف استراتژیک حفاظت از محیط زیست را درنظرمی گیرند ( جوشی و همکاران، 2001؛ سیم نت و همکاران، 2009). به دلیل افزایش تمرکز بر توانایی جمع آوری مالی، پردازش و ارائه اطلاعات حسابداری زیست محیطی برای ارتباط با سهامداران موسسه و برای ارزیابی جهت کمک به تصمیم گیری های آگاهانه محیط زیست، این مطالعه بر روی تنظیمات تصمیم شامل AIS زیست محیطی تمرکز می کند (براون و همکاران، 2005؛ دیلا و استینبارت 2005).

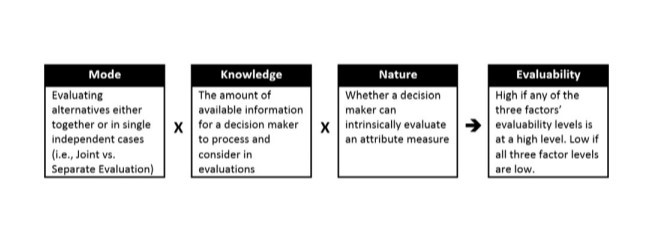

وقتی که با اندازه گیری غیر متعارف و نا آشنا سروکاردارید، چالش خاص برای یک AIS زیست محیطی ارائه اطلاعات زیست محیطی در چنین شیوه هایی می باشد که آن کاهش می یابد، به جای تأکید، موانع شناختی تصمیم گیرندگان به ناچار رو به رو خواهد شد که این داده ها را ارزیابی می کند ( آلوین 2010، سی اف استن و شکید 1994). وقتی که با ارزیابی هر ویژگی مانند اندازه گیری عملکرد سروکارداریم، هسی و ژانگ (2010) نظریه عمومی ارزیابی (GET) پیشنهاد می دهند که سه ویژگی یعنی - ماهیت ویژگی، دانش در مورد ویژگی و ارائه حالت ویژگی باید در نظر گرفته شود. یک ویژگی "ارزیابی " به درجه ای از سهولت اشاره دارد که در آن تصمیم گیرنده می تواند با موفقیت اطلاعات را ارزیابی کند که به ویژگی متصل است، در تصمیم گیری موثر و در نتیجه ارزیابی اشاره دارد. نتایج پایین در ارزیابی پایین حاصل می شود زمانی که هر سه ویژگی مربوطه کم هستند (نه به طور غریزی و یا به طور طبیعی قابل ارزیابی، دانش محدود، و یک حالت ارزیابی جدا شده) . ویژگی های طبیعت و دانش اغلب برای ویژگی تنظیمات حسابداری زیست محیطی کم است، و بنابراین ارائه حالت انبار اهمیت فوق العاده در طراحی AIS زیست محیطی دارد زمانیکه نحوه محدودکردن تعصبات تصمیم احتمالی بررسی می شود. حالت ارزیابی مشترک به تجزیه و تحلیل همزمان چندین گزینه تحت بررسی یک تصمیم اشاره دارد. حالت ارزیابی جداگانه به تجزیه و تحلیل یک گزینه در انزوا برای تصمیم اشاره دارد.

بر اساس چارچوب GET، حالت ارزیابی انتظار می رود که نقش مهمی در حداقل رساندن تعصب تصمیم گیری در زیست محیطی AIS ایفا می کند؛ به هرحال، ارائه عوامل دیگر به احتمال زیاد بر ارزیابی ویژگی ها تاثیر می گذارد. یکی از نمونه های به احتمال زیاد خواص یا ویژگی چارچوب خواهد بود. ویژگی ها زمانی رخ می دهد زمانیکه توصیف مثبت اقلام بیش از اقلام مشابه توصیف شده با شرح منفی ارزیابی می شود ( لوین و همکاران 1998) . اثر ویژگی چارچوب در سراسر زمینه های مختلف تصمیم گیری (پزشکی در مقابل کسب و کار) و تصمیم گیرندگان (متخصص درمقابل تازه کار)قوی بوده است، و ویژگی های اطلاعات حسابداری زیست محیطی به احتمال زیاد به استفاده از ظرفیت توصیفی مثبت و / یا منفی نیاز دارد(به لوین و همکاران، 1998 برای بررسی پیشینه تحقیق مراجعه کنید)

در حالی که بافت محیط زیست به احتمال زیاد نیاز به چارچوب ویژگی دارد، هر AIS به احتمال زیاد شامل ویژگی هایی برای محدود کردن هر گونه تصمیم گیری تعصبی بر اساس توصیف ویژگی مثبت یا منفی می باشد. به ویژه، نسبت توصیف در یک AIS به احتمال زیاد به اندازه ظرفیت شارژ همانند مواردی که در پژوهش های روانی دیده می شود. نمونه هایی مانند زندگی در مقابل مرگ قطعا به احتمال زیاد نیست، در حالی که توصیف، ضعیف تر مانند بازیافت در مقابل بازیافت نمی شوند احتمالا چنین تفاوت های توصیفی نشان داده است تا بر اندازه اثرات چارچوب تاثیر بگذارد (کوه برگر 1995). علاوه بر این، AIS به احتمال زیاد شامل یک معیار به عنوان یک نقطه مرجع برای تصمیم گیرندگان است. تعداد اندکی از مطالعات چارچوب بررسی شده است (برای استثنا به کرلر و همکاران، 2014 مراجعه کنید). از همه مهمتر برای مطالعه حاضر، به هر حال، تاثیر ارائه حالت در اثر ویژگی چارچوب است. ما پیش بینی می کنیم که ارزیابی ویژگی مشترک، تصمیم گیری را افزایش می دهد و بنابراین اثر چارچوب ویژگی های مثبت و منفی را محدود کند. به طور کلی، مطالعه حاضر به دنبال تجزیه و تحلیل تاثیر چارچوب ویژگی های واقع گرایانه در تصمیم گیری های حسابداری زیست محیطی در سراسر حالت ارزیابی جداگانه و مشترک است.

در یک آزمایش آزمایشگاهی، شرکت کنندگان (به تعداد 206 نفر) به طور تصادفی انتخاب و به یکی از چهار شرایط بین شرکت کنندگان اختصاص داده شد. متغیرهای کنترل شده شامل چارچوب ویژگی (مثبت، منفی) و حالت ارزیابی (جداگانه، ارزیابی مشترک) می باشد. معیار های صنعتی به عنوان یک متغیر کنترل شامل می شود، با کارخانه های ارزیابی شده خواهد عملکرد بهتر یا عملکرد بدتر از معیار (یک متغیر داخل، شرکت کنندگان) شرکت کنندگان دو عملکرد کارخانه را در دو اقدامات زیست محیطی سنجش و آنها را بر اساس عملکرد زیست محیطی خود ارزیابی می کنند. این فرایند برای سه جفت دیگر ارزیابی کارخانه تکرار می شود.

همانطور که پیش بینی شد، اثر ویژگی چارچوب طبق انتظار در حالت ارزیابی جداگانه قوی بود، ارزیابی حالت بالاتر (پایین تر) رخ می دهد زمانیکه از ویژگی چارچوب مثبت (منفی) استفاده می کند. این تفاوت حتی در حضور توصیف ویژگی متوسط و حضور معیار ویژگی همچنان ادامه داشت. با این حال، مطابق با پیشینه ارائه در تصمیم گیری، در هنگام ارائه ارزیابی مشترک همراه با معیار صنعت، اثر ویژگی فریم مشاهده نشد. یعنی، هیچ تفاوت ارزیابی بین تنظیمات با استفاده از فریم ویژگی های مثبت و منفی پیدا نشد.

ارائه ویژگی های اطلاعات مختلف توسط سیستم اطلاعات و یا محققان AIS بررسی شده است ( کلتون و همکاران، 2010) . نتایج گزارش شده این مطالعه به تصمیم گیران و طراحان AIS زیست محیطی در مورد نحوه ارائه حالت اطلاع می دهد (جداگانه در مقابل ارزیابی مشترک) تصمیم گیرندگان می توانند در مواجه با داده های غیر سنتی و / یا ناآشنا بهره مند شوند. بویژه، این مطالعه بینش مزایای مقایسه ارزیابی مشترک در ارزیابی جداگانه را ارائه می دهد (در صورت امکان)، همانطورکه تفاوت ظرفیت توصیفی تصمیم گیری بر ارزیابی مشترک تاثیر نمی گذارد. تجزیه و تحلیل های اضافی نیز نشان می دهد قضاوت بهتری در سراسر حالت ارزیابی رخ می دهد که توصیف مثبت در مقایسه با توصیف منفی استفاده می شود. این یافته مفاهیم ارائه اضافی، همانند توصیف مثبت احتمالی را نشان می دهد منجربه تعصب تصمیم کمتر شناختی از توصیف منفی شود. در نهایت، این مطالعه به تماس ها در پیشینه مسائل تحقیقاتی بطور فعالانه پاسخ می دهد که ترکیب AIS و زمینه های حسابداری مدیریت رسیدگی را بررسی می کند، و برای گسترش دیدگاه در برخورد با چنین مسائل با معرفی مبانی نظری، مانند GET، که به طور سنتی در پیشینه AIS در نظر گرفته نشده است (گرانلوند، 2011؛ واسرهلیی، 2012؛ رام و رود، 2007)

این مقاله بعدا توسعه فرضیه را توصیف می کند، و به دنبال روش و نتایج حاصل از یک آزمایش گزارش شده است. این مقاله با بحث از مشارکت، محدودیت ها، و راه برای سوالات تحقیقات آینده نتیجه گیری می کند.

1.1 پیشینه تحقیق و فرضیه

1.1.1 پیشینه حسابداری زیست محیطی و مربوط AIS

برای رسیدن به اهداف سازمانی، سیستم های اطلاعاتی حسابداری (AIS) داده ها را برای تولید اطلاعات مربوطه، قابل اعتماد، کامل، و به موقع را جمع آوری، پردازش و ذخیره می کند. سپس این اطلاعات در یک فرمت مفید و قابل فهم (رامنی و استینبارت،2015 ) برای تصمیم گیرندگان ارائه می شود. تحقیقات تجربی نشان داده است که ارائه اطلاعات تاثیر مهمی در تصمیم گیری دارد. برخی از تحقیقات بر مزایای نسبی یک فرمت نمایشی متمرکز (به عنوان مثال، نمودار در مقابل جداول؛ کاغذ در مقابل صفحه نمایش کامپیوتر؛ 2 بعدی در مقابل 3 بعدی)، و برخی دیگر بر تأثیرات یک عنصر نمایشی (به عنوان مثال، رنگ ها، دامنه های نمودار، خطوط، تعامل، چند رسانه ای)، برخی دیگر هم در تعامل بین ارائه اطلاعات و عوامل دیگر، مانند ویژگی های کاربران و یا وظایف مورد نیاز تمرکز کرده است. (باکیک و آپان ، 2012؛ دپرسنی، 2011؛ دیلا و همکاران، 2010؛ کلتون و همکاران، 2010؛ شفت و وسی، 2006؛ وسی، 1991).

How does information presentation within an accounting information system (AIS) influence environmental performance judgments? Decision makers generally analyze alternatives' performances in one of two evaluation modes: jointly or separately. Joint mode provides greater measure evaluability because of available comparisons between alternates. Thus, additional information garners greater decision weight in separate mode, where less contextual information exists. However, many environmental decision settings use separate evaluation mode because of no viable alternatives (e.g., large pollution abatement investments). In this setting, General Evaluability Theory (GET; Hsee and Zhang, 2010) suggests low measurement evaluability when low measurement knowledge and non-inherently understood measures exist—both common characteristics in environmental settings. This study introduces attribute framing to the GET framework as important to consider when analyzing environmental decision differences across modes, because frames are often a necessary component of information presentation and different descriptions often lead to different decisions (Dunegan, 1993). Experimental participants (n = 206) evaluated factory environmental performances with joint/separate mode and positive/negative attribute framing. Findings inform AIS designers as results suggest evaluation mode moderates the presentation of attribute frames on decisions. Specifically, higher (lower) evaluations occur when using positive (negative) framing, and this effect is more (less) pronounced in separate (joint) mode. Findings also suggest that more consistent judgments occur across evaluation mode with positive compared to negative framing of performance measures.

1. Introduction

Accounting information systems (AIS) are designed to collect and store data and to present this data to decision makers as relevant and reliable information (Romney and Steinbart, 2015). Decision makers evaluate this information in a wide range of organizational settings. Increasingly, AIS data matrices are expected to include nontraditional, nonfinancial, and relatively unfamiliar measurements. Decision settings consisting of large proportions of this type of accounting information include fair value accounting (Benston, 2006), goodwill accounting (Wines et al., 2007), and performance evaluations via a balanced scorecard (Humphreys and Trotman, 2011; Kaplan and Wisner, 2009).This decision setting is particularly prominent with environmental accounting information, which entities increasingly consider in decisions aimed at improving environmental stewardship strategic objectives (Joshi et al., 2001; Simnett et al., 2009). Because of the increasing focus afforded to the collecting, processing, and presenting of environmental accounting information for communication to entity stakeholders and for assessment to aid in environmentally conscious decisions, this study focuses on decision settings involving environmental AIS (Brown et al., 2005; Dilla and Steinbart, 2005).

When dealing with nontraditional or unfamiliar measurements, a particular challenge for an environmental AIS is to present environmental information in such a way that it alleviates, rather than accentuates, the cognitive hurdles decision makers will inevitably face when evaluating this data (Alewine, 2010; cf. Stone and Schkade, 1994). When dealing with the evaluability of any attribute such as a performance measurement, Hsee and Zhang's (2010) General Evaluability Theory (GET) suggests that three characteristics should be considered – the nature of the attribute, the knowledge about the attribute, and the mode of attribute presentation. An attribute's “evaluability” refers to the degree of ease in which a decision maker can successfully assess the information that is attached to the attribute, resulting in effective decision making. Low evaluability results when all three attribute characteristics are low (not instinctively or naturally evaluable, limited knowledge, and an isolated evaluation mode). The nature and knowledge characteristics are often low for attributes in environmental accounting settings, and thus the presentation mode garners extra significance in environmental AIS design when considering how to limit possible decision biases. Joint evaluation mode refers to a simultaneous analysis of multiple alternatives under consideration in a decision. Separate evaluation mode refers to the analysis of one alternative in isolation for a decision.

Based on the GET framework, evaluation mode is expected to play an important role in minimizing decision bias in an environmental AIS; however, other presentation factors are likely to impact attribute evaluations. One likely example would be attribute framing. Attribute framing occurs when functionally equivalent information is described either positively (chance of success) or negatively (chance of failure). The attribute framing effect occurs when the positive description of an item is evaluated more highly than the same item described with a negative description (Levin et al., 1998). The attribute framing effect has been robust across various decision contexts (medical vs. business) and decision makers (expert vs. novice), and the characteristics of environmental accounting information are likely to require the use of positive and/or negative descriptive valences (see Levin et al., 1998 for a literature review).

While the environmental context likely requires attribute frames, any AIS is likely to include characteristics to limit any decision bias based on positive or negative attribute descriptions. Specifically, attribute descriptions in an AIS are unlikely to be as valence-charged as those seen in psychological research; examples such as life vs. death are certainly not likely, while ‘weaker’ descriptors such as recycled vs. not recycled are likely. Such descriptive differences have been shown to impact the size of framing effects (Kuhberger, 1995). In addition, an AIS would likely include a benchmark as a reference point for decision makers. Very few framing studies have considered benchmarks (see Kerler et al., 2014 for an exception). Most importantly for the current study, however, is the impact of presentation mode on attribute framing effects. We predict that joint evaluations will increase attribute evaluability in decision making and therefore limit the effect of positive and negative attribute frames. Overall, the current study seeks to analyze the impact of realistic attribute frames on environmental accounting decisions across separate and joint evaluation modes.

In a laboratory experiment, participants (n = 206) were randomly assigned to one of four between-participant conditions; manipulated variables include attribute framing (positive, negative) and evaluation mode (separate, joint evaluation). An industrial benchmark was included as a control variable, with assessed factories being either all better-performing or all worseperforming than the benchmark (a within-participant variable). Participants assessed two factory performances on two environmental measures and evaluated them based on their environmental performance. This process was repeated for three other pairs of factory evaluations.

As predicted, the attribute framing effect was robust in expected directions in the separate evaluation mode—higher (lower) evaluations occurred when using positive (negative) attribute frames. These differences persisted even in the presence of moderate attribute descriptions and the presence of attribute benchmarks. However, consistent with the literature on presentation mode in decisions, when providing joint evaluations along with the industry benchmark, the attribute framing effect was not observed. That is, no evaluation differences were found between settings using positive and negative attribute frames.

Various information presentation characteristics have been examined by information system or AIS researchers (Kelton et al., 2010). The study's reported results inform decision makers and environmental AIS designers on how presentation mode (separate vs. joint evaluation) can benefit decision makers faced with non-traditional and/or unfamiliar data. Specifically, this study provides insight on the advantage of joint evaluation comparisons over separate evaluation (when possible), as descriptive valence differences do not impact decisions in joint evaluations. Additional analysis also suggests more consistent judgments occur across evaluation mode when positive descriptions are used compared to negative descriptions. This finding suggests additional presentation implications, as positive descriptions may cause less cognitive decision bias than negative descriptions. Finally, this study answers calls in the AIS literature to proactively address research matters that combine AIS and management accounting fields, and to expand perspectives on dealing with such issues by introducing theoretical foundations, such as GET, that have not been traditionally considered in the AIS literature (Granlund, 2011; Vasarhelyi, 2012; see Rom and Rohde, 2007).

This paper next describes the hypotheses development, followed by the procedure and reported results of an experiment. The paper concludes with a discussion of contributions, limitations, and avenues for future research inquiries.

1.1. Literature and hypotheses

1.1.1. Relevant AIS and environmental accounting literature

To achieve organizational goals, accounting information systems (AIS) collect, process, and store data to produce relevant, reliable, complete, and timely information. This information is then presented to decision makers in a useful and intelligible format (Romney and Steinbart, 2015). Empirical research has evidenced that information presentation has a significant impact on decision making. Some research has focused on the relative advantages of a presentational format (e.g., graphs vs. tables; paper vs. computer screen; 2D vs. 3D), others on the influences of a presentational element (e.g., colors, graph slopes, gridlines, interactivity, multimedia), still others on the interaction between information presentation and other factors, such as user characteristics or task requirements (Bacic and Appan, 2012; Debreceny, 2011; Dilla et al., 2010; Kelton et al., 2010; Shaft and Vessey, 2006; Vessey, 1991).

چکیده

1. مقدمه

1.1 پیشینه تحقیق و فرضیه

1.1.1 پیشینه حسابداری زیست محیطی و مربوط AIS

1.1.2 نظریه ارزیابی عمومی

1.1.3 ویژگی فریم

1.1.4 نسبت فریم و حالت ارزیابی

2. روش

2.1 شركت كنندگان

2.2 روش

2.3 ضرورت اطلاعات معیار به عنوان یک متغیر شرکت کنندگان داخلی

2.4 اندازه گیری

2.5 روش های آماری

3. نتایج

3.1 شرکت کنندگان در تحقیقات

3.2 اعتبار اندازه گیری

3.3آزمون فرضیه

4. بحث

5. نتیجه گیری

منابع

Abstract

1. Introduction

1.1. Literature and hypotheses

1.1.1. Relevant AIS and environmental accounting literature

1.1.2. General evaluability theory

1.1.3. Attribute framing

1.1.4. Attribute framing and evaluation mode

2. Method

2.1. Participants

2.2. Procedure

2.3. Necessity of benchmark information as a within-participant variable

2.4. Measurements

2.5. Statistical methods

3. Results

3.1. Research participants

3.2. Measurement validity

3.3. Tests of hypotheses

4. Discussion

5. Conclusion

References